The lack of major data releases and central bank announcements steered the markets’ focus back to easing fears of global banking concerns and rising expectations of a less hawkish Fed.

Risk-taking became the name of the game and volatile assets like Bitcoin, equities, and crude oil traded higher while safe-havens like USD and JPY lost ground.

Notable News & Economic Updates:

The U.S. Commodities Futures Trading Commission (CFTC) filed a lawsuit against Binance Holdings Ltd., the biggest cryptocurrency exchange in the world, and its CEO Changpeng Zhao for allegedly breaching derivatives laws.

Crude oil jumped after the Iraqi federal government and Kurdish officials failed to agree on the resumption of around 400,000 barrels a day of oil exports from a Turkish port.

Australia’s inflation decelerated from 7.4% to an eight-month low of 6.8% in February and supported a pause in RBA’s rate hikes.

U.S. GDP in Q4 2022 was lowered again to 2.6% y/y vs. the initial read of 2.9% y/y; consumer spending was weaker than originally thought, now seen at 1.4% y/y vs. initial expectations of 2.1%.

Gov. Bailey hinted that the BOE isn’t too worried about the banking sector, saying “With the Financial Policy Committee on the case of securing financial stability, the Monetary Policy Committee can focus on its own important job of returning inflation to target.”

U.S. Treasury Secretary Janet Yellen called for stronger regulation of the non-bank or “shadow bank” sector that includes money market funds, hedge funds, and crypto assets.

The U.K. economy grew by 0.1% in Q4 and avoided a formal recession thanks to increased tourism and governmental assistance for energy costs.

The U.K. was accepted into the 11-economy Trans-Pacific Partnership, which could add 1.8 billion GBP to the GDP over time.

Banking sector updates:

- First Citizens BancShares Inc. agreed to buy Silicon Valley Bank, acquiring about $72Bn in assets at a discount of $16.5B.

- Michael Barr, the Fed’s vice chairman for supervision, said on Monday that Silicon Valley Bank failed due to not effectively managing its liquidity and interest rate risk.

- U.K.’s Financial Policy Committee (FPC): U.K. banking system is resilient and well capitalised

- The IMF believes the BOJ should consider allowing longer-term interest rates to move more flexibly to help ease strains in Japan’s financial institutions.

- On Thursday, President Joe Biden urged federal regulators to “strengthen oversight and regulation of larger banks.” Reforms that “can be accomplished under existing law” or without Congress participation include raising liquidity requirements, updating stress tests, and limiting banks that must contribute to the Deposit Insurance Fund that saved SVB.

Central Bank Updates:

- Erik Thedeen, governor of the Riksbank, said on Sunday that the Swedish central bank may have misjudged inflationary pressures and will likely have to stick to its outlook of another interest rate increase in April.

- According to Bundesbank President Joachim Nagel on Monday, the European Central Bank is committed to keep battling inflation while also being prepared to react to any future market stress.

- Bank of Thailand raised the policy rate by 25 bps to 1.75%

- The South African Reserve Bank raised interest rates by 50 bps (double the 25 bps forecast) to 7.75%

- Kenya’s Central Bank raised the policy rate to 9.5% on Wednesday, above 9.0% expectations and the 8.75% previous policy rate

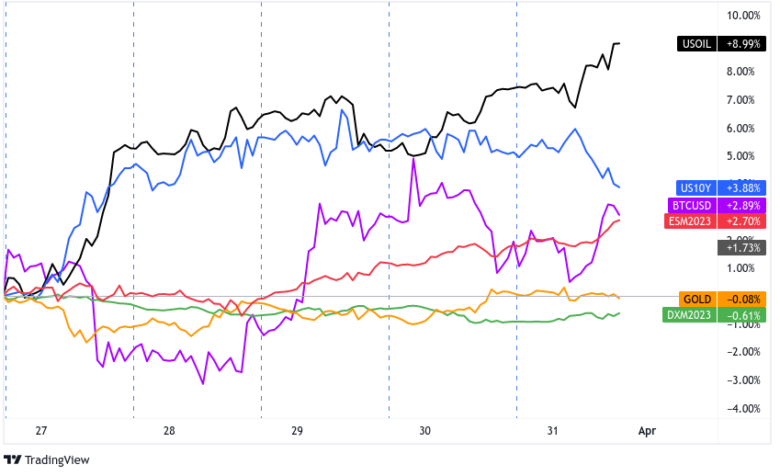

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour by TradingView

There were not a lot of top-tier economic reports to price in this week, so traders were free to digest the latest banking sector headlines from the Monday open.

