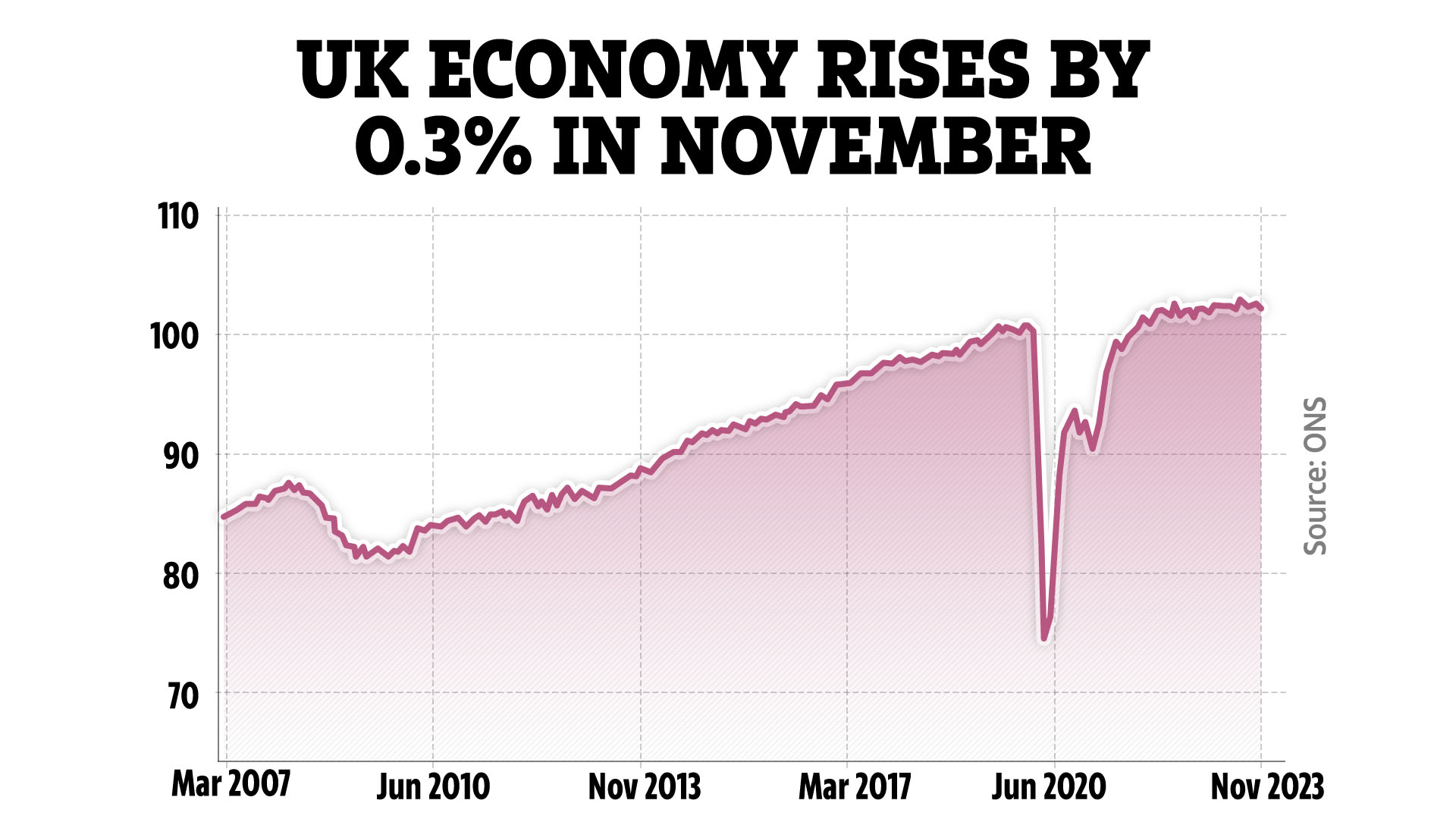

THE economy shrank by 0.3% in the final few months of 2023, the latest figures from the Office for National Statistics (ONS) show.

It means the UK tipped into a technical recession, which is defined as two or more quarters in a row of falling Gross Domestic Product (GDP).

1

This is due to the economy contracting by 0.1% in December.

GDP measures the value of goods and services produced in the UK.

It also estimates the size and growth of the economy.

Services output fell by 0.1% in December, and in the final three months of the year services output fell by 0.2%.

READ MORE IN MONEY

Meanwhile, production output grew by 0.6% in December, but in the three months of 2023 production output fell by 1.0%.

Today’s data follows a 0.1% contraction in the previous three months, the third quarter.

ONS estimates suggest the economy did not grow at all between April and June before shrinking between July and September, which left the UK at risk of recession in the final three months.

