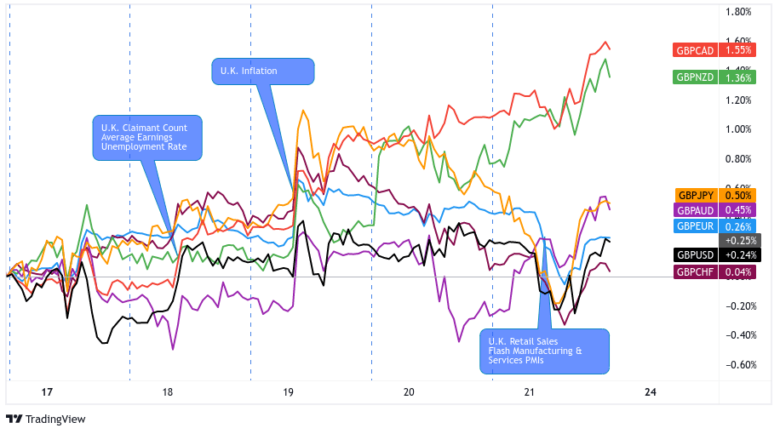

We’ll get the latest U.K. inflation update on Wednesday, which has been an influence on the Bank of England’s monetary policy decisions and the British pound as of late.

Check out all of the important data to consider before putting together your latest trade idea!

Event in Focus:

U.K. Inflation updates: Consumer Prices, Producer Prices

When Will it Be Released:

May 24, 2023, Wednesday: 6:00 am GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

U.K. CPI annual rate: 8.5% y/y forecast vs. 10.1% y/y previous

U.K. CPI monthly rate: 1.0% m/m forecast vs. 0.8% m/m previous

U.K. core CPI annual rate: 6.1% y/y forecast vs. 6.2% y/y previous

U.K. PPI Input annual rate: 5.2% y/y forecast vs. 7.6% y/y previous

U.K. PPI Output annual rate: 5.9% y/y forecast vs. 8.7% y/y previous

Relevant Data Since Last Event/Data Release:

? Arguments for a potential uptick in rate of inflation / Bullish GBP

Global / CIPS UK Services PMI for April: 55.9 vs. 52.9; “a combination of stronger demand and rapidly rising business expenses led to a faster rate of prices charged inflation”

Nationwide: U.K.’s house prices rose by 0.5% m/m in April, the first increase in eight months. Annual growth improved from -3.1% to -2.7%.

U.K. BRC Shoprice index rose by 15.7% in April, Food inflation accelerated to 15.7% vs. 15% in March

? Arguments for a potential downtick in rate of inflation / Bearish GBP

Global / CIPS UK Manufacturing PMI for April: 47.8 vs. 47.9 in March; “Rates of increase in average input costs and output charges both eased in April, falling to 35- and 28-month lows respectively”

Property website Rightmove: Average asking prices for properties up by 0.2% m/m in April, less than the 1.2% gain seen at this time of last year.

U.K. claimant count increased by 46.7K versus the expected 31.2K figure in April, adding to the previous 28.2K rise in joblessness; unemployment rate ticked higher to 3.9% vs. 3.8% forecast/previous

Previous Releases and Risk Environment Influence on the British Pound

April 19, 2023

Action / results:

U.K. headline CPI for March ticked lower to 10.1% y/y from 10.4% y/y in February vs. estimated slowing to 9.8%, U.K. core CPI up from 5.8% y/y to 6.2% y/y vs. estimated rate of 6.0% y/y.

The British pound jumped roughly between 0.30% to 0.50% against the majors on the event, and was able to hold those gains through the Wednesday and Thursday session, despite a broad risk-off environment.

Risk environment and intermarket behaviors:

Risk sentiment was broadly negative on the week as fresh global data pointed to higher odds of central banks maintaining hawkish monetary policies to fight inflation.

Mar 22, 2023

Action / results:

U.K. headline CPI jumped from 10.1% to 10.4% year-over-year in February vs. estimated dip to 9.9%, U.K. core CPI up from 5.8% to 6.2% year-over-year in February vs. estimated drop to 5.7%

The British pound jumped roughly between 0.05% to 0.50% against the majors on the event, a relatively tame reaction, likely due to traders taking quick profits or repositioning for the Bank of England statement that was to come just a day after.

Risk environment and intermarket behaviors:

Risk sentiment was broadly positive this week, generally a reaction to positive news (e.g., UBS takes over Credit Suisse, central banks shore up U.S. dollar liquidity) on the negative banking sector events that dominated headlines in March. Risk assets were up while the Dollar and gold spent most of the week in the red.

Price action probabilities:

Risk sentiment probabilities:

Broad risk sentiment behavior will likely be dominated by developments in the U.S. debt ceiling deal story. After what appeared to be a resolution to come this past weekend, we’re back to a high level of uncertainty as officials meet once again to try and get over the last hurdles.

Until a deal does come through (or if talks fall apart and a default looks certain), it’s likely price behavior will remain choppy as it has been throughout May, setting up what could be an explosive breakout of volatility when we finally do see a resolution to this story.

Aside from the U.S. debt ceiling story, the next likely catalyst for broad risk sentiment will be the latest round of global business survey updates. This will give traders the freshest look on whether or not price inflation rates and employment conditions may really be topping out across the globe.

British Pound scenarios:

Base Scenario:

If U.K. inflation data generally comes inline with expectations or lower, probabilities rise that the British pound may see selling pressure as the odds rise that the Bank of England will pause on tightening policy, or at the very least prompt BOE members to highlight peak inflation conditions in the weeks ahead.

Prices tend to consolidate ahead of this event, making a potential downside breakout a setup to watch out for if this event scenario plays out. The odds rise of a downside breakout grows if Sterling trends or leans higher ahead of the event.

In this scenario, short GBP opportunities should be looked into further, and if risk sentiment is leaning negative due to negative U.S. debt ceiling developments, JPY, USD, and CHF may be the best options to trade against in the short-term.

Alternative Scenario:

If U.K. inflation data surprises traders with a higher-than-expected/previous read (a scenario we have seen in the past), probabilities rise that the British pound may see some buying pressure as expectations will likely rise that the Bank of England may have to keep monetary policy tight.

And if Sterling prices are consolidating ahead of the event, then an upside break out scenario is one to look out for, especially if there is a bearish lean on Sterling before the data release.

In this range of scenarios, and if broad risk sentiment is net negative, long GBP opportunities may be best against the comdolls, but don’t leave out JPY and CHF from your scan. The interest rate divergence is wide enough with those two currencies to potentially attract some Sterling buyers in this alternative scenario.