At the start of the week, fears of the rising costs of Deutche Bank’s credit default swaps – the cost of protection against a default – were somewhat alleviated by the news of the FDIC facilitating First Citizens BancShares Inc. acquisition of SVB’s loans and deposits.

Michael Barr, the Fed’s vice chairman for supervision, also shared in a testimony that SVB’s situation was caused by liquidity mismanagement. This implied that the fallout was an SVB problem and is not as common among other banks.

Easing banking crisis concerns and better-than-expected lower-tier U.S. economic data redirected the markets to pricing in a continuation of the Fed’s tightening program.

2-year and 10-year Treasury yields traded sharply higher while interest rate-sensitive tech stocks (and consequently equities markets) dipped to their intraweek lows on Tuesday.

Fiat currencies straight up priced in risk-taking, though, characterized by the “safe-havens” like USD and JPY dropped like rocks while riskier currencies like AUD, NZD, CAD, and GBP shot up on Monday and Tuesday.

Crude oil prices got an extra boost from the International Chamber of Commerce ruling against Turkey and its state-owned pipeline operator BOTAS for transporting Kurdish oil without prior approval from Iraq.

The suspension of Iraqi Kurdish oil export to Turkey is expected to take out about 450,000 barrels per day from the global oil supply. It caused bullish spikes and eventually new intraweek gains for both Brent and WTI crude oil prices.

On Wednesday, Alibaba’s decision to split its conglomerate into six business groups got the risk-on party started for global equities as it signaled that China is more willing to work with its tech sector.

Traders may have also started pricing expectations for Friday’s U.S. core PCE price index, that the rate may slow and support the narrative of the Fed pausing its rate hikes after a May increase. U.S. equities saw a bullish mid-week reversal and gold pulled back from its Tuesday highs.

Bitcoin, which dropped to the $26,800 technical support area on Monday when the CFTC sued Binance and CEO Changpeng Zhao, jumped on the bull train as well and broke through the $29,000 major resistance.

The bond markets said “cap” to rate hike pause and rate cut expectations though, as the 2-year and 10-year Treasury yields made new intraweek highs by mid-week at 3.61%.

On Friday, the highly anticipated U.S. core PCE price index data came and went, coming in a tick lower than expected at 0.3% m/m vs. 0.4% m/m forecast. The reaction was a move lower in bond yields and gold, while equities, crypto and oil continued to ride higher ahead of the weekend close.

Zooming onto FX, the pound was one of the broader winners this week on expectations of further tightening from the BOE. Governor Bailey implied that the central bank will continue to focus on “returning inflation to target.” The Financial Policy Committee (FPC), whose job is to worry about banking concerns, also put out a statement saying that “the U.K. banking system is resilient and well capitalized.”

The GBP train continued in its bullish direction on early Friday when the U.K. got accepted into an 11-economy Trans-Pacific Partnership that’s expected to add at least £1.8B to the GDP over the coming years. Meanwhile, the latest GDP report from the U.K. showed the economy avoiding a technical recession. Phew!

Despite Sterling’s strength this week, it was the Canadian dollar that took the top spot thanks to the broad risk-on vibes and the strong push higher in oil prices, but it was the yen that saw the highest volatility this week with multiple 2.00% or more drops against the majors.

The Japanese yen’s weakness was likely not only on the return of risk-on vibes, but also likely influenced by the lower-than-expected Japanese core inflation update and a sharp rally in USD/JPY.

Most Notable FX Moves

USD Pairs

Over the weekend, FOMC member Neel Kashkari the Fed is “monitoring very, very closely” the recession risks of the recent bank turmoil, implying that the Fed is close to its “peak rates”

Dallas Fed Manufacturing Survey for March: 2.5 vs. -2.8 previous; employment index was +11 to 10.4

Richmond Fed Manufacturing Index for March improved to -5 vs. -10 in February; firms remained negative on future local business conditions, but see supply chain issues easing (but remaining negative)

The U.S. merchandise-trade deficit grew slightly in February to -$91.6B from -$91.1B in January

U.S. pending home sales index for February: +0.8% m/m to 83.2 vs. +8.1% m/m previous

U.S. weekly initial jobless claims increase 7K over last week to 198K; continuing claims rose by 4K to 1.689M

EUR Pairs

Improved business expectations helped push Germany’s Ifo business-climate index from 91.1 to 93.3 in March, its highest reading since May 2022.