The UK last went into recession in 2020 after the coronavirus pandemic hit, shutting down large parts of the economy.

Most read in Money

The 2020 recession lasted just six months, while the previous instance in 2008 lasted one and a half years.

In a recession, job losses are common, as companies try to cut their costs to stay afloat.

Liz McKeown, ONS director of economic statistics, said: “Our initial estimate shows the UK economy contracted in the fourth quarter of 2023.

“While it has now shrunk for two consecutive quarters, across 2023 as a whole the economy has been broadly flat.

“All the main sectors fell on the quarter, with manufacturing, construction and wholesale being the biggest drags on growth.”

Most economists had been forecasting a 0.1% decline in GDP between October and December.

Experts had said that if confirmed, it would be a recession in the “mildest of senses” and is likely to be short-lived, with many preferring to describe the UK’s economy as having “stagnated”.

Bank of England governor Andrew Bailey had signalled that a recession, if confirmed, would likely be brief, telling a Lords committee on Wednesday that the UK economy was beginning to pick up.

But a technical recession may further add to the case for an interest rate cut, with the Bank already indicating it’s more a case of when, not if, a reduction will come.

Official data on Wednesday showed inflation defied expectations for a rise in January to unexpectedly hold firm at 4%.

This is seen as giving policymakers at the Bank more room to consider rate cuts, from the current level of 5.25%.

Nevertheless, while Mr Bailey said the latest data was “good news”, he said that inflation remaining unchanged “leaves us broadly where we thought we were going to be”.

Chancellor Jeremy Hunt said low economic growth is “not a surprise”, but he added that the UK must “stick to the plan – cutting taxes on work and business to build a stronger economy” despite tough times for many households.

The Chancellor said: “High inflation is the single biggest barrier to growth which is why halving it has been our top priority. While interest rates are high – so the Bank of England can bring inflation down – low growth is not a surprise.

“But there are signs the British economy is turning a corner; forecasters agree that growth will strengthen over the next few years, wages are rising faster than prices, mortgage rates are down and unemployment remains low.

“Although times are still tough for many families, we must stick to the plan – cutting taxes on work and business to build a stronger economy.”

What does it mean for your finances?

Today’s figures mean the economy has shrunk for two quarters in a row, leading to a recession.

Job losses are common during a recession, as companies try to cut their costs to stay afloat.

Businesses may also go into administration or go bust.

The 2008 recession, for example, saw the loss of high street stores including music retailer Zavvi, clothes shop Principles, and stalwart Woolworths.

The Government may make cut backs or raise taxes to try and shore up its finances – alternatively, it may decide to increase budgets to spend its way out of the problem.

And the number of people in debt and arrears is also likely to soar, and there could be more defaults on loans and mortgages or repossessions and bankruptcies.

How to protect your finances

There are ways you can keep your cash safe if you’re worried about the UK’s economic outlook.

Make sure you go through all your bank statements and accounts so you know what your income and outgoings are every month.

Of course, there are bills that you can’t avoid paying – but that doesn’t mean you can’t cut back in other ways.

For example, you can save money by moving to a cheaper mobile phone tariff or by axing subscriptions you don’t need like Netflix or Amazon Prime.

If you’ve got any outstanding debts, the worst thing to do is ignore them as it will only make your financial situation worse.

Stay on top of what you owe and always repay priority debts.

There are also plenty of organisations where you can seek debt advice for free.

You should also check what benefits you are eligible for as you might be able to claim without realising.

Entitledto’s free calculator works out whether you qualify for various benefits, tax credits and Universal Credit.

If you don’t want to register, consumer group moneysavingexpert.com and charity StepChange both have benefits tools powered by Entitledto’s data that let you save your results without logging in.

There is also emergency funding available for struggling households, which is dished out by local councils.

The Household Support Fund is designed to help those on a low income or benefits cover the cost of food, energy and general living costs.

What help is available varies depending on where you live as each council sets it own eligibility criteria.

READ MORE SUN STORIES

It’s worth getting in touch with your local authority to see what you might be able to get.

You can find what council area you fall under by using the government’s council locator tool online.

How to get debt help for free

THERE are several groups which can help you with your problem debts for free.

- Citizens Advice – 0800 144 8848 (England) 0800 702 2020 (Wales)

- StepChange – 0800 138 1111

- National Debtline – 0808 808 4000

- Debt Advice Foundation – 0800 043 4050

You can also find information about Debt Management Plans (DMP) and Individual Voluntary Arrangements (IVA) on the MoneyHelper and on the Government’s Gov.uk site.

Speak to one of these organisations – don’t be tempted to use a claims management firm. They say they can write-off lots of your debts in return for a large up-front fee. But there are other options where you don’t need to pay.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories.