A MONEY expert has revealed their child benefit trick for turning £26 a week in £50,000 after a huge Spring Budget change.

Speaking in the commons yesterday, the Chancellor outlined reforms to the high-income child benefit charge in a big boost for parents.

1

Child benefit is paid to parents to help with the costs of childcare.

From next month, parents can claim £25.60 per week for their first or only child and an extra £16.95 a week for any additional children.

But, as it stands, if either parent or carer starts earning over £50,000, they have to start paying the high-income child benefit charge.

The Chancellor has now confirmed in his Spring Budget that from April the threshold at which parents have to pay the charge will be increased to £60,000.

READ MORE ON CHILD BENEFIT

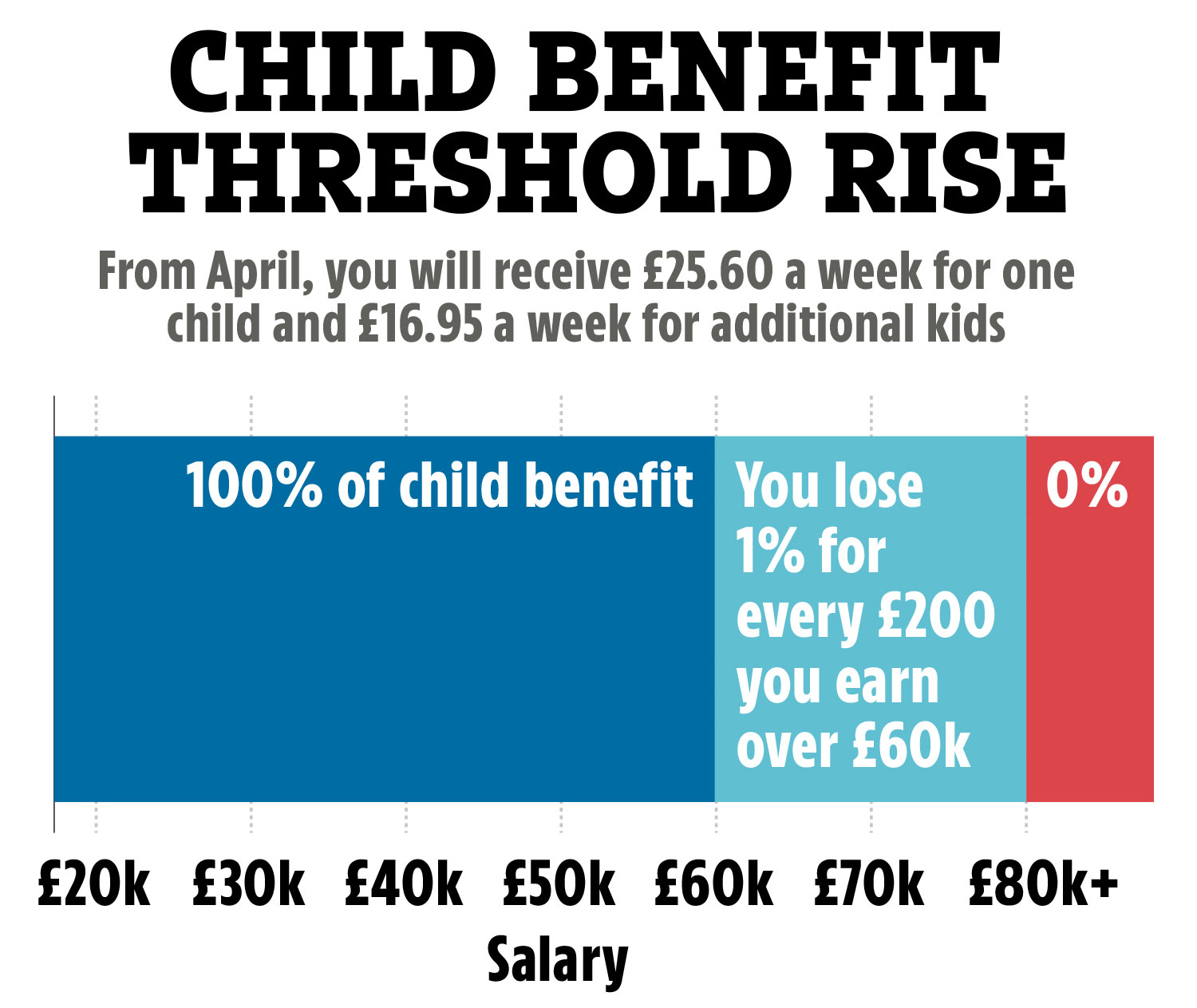

Currently, when you reach a £60,000 salary, you have to repay the full amount of child benefit received.

From April though, in a further boost, the Chancellor announced this will go up to £80,000 to ensure fewer parents are caught out.

It means that parents earning £60,000 will soon be able to keep their entire child benefit payment.

The experts at Hargreaves Lansdown have now outlined how a simple trick could lead to savings of £48,639 for your child.

Most read in Money

From £450 tax cut to child benefit changes, what the Budget means for YOUR finances

If you have one child and newly qualify to keep all of your child benefit, you can invest it every month in a Junior ISA.

A Junior ISA is a tax-free savings account for those aged under 18, where you can squirrel away £9,000 a year.

Sarah Coles, head of personal finance at Hargreaves Lansdown said: “Parenting is getting more rewarding, because from April 6, half a million higher-earning parents are set to lose less of their child benefit – and 170,000 will have it all reinstated.

“But while the £25.60 a week could come in handy if you were to put it into your child’s Junior ISA, it could do so much more.”

She went on to explain that in the coming tax year, child benefit will rise from £24 to £25.60 for the first child, and from £15.90 to £16.95 for a second or subsequent child.

