Risk aversion sentiment dominated once again this week, but unfortunately for USD bulls, the Greenback wasn’t able to benefit as it seems traders priced in the odds of a U.S. recession ahead rose, leading to the worst performance of the week.

The Swiss franc was the winner this week among the major currencies, sparked by comments from SNB Chair Jordan on there being a possibility the SNB would move to curb inflation if needed.

Notable News & Economic Updates:

China kept its key interest rate unchanged on Monday despite sharp economic slowdown due to covid restrictions

The IMF lifted the yuan’s weighting in its Special Drawing Rights currency basket

U.S. retail sales in April: +0.9% m/m vs. 1.0% m/m forecast and 1.4% previous read; core retail sale dipped lower to 0.6% vs. 2.1% previous

Sweden Foreign Minister Ann Linde signed an application declaring Sweden’s intention to join NATO on Tuesday

Fed Chair Powell said on Tuesday that the Fed will not hesitate to keep raising rates until inflation comes down

US EIA weekly crude oil inventories -3394K vs +1383K expected

Shanghai authorities gradually lift COVID-19 restrictions

Turkey’s Erdogan digs in over NATO expansion as Biden hosts Finnish, Swedish leaders

PBOC cut the 5-year loan prime rate to 4.45% from 4.6% to boost economy

European gas futures prices fell this week on rising stockpiles

U.S. equities end the week down 20% from record highs, officially entering a technical bear market

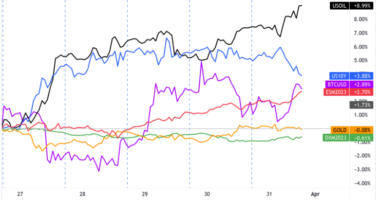

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour

Looking at the chart above, it’s pretty clear it was another round of risk-off vibes as most major asset classes closed in the red on Friday. But there is one big change in that we saw weakness in the Greenback and a fall in bond yields, while bond prices (which have been destroyed in 2022) and gold found strength through the latter half of the week.

Arguments can be made that traders are starting to price in rising odds of a global recession around the corner, especially in the U.S. given the persistently strong inflation updates and rate hike rhetoric from the Fed, and weakening U.S. economic/survey data.

We also got a round of earnings reports from the U.S.’s largest retailers like Walmart and Target this week, broadly signaling that U.S. consumers were pulling back on discretionary items, echoing Amazon’s slowing growth sentiment at their earnings call in April.

The big turn in risk sentiment towards negative on Wednesday correlated with Target’s earnings release, so that may have been the spark to light the big risk-off move, characterized by a fall in equities, crypto, bond yields and oil against a pop higher in gold and bond prices. It also shows that traders may have been waiting to see what the U.S. retail sector would print before making moves on the broad markets.

This sentiment continued on through the Thursday Asia and London sessions before bottoming out in the U.S. session, correlating with another round of weak U.S. data points, including a tick higher in U.S. unemployment claims and Philly Fed manufacturing survey data. We guess the argument here could be that the more we see weaker data points, the odds fall of a more aggressive rate hiking cycle ahead.

Risk assets continued to drift higher into the Friday session, possibly with the help of news from China that the People’s Bank of China cut the 5-year loan prime rate to 4.45% to help boost their economy. But risk sentiment took a negative turn once again during the U.S. session, with no apparent direct catalyst for the quick shift in risk vibes.

In the forex space, the Swiss franc took the top honors, boosted heavily by a speech from Swiss National Bank Chair Thomas Jordan on Wednesday. He signaled that the SNB is ready to act if inflation pressures continue, a surprise idea given the SNB’s usual stance of intervening in the forex markets to weaken the Swiss franc if necessary.

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

NY manufacturing index slumps to -11.6 in May vs. expected drop to 15.5

U.S. Industrial Production increased by 1.1% in April vs. 0.4% forecast

U.S. business inventories rose 2.0% in March vs. 1.8% increase in February & 1.9% forecast.

Federal Reserve Bank of St. Louis President James Bullard showed support for Fed’s plan to raise by 50 bps in upcoming meetings

US homebuilder sentiment fell in May to 69 vs. 77 in April, the largest fall since April 2020.

