MILLIONS of households will breathe a sigh of relief as the Bank of England left interest rates unchanged again today.

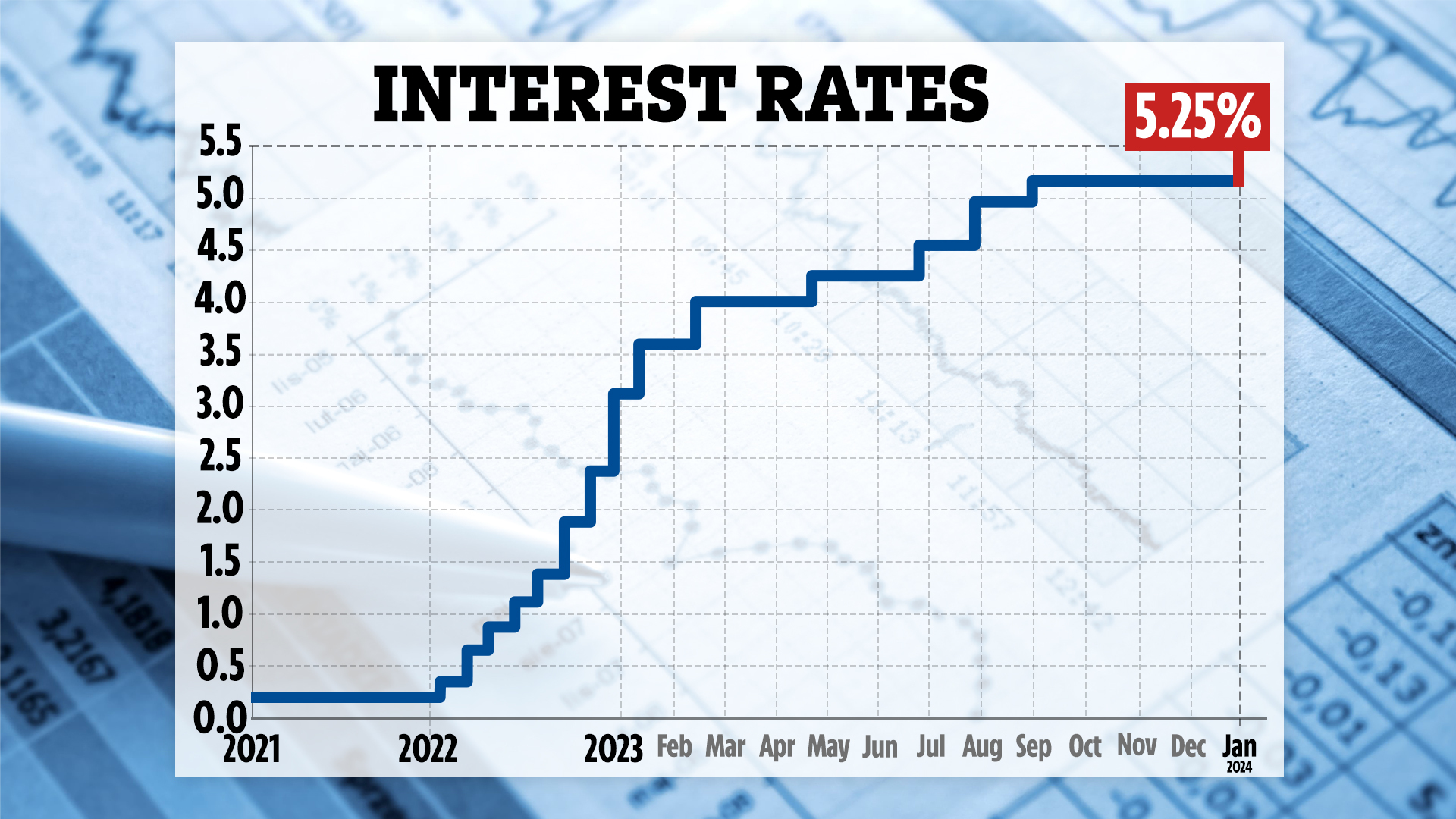

Decision-makers on the Bank’s Monetary Policy Committee (MPC) have now kept interest rates at 5.25% for four consecutive meetings.

1

The MPC voted to retain rates at their current level by a majority of six to three.

Andrew Bailey, the Bank’s Governor, said there had been “good news” on inflation in recent months but that the committee needs to see more evidence that inflation will fall “all the way to the 2% target, and stay there” before it can lower interest rates.

Although the lack of a cut to rates might hit mortgage holders harder, new inflation forecasts from the Bank could relieve households grappling with the cost of living crisis.

The inflation rate is set to fall to 2% between April and June this year, about 18 months earlier than previous forecasts, according to the latest Monetary Policy Report.

Read more in money

However, it will only stay at the target level temporarily before increasing during the second half of the year and could rise to 2.8% by the first three months of 2025.

Andrew Bailey has said that he and his colleagues “need to see more evidence” that inflation is going to stay around 2% before they start cutting interest rates.

“Today, we’ve decided to hold interest rates at 5.25%. We have had good news on inflation over the past few months,” he said.

“It has fallen a long way, from 10% a year ago to 4%.

Most read in Money

“But we need to see more evidence that inflation is set to fall all the way to the 2% target, and stay there, before we can lower interest rates.”

Energy prices are expected to be a key driver of the level of inflation throughout the year.

High street banks use the base rate to set the rates they offer to customers on things like loans, savings and mortgages.

Higher interest rates are bad news for households because it makes mortgage bills more expensive.

But freezing mortgage rates is good news for homeowners facing crippling repayments.

What it means for your money

Below we reveal more about what the rate hold means for your money.

Mortgages

Usually if rates rise it means that mortgage bills, depending on the type you have, will increase.

Those on a fixed-rate deal tend to be safe for now until they remortgage.

But other mortgages, such as a tracker or standard variable rate (SVR) mortgage, can be impacted straight away.

Homeowners on variable-rate mortgages might not see their repayments go up straight away, but they likely increase shortly after interest rates are hiked.

But the exact amount depends on your borrowing and your loan-to-value.

However, because the BoE has opted to freeze current rates, your lender may opt to do nothing at all.

Your bank should warn you of any increase to your rate before it goes up.

We’ve got more info on how to find the best mortgage rate deal here.

Credit card and loan rates

Again the cost of borrowing through loans, credit cards and overdrafts can go up if the base rate is hiked, as banks are likely to pass on the increased rate.

Certain loans you already have, like a personal loan or car financing, will usually stay the same anyway, as you’ve already agreed on the rate.

But rates for any future loan could be higher, and lenders could increase the rate on credit cards and overdrafts – although they must let you know beforehand.

But nothing is likely to change for now because of the rate hold.

However, you can still cancel a credit card if you want and will have 60 days to pay off any outstanding balance.

Savings rates

Savers are the main group to have benefited after the consecutive rate rises.

Banks tend to battle it out by offering market-leading interest rates.

Although banks are usually much slower to act than when passing on higher rates for borrowing.

READ MORE SUN STORIES

Of course, because the rate will not change, banks will likely take advantage and keep their rates the same, too.

Anyone currently getting a low rate on easy-access savings could find it’s worth looking around for a better rate and moving their money.