Broad risk sentiment leaned positive this week as early data on Omicron variant cases appeared to be less severe than originally feared. With no other notable catalysts, the major currency pairs performed as expected in this environment with the “safe havens” taking a back seat to higher-risk currencies this week.

Notable News & Economic Updates

Extremely early Omicron data shows variant may be less threatening as cases so far have shown mild symptoms.

Reserve Bank of Australia kept interest rates unchanged at 0.10% as expected in December, will discuss QE program in February

Oil rebounds above $71 per barrel on Monday on Iran talks

Brazil Central Bank makes 150 bps interest rate Hike to 9.25% and signals more may be on the way

Bank of Canada kept the overnight rate unchanged at 0.25% on Wednesday

GDP up by 2.2% and employment up by 0.9% in the euro area; In the EU, GDP up by 2.1% and employment up by 0.9%

Evergrande missed payment deadlines and entered “restricted default” status.

U.S. inflation accelerated more than expected to 6.8% in November, the fastest rate since 1982

Intermarket Weekly Recap

Due to the lack of fresh major catalysts for most of the week, the early rebound in risk taking behavior seemed to have focused mainly on Omicron variant developments. Early Omicron data from South Africa showed that the variant may be more transmissive but less threatening, so traders likely took this as a sign that another destructive wave of cases is a less likely scenario for now.

Risk assets seemed to have benefited from this development as expected, with oil and equities taking back much of the losses incurred since the variant was first discovered back in late November. Crypto assets also rallied to recover some losses from the big weekend sell-off thanks to the broad shift to risk-on sentiment, while bonds prices drifted lower in this environment as expected.

The U.S. dollar and gold was mostly choppy despite the risk-on lean, likely due to traders waiting for the latest CPI data from the U.S on Friday. This was the other key risk event for the week as it would likely dictate how traders may position for next week’s bundle of monetary policy statements from top tier global central banks.

The U.S. CPI data came in hotter-than-expected at 6.8% m/m headline and the core read at 4.9% m/m, sparking both the usual and unusual reactions as gold and risk assets popped higher, while bond yields dipped. Further more, the pop in risk assets was short-lived as those trades reversed, suggesting that traders were pricing in rising odds that monetary policy tightening will accelerate, and the rising odds that high inflation and rising interest rates would slow down global growth.

In the foreign currency space, there no surprise catalysts from the forex calendar, while the major points of interest (the Bank of Canada and Reserve Bank of Australia policy statements, and the U.S. CPI read) came in pretty much within expectations. Overall, we saw the usual behavior from traders in a risk-on environment where the “safe haven” currencies under performed the higher-risk currencies.

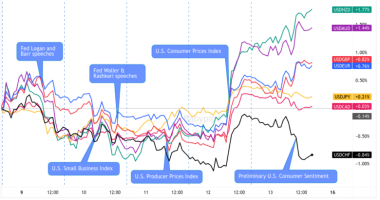

USD Pairs

Job resignations fell by 4.7% to 4.16M; Job openings increased to near all-time highs at 11.03M

U.S. unemployment claims dropped by 43,000 to 184,000 last week

U.S. wholesale inventories accelerated 2.3% vs. 2.2% prev.

The U.S. Senate approved a bipartisan deal to avoid debt ceiling crisis

University of Michigan Consumer Sentiment rises to 70.4 in December vs. 67.4 in November.

GBP Pairs

U.K. Construction PMI rose to 55.5 in November vs. 54.6 in October

BoE’s Broadbent sees inflation above 5% and price pressures coming from the jobs market; refused to say if a rate hike is needed on Monday

Boris Johnson issues work from home guidance on Wednesday to curb Omicron in U.K.

U.K. home prices reached a new record high of £272,992 ($362,708) in November – Halifax

U.K. monthly GDP printed 0.1% uptick in October vs. 0.4% forecast; U.K. manufacturing production flat vs. projected 0.2% increase

EUR Pairs

German factory orders slumped 6.9% vs. projected 0.2% dip

Eurozone Sentix investor confidence index slipped from 18.3 to 13.5

Eurozone Construction PMI in November rose to 53.3 vs. 51.2 in October

German industrial production up by 2.8% in Oct. after 1.1% dip in Sept.

French private payrolls up 0.5% as expected in Q3

German final CPI unchanged at -0.2% as expected

CHF Pairs

Swiss unemployment rate remains unchanged at 2.5% in November 2021

SECO Swiss Economic Forecast: Lowered 2022 growth forecasts to 3.0%; 2.0% for 2023

CAD Pairs

Bank of Canada kept the overnight rate unchanged at 0.25% on Wednesday; committed to no rate hikes until a complete recovery, possibly in 2022

Canada Ivey PMI holds at 61.2 in November

NZD Pairs

New Zealand ANZ commodity prices index up from 2.2% to 2.8%

New Zealand manufacturing sales fell -6.4% in third quarter

New Zealand Business NZ manufacturing index down from 54.2 to 50.6

New Zealand electronic retail spending rises 9.2% in November

AUD Pairs

Australian job advertisements grew 7.4% in November

Australia AIG Services Index rises to 49.6 vs. 47.6 previous

JPY Pairs

Japan’s avg cash earnings up 0.2% in Oct (vs. 0.7% expected, 0.2% in Sept)

Japan’s household spending dips by -0.6% in October, falling for the third straight month due to COVID

Japanese Q3 GDP downgraded to 3.6% year-over-year contraction

Japanese Economy Watchers Sentiment index up from 55.5 to 56.3

Japanese wholesale inflation reached a record high of 9.0% y/y in November