Fed official Evans: Transition to 0.25% hikes expected by July or Sept

Permits for future U.S. homebuilding tumbled by 3.2% to a five-month low in April

Janet Yellen confirms she is pressing Joe Biden administration for some China tariff cuts

Philadelphia Fed Manufacturing Index slowed to 2.6 in May vs. 17.6 in April, the lowest read in two years

Weekly U.S. initial unemployment claims rose to 218K last week vs. a 200K forecast

U.S. existing home sales fell -2.4% m/m in April; -5.9% y/y; inventory continues to be tight at a 2.2 month-supply, keeping prices higher

Fed official Kashkari: FOMC might wind up needing to hike further

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

UK unemployment falls 3.7%, the lowest level in nearly 50 years

UK jobs data shows more job openings than people out of work for the first time on record

UK real wage growth decreased as higher inflation hurt consumers’ purchasing power

U.K. headline CPI rose from 7.0% to 9.0% y/y vs. 9.1% forecast; core CPI climbed from 5.7% to 6.2% as expected in April

U.K. Finance Minister Sunak: Inflation jump driven by energy price cap rise

U.K. retail sales rebounded by 1.4% m/m in April vs. estimated 0.3% dip, previous -1.2% m/m slide in March

U.K. consumer confidence index fell to -40 in May, the lowest level since 1974

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

German wholesale prices up 2.1% vs. projected 4.2% increase

Euro area Flash GDP: 0.3% q/q; employment change was 0.5%

Dutch central bank chief Klaas Knot says the ECB should raise by 25 bps in July, but a bigger increase shouldn’t be ruled out

ECB policymakers Rehn and de Cos pushed for quick monetary policy normalization on Wednesday

Eurozone CPI (Final) in April: +7.4% y/y vs. +7.5% y/y forecast; core CPI at +3.5% y/y

ECB Monetary Policy Meeting Accounts showed inflation worries and policy action urgency. No commitment to plans on interest rates but ending bond purchases in Q3 is still confirmed.

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

SNB Chair Thomas Jordan speech on Wednesday:

- Swiss National Bank not a hostage to other central banks

- Inflation is expected to fall back within SNB’s target 0 to 2% range

- SNB ready to act if inflation pressures persist, but no indications of a need to move at this time

- Ready to intervene in currency markets when necessary

CAD Pairs

Overlay of CAD Pairs: 1-Hour Forex Chart

Canadian housing starts was 257,846 units in April, up from 253,226 units in March – CMHC

Statistics Canada says higher prices lifted manufacturing (+2.5%) and wholesale sales (+0.3%) in March

Canada Industrial Product Price Index (IPPI) rose 0.8% m/m in April; Raw Materials Price Index (RMPI) slipped by -2.0% m/m

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

New Zealand Services PMI (April) 51.4 (prior was 51.6)

New Zealand GDT dairy prices fell by 2.9%, following earlier 8.5% drop

New Zealand plans to spend NZ$1 billion to ease inflation pain

New Zealand PPI Inputs +3.6% On Quarter, Outputs +2.6% In Q1

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

RBA minutes: Central bank considered raising cash rate by 15bp, 25bp, or 40bp

RBA minutes: Inflation may peak at 6% by the end of 2022

Australia’s wage price index up by 0.7% vs. 0.8% forecast in Q1

Australian MI leading index fell by 0.2% in April

Australia’s jobless rate at a 50-year low of 3.9% but fewer positions were added in April than predicted

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Japanese preliminary machine tool orders slowed from 30% to 25.5%

Japan Tertiary Industry Activity Index rose 1.3% m/m to 97.6 in March

Bank of Japan Deputy Governor Masayoshi Amamiya vowed to continue “powerful monetary easing”

The Japan Tourism Agency announced on Tuesday that small group tours may be allowed soon in May

Japan GDP preliminary for Q1 2022: -0.2% q/q

Tankan’s Japan manufacturers’ sentiment index for May: +5 vs +11 in April, the lowest since February 2021

Japan’s core machinery orders rise 7.1% vs. 3.9% expected in March

Japan’s trade gap widens in April as imports (28%) outpace exports (12.5%)