Escalating tensions in Ukraine and resilient economic data from the major economies got traders pricing in higher interest rates and risk aversion.

No wonder commodity-related currencies like NZD tanked while safe havens like the Swiss franc and gold gained ground!

Not sure what I’m talking about? I can explain, but lemme show you the biggest headlines first:

Notable News & Economic Updates:

? Broad Market Risk-on Arguments

ECB Governing Council member Klaas Knot said monetary tightening beyond next week’s meeting is anything but guaranteed

New Zealand’s CPI up by 1.1% q/q in Q2 2023 vs. 1.2% in Q1, 0.9% expected. Annual CPI dropped from 6.7% to 6.0% in Q2 thanks to lower petrol prices and higher interest rates

U.S. Retail Sales for June: 0.2% m/m (0.3% m/m forecast; 0.5% m/m previous); core Retail Sales was inline with expectations at 0.2% m/m (0.3% m/m previous)

Falling fuel prices dragged the U.K.’s consumer prices from 8.7% y/y to 7.9% y/y in June. Core CPI also eased from 7.1% y/y to 6.9% y/y.

Canada CPI for June 2032: 2.8% y/y (3.0% y/y forecast; 3.4% y/y previous); led by falling energy costs to a 27-month low; core CPI fell to 3.2% y/y (3.6% y/y forecast) vs. 3.7% y/y previous

PBoC raised a parameter on cross-border corporate financing under its macro-prudential assessments (MPA) to 1.5 from 1.25, allowing companies to borrow more overseas in proportion to their assets

Australia added net 32.6K jobs in June vs. 15K expected, 76.6K previous. Unemployment rate dipped from 3.6% to 3.5% as the participation rate edged 0.1% lower to 66.8%

Euro Area Flash Consumer Confidence for July 2023 improved by 1 point to -15.1, continuing its slow recovery since 2022 low levels around -30

Australia’s quarterly NAB survey showed business confidence rising 1pt to -3 while business conditions dropped 8 pts to +9 as businesses “moderated considerably” in Q2

Sources familiar with the Bank of Japan said that the BOJ is likely leaning towards keeping yield control steady next week

? Broad Market Risk-off Arguments

China’s GDP grew by 0.8% in Q2 2023, slower than the 2.2% quarterly growth in Q1. Annual GDP came in at 6.3%, faster than Q1’s 4.5% uptick but slower than the 7.1% growth expected

China’s retail sales slowed down from 12.7% to 3.1% y/y in June

New Zealand Services PMI fell to 50.1 in June (52.5 forecast) from a revised 53.1 previous read; Employment index fell to 49.1 vs. 52.3 previous; New orders dipped to 51.3 vs. 55.4 previous

RBA’s July meeting minutes showed that the Board agreed that “some further tightening may be required” and hints at revisiting the rate hike move at the August meeting

Wheat prices soared after Russia ended grain deal with Ukraine, warned it would treat ships heading for Ukrainian ports as potential military targets

Canada retail sales for May 2023: 0.2% m/m (0.5% m/m forecast; 1.0% m/m previous); core retail sales was 0.0% m/m (0.3% m/m forecast; 1.2% m/m previous)

Japanese government downgraded its economic outlook on Thursday from 1.5% for fiscal year ending March 2024 to 1.3%; raised its 2023 consumer price inflation forecast to 2.6% from 1.7% prior

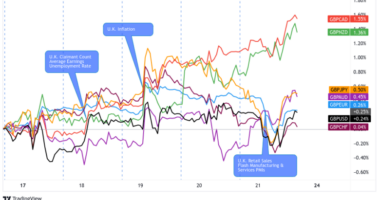

Global Market Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TV

Global markets started the week on shaky ground on Monday when China – the world’s second-largest economy – released its Q2 2023 GDP read at 6.3% y/y, below expectations of 7.1% annual growth.U.S. Treasury Secretary Janet Yellen piled on to global growth fears later that day when she said that “slow growth in China can have some negative spillovers for the U.S.”

It’s like she was laying the ground for gloomy vibes ahead of the Oppenheimer weekend!

With Japanese and Hong Kong markets closed on Monday, China-related currencies like AUD and NZD saw steady-ish downswings during the Asian and European sessions.

Interestingly, U.S. equities gained ground as traders focused on Friday’s “peak inflation” and “peak interest rates” themes.

Meanwhile, U.S. crude oil prices traded below $74 on China’s weak growth and rumors that two of three of Libya’s oil fields would resume production and add about 370,000 oil barrels per day.

On Tuesday, the U.S. retail sales data inspired all kinds of shenanigans for the global assets. See, both headline and core retail activity grew by 0.2% in June, which was apparently not low enough to inspire hard landing concerns but also not high enough to support more hawkishness among Fed members.

High-yielding currencies like AUD, NZD, GBP, and BTC remained on “China growth watch” and extended their downswings. On the other hand, CHF and European and U.S. equities traded higher as traders priced in the “peak interest rate” bets for the Fed.

U.S. crude oil also recovered all of its intraweek losses while spot gold jumped to a one-month high near $1,985.

Inflation was the name of the game on Wednesday, and it started with New Zealand printing a 6.0% y/y growth in Q2. While it’s slower than Q1’s 6.7% uptick, it was still high enough above the RBNZ’s 1%-3% target range that the central bank can maintain its hawkish stance.

NZD spiked higher before overall risk aversion during the Asian session dragged it back down to its intraweek lows.

Then, the U.K.’s CPI dropped and so did the British pound and global bond yields. See, U.K.’s inflation slowed down from 8.7% y/y to 7.9% y/y, while the core CPI dipped from 7.1% y/y/ to 6.9% y/y.

The optimism over cooling U.K. inflation and the upcoming U.S. earnings reports helped boost U.S. equities in the late European/early U.S. session trading.

Risk sentiment soured before the day ended, however, thanks to Russia warning that ships heading for Ukrainian ports (including wheat-carrying ones!) could be considered potential military targets.

It also didn’t help risk sentiment that Netflix’s projected Q3 revenue missed analysts’ estimates while Tesla reported lower profitability in Q2.

Risk assets took more hits on Thursday, and it’s probably because of better-than-expected data.

What’s up with that?!

Meanwhile, the People’s Bank of China (PBoC) set a much weaker USD/CNY fixing AND adjusted its financing rules so that companies could borrow more through cross-border financing.

AUD and NZD traded higher while safe havens like USD and CHF lost pips until the U.S. session when the U.S. printed its jobless claims data.

Turned out, there were “only” 228K initial jobless claimants in the U.S. last week, lower than the 239K claimants analysts had estimated. Traders who priced in “peak rate” bets from the major central banks were shook and they scaled back their “risky” holdings.

USD and 10-year Treasury yields popped up, U.S. equities struggled for direction, and crude oil, BTC/USD, and spot gold dropped sharply.

Friday was light on major catalysts, probably with exception to the Japanese national core CPI update. It came in a tick above the previous read at 3.3% y/y, which based on the fall in the yen is apparently not enough to get the BOJ to make any changes to yield curve control at their next meeting.

But overall, it looks like risk-on players held their ground going into the weekend. Oil shot up further to break the $77/barrel market, bitcoin recovered from the previous day’s drop to retest the $30K handle, and equities marched higher while gold took a dip into the Friday close.