Euro Area broad M3 money supply growth rate in February: 2.9% y/y vs. 3.5% y/y in January; growth rate of adjusted loans to households fell to 3.2% y/y vs. 3.6% y/y in Jan.

According to data released on Monday by the European Central Bank, the growth of corporate lending in the Eurozone decreased in February from 6.1% to 5.7%

Germany GfK Consumer Sentiment for April: -29.5 vs -30.6 in March

According to Chief Economist Philip Lane in an interview with Zeit, the European Central Bank will need to raise interest rates even more if recent financial system tensions are kept in check.

Germany Preliminary CPI for March: +0.8% m/m vs. +0.7% m/m forecast; food price growth continues to remain high while energy prices have slowed dramatically

Germany’s retail sales down 1.3% m/m in February, marking the third consecutive month of decreases, due to high inflation and sluggish consumer demand.

Euro area Unemployment Rate in February 2023: 6.6% as expected/previous

Euro area Flash CPI read for March 2023: 6.9% y/y vs. 8.5% y/y read in February; core hits record high of 5.7% y/y as expected vs. 5.6% y/y previous

GBP Pairs

U.K. Retail sales volumes were steady year-to-March (weighted balance +1% from +2% in February). Sales are predicted to rise 9% next month, the first gain since September 2022. – CBI

CBI: U.K. retailers reported their first positive sales expectations in seven months in April.

BRC: higher food prices accelerated shop price inflation from 8.4% to 8.9% m/m in March, its fastest rate in at least 18 years.

U.K. mortgage approvals for February: 43.5K vs. 39.6K in January; Consumers borrowed £1.4B in February vs. £1.7B in January

Slide in U.K.’s house prices accelerated from 1.1% to 3.1% in March, the fastest annual decline since July 2009.

The U.K. economy grew by 0.1% in Q4 and avoided a formal recession thanks to increased tourism and governmental assistance for energy costs.

The U.K. was accepted into the 11-economy Trans-Pacific Partnership, which could add £1.8B to the GDP over time.

CHF Pairs

Swiss National Bank Quarterly Bulletin March 2023

- Global growth momentum and the outlook for the coming quarters remain subdued

- SNB anticipates GDP growth of around 1% for 2023

- Short term inflation expectations remain elevated

Switzerland’s real, seasonally adjusted retail sales grew by 0.3% y/y in February after a 2.2% dip in January

CAD Pairs

Canada posted a budget deficit of 6.44B CAD in the first ten months of the 2022-2023 fiscal year, down from the 75.29B CAD deficit in the same period last year.

Canada GDP for January 2023: +0.5% m/m to CA$ 2.078T vs. -0.1% m/m in December

AUD Pairs

Australia’s retail sales rose by 0.2% m/m in February, lower than January’s 1.8% uptick but beating 0.1% growth expectations.

Australia’s inflation decelerated from 7.4% to an eight-month low of 6.8% in February and supported a pause in RBA’s rate hikes.

Australia’s trade union body submitted proposal for 7% minimum wage increase, although only 5% hike is expected in June

Australia Job Vacancies for February: – 1.5% q/q to 438.5K; still 92.4% higher than the start of the 2020 pandemic signaling continued labor shortages across most industries

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

New Zealand ANZ business confidence index dipped from -43.3 to -43.4 in March, as inflation indicators inched slightly lower

On Thursday, Statistics New Zealand reported a seasonally adjusted 9.0% reduction in new dwelling consents in February compared to a 5.2% drop in January; Building consents fell 29.2% y/y

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Japan Services PPI for February: +1.8% y/y as expected vs. +1.6% y/y previous

BOJ’s core CPI – a measure of underlying inflation – eases from 3.1% to 2.7% y/y in March

Easing semiconductor shortages helped boost Japan’s industrial production by another 4.5% m/m in February

Housing starts dip by 0.3% y/y in February after a 6.6% surge in January

Retail sales jumped from 5.0% to 6.6% y/y in February. This marks the steepest gain since May 2021.

The IMF believes the BOJ should consider allowing longer-term interest rates to move more flexibly to help ease strains in Japan’s financial institutions.

Tokyo’s core CPI – a leading indicator of Japan’s inflation – rose by 3.2% y/y in March, marking the second consecutive month of deceleration since the 40-year high of 4.3% in January.

Japan’s unemployment rate ticked up by 0.2 points to 2.6% – its first increase in five months – as employees seek better working conditions.

Japan’s housing starts dip by 0.3% y/y in February after a 6.6% surge in January