Sarah added: “This sort of sum can make a real difference, especially to those on lower incomes, but it can also quickly disappear.

“If there’s a risk it could end up funding the kind of nice-to-haves that are discarded as quickly as last season’s ‘Fortnite’ skins, it’s worth considering how much difference it could make if you put it to work.”

A Junior ISA is a good option to help build a nest egg for your children to start adult life, she explained.

It’s worth noting, that the nearly £50,000 savings assumes you invest your child benefit every month for 18 years, and that the benefit rises 3% a year, and you get investment returns of 5%.

If you have two children, so get the additional child benefit payments, you could amass £80,843.

Although Sarah pointed out that you may want to divide it equally between your kids to keep it fair.

Bear in mind, that the amount you’ll get depends on how long you save and how much you put in each month.

Plus, this option is only a good idea if you don’t rely on the benefit payments for the day-to-day of caring for your child.

Junior ISAs come in two forms, cash accounts and investment accounts – most people tend to choose a cash ISA.

She said: “Over this kind of period, both returns and charges will make a real difference, so it’s worth considering a stocks and shares ISA rather than a cash ISA, choosing a provider which doesn’t charge for the JISA, and weighing up your investment options carefully.”

Below we reveal how you can open a Junior ISA and further changes on the way for child benefit.

How can I open a Junior ISA for my child?

You can get a Junior ISA from a range of banks, building societies, credit unions, friendly societies and stock brokers.

Contact any of these directly for more information about how you can open a Junior ISA with them.

Make sure you compare different options first, to get the savings account that best suits your needs.

You can use a comparison website such as Compare the Market or Moneysupermarket to do this.

According to MoneySavingExpert.com both Coventry Building Society and Loughborough Building Society have the best rates at 4.95% and 4.8% respectively.

Anyone can pay money into a Junior ISA, but the total amount paid in cannot go over £9,000 in the 2024 to 2025 tax year.

The money belongs to your child and cannot be withdrawn until they turn 18.

Spring Budget at a glance

What other child benefit changes are on the way?

The Chancellor confirmed in his Spring Statement that from April the threshold at which parents have to pay the charge will be increased to £60,000.

As it stands, when you reach a £60,000 salary, you have to repay the full amount of child benefit received.

From April, though, the Chancellor announced this will go up to £80,000 to ensure fewer parents are caught out.

It means that parents will repay 1% for every £200 of income earned over these new thresholds.

Hundreds of thousands of parents will save an average of £1,260 next year.

These changes will come in from April 6 this year.

Speaking in the Commons, the Chancellor acknowledged that the existing child benefit system could be “confusing and unfair” because of how single parents are affected.

So, in a further boost, Mr Hunt said the government will look to change the system to a household-based one by April 2026.

At the moment, child benefit begins being withdrawn when one parent earns over £50,000 a year.

This means two parents earning £49,000 a year – totalling £98,000 in the household – each receive the benefit in full.

Whereas a household earning a lot less than that does not get the full payment if just one of the parents earns over £50,000.

By converting to a household-based system, it would mean parents aren’t caught in the tax trap unnecessarily.

But this change will take time as they are complicated measures.

What is the high-income child benefit charge?

If either parent or carer starts earning over £50,000, they have to start paying the high-income child benefit charge.

This means you have to pay back 1% of your child benefit for every £100 of income earned over the £50,000 threshold.

Once you reach £60,000 of yearly income you have to repay the full amount of child benefit received.

Parents have been caught out by the complicated rules and extra charges and landed with bills for thousands of pounds.

It’s up to parents to notify HMRC if they are liable for the charge and they must file a self-assessment tax return to pay it.

Child benefit

Everything to know about child benefit:

What is child benefit and who is eligible?

Child benefit is paid to parents to help with the costs of childcare.

Payments are usually made every four weeks, plus by claiming child benefit you also get National Insurance credits that count towards your State Pension.

Currently, parents can claim £24 per week for their first or only child – £96 a month and £1,248 a year.

But, from April the rate for your eldest or only child will go up to £25.60 a week – equating to around £102.40 a month or £1,334.86 a year.

For any additional children, they can claim an extra £15.90 a week per child – £63.60 a month and £826.80 a year.

And, from April for every other child, you’ll get £16.95 a week, which is £67.80 a month and £883.82 per year.

You normally qualify for child benefit if you live in the UK and are responsible for a child under 16.

Parents can also claim support for a child under 20 if they are in approved education or training.

When two or more people share the responsibility of caring for a child, it can only be claimed by one person.

You’ll be responsible for a child if you live with them or you are paying at least the same amount as child benefit towards looking after them.

This might mean you are paying the equivalent amount of child benefit on food, clothes or pocket money.

You should bear in mind, eligibility changes if a child goes into hospital or care and if your child starts to live with someone else.

Usually, you get child benefit for eight weeks after your child goes to live with a friend or relative – as long as they don’t make a claim.

But it can continue for longer if you make contributions to your child’s upkeep.

Foster parents can also claim child benefit, as long as the council is not paying anything towards their accommodation or maintenance.

Legal guardians or parents adopting a child can also apply for the benefit, but the child has to be living with them.

You will only be able to claim for a short period if you leave the UK, for example, if you go on holiday or for medical treatment.

For anyone not sure about eligibility, you can contact the Child Benefit Office.

READ MORE SUN STORIES

Meanwhile, here are four ways to avoid the child benefit tax trap – but still gain £1,248 a year in free cash.

Plus, here are 17 big money changes in 2024 and what they mean for you – including a £1,800 pay rise for millions and free childcare.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories.