Currency performance was pretty mixed this week, likely the result of traders balancing U.S. dollar dominance & individual currency narratives.

But after a big Dollar pullback on Thursday that it couldn’t fully recover from, the Kiwi dollar was able to snatch the top spot away from the Greenback at the Friday close. Meanwhile, the Swiss franc fell to last place, likely still having bearish vibes after last week’s interest rate hold from the Swiss National Bank.

Missed the major forex headlines? Here’s what you need to know from this past week’s FX action:

USD Pairs

Overlay of USD vs. Major Currencies Chart by TradingView

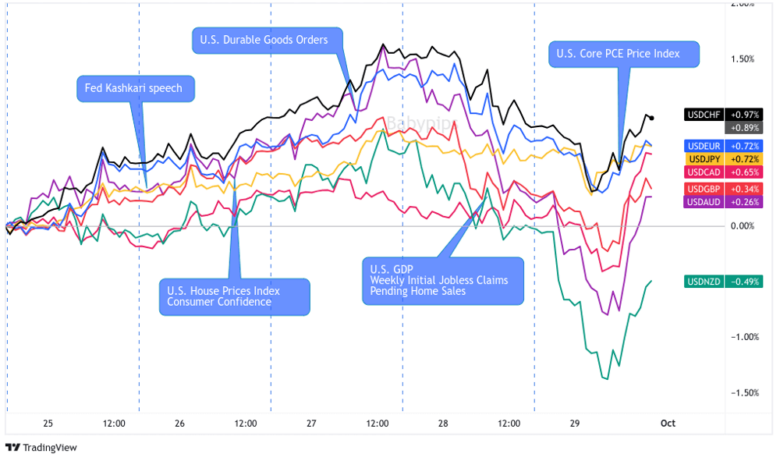

Well, well, well, the good ol’ U.S. dollar has been quite the drama queen this week, following its “higher for longer” script set by the FOMC last week. And guess what? The plot thickened thanks to commentary from FOMC member Kashkari, who seems to believe that there’s some chance that the Fed may push interest rates even higher if warranted.

But wait, the dollar had a sudden change of heart on Thursday, and we’re not entirely sure why. Maybe it saw the Euro flexing its muscles and got a bit scared, or perhaps it just decided it was time to take a breather (i.e., profit taking) before the month and quarter ended. Who knows? The dollar can be a bit of a diva at times.

And just when you thought the dollar was down for the count, the bulls came charging back on Friday. It’s almost as if they were waiting for the perfect moment, which conveniently coincided with the release of the Core PCE Price Index.

The results? Well, let’s just say it was as mixed as a bag of nuts at a party – monthly changes were below expectations, but the year-over-year data continued to show that high inflation environment is sticking around like that one friend who never leaves the party.

In the end, the dollar managed to regain ground against the major currencies, but it seems the New Zealand dollar had other plans – probably off on a “Lord of the Rings” adventure or something.

🟢 Bullish Headline Arguments

Federal Reserve Bank of Chicago President Austan Goolsbee said on Monday that it is possible for the U.S. to avoid recession despite rising interest rates

FOMC member Kashkari shared that he’s “one of those folks” who favor higher and higher for longer interest rates, and shared that there’s a 40% chance the Fed would “push the federal funds rate higher, potentially meaningfully higher”

U.S. Durable Goods Orders for August: 0.2% m/m (-1.4% m/m forecat; -5.6% m/m previous); Core Durable Goods Orders came in at 0.4% m/m (0.6% m/m forecast; 0.1% m/m previous)

U.S. weekly initial jobless claims: 204K (205K forecast; 202K previous)

U.S. Core PCE Price Index for August: 3.9% y/y (3.8% y/y forecast; 4.3% y/y previous)

🔴 Bearish Headline Arguments

U.S. Pending Home Sales: -7.1% m/m (0.2% m/m forecast; 0.5% m/m previous)

U.S. Core PCE Price Index for August: 0.1% m/m (0.2% m/m forecast / previous)

U.S. GDP, final read for Q2 2023: 2.1% (2.1% forecast; 2.2% previous); PCE Price Index: 2.5% q/q as forecast; Core PCE Prices 3.7% q/q as forecast vs. 5.0% q/q

Fed’s Barkin says it’s too early to know if more rate hikes are needed

EUR Pairs

Overlay of EUR vs. Major Currencies Chart by TradingView

ECB President Lagarde reiterated on Monday that interest rates will stay high for as long as needed, but that was no help to the bulls as the euro got almost no love this week. This was likely due to a mix of the U.S. dollar strength environment, and a continued flow of weak economic and sentiment updates from the euro area, mainly from Germany.

The bulls did get a brief moment of love on Thursday as Euro area CPI updates did show signs of sticky inflation conditions, but it wasn’t enough get the the euro in the green against most of the majors.

🟢 Bullish Headline Arguments

On Monday, ECB President Lagarde restated that the level of interest rates will stay restrictive for as long as needed to slowdown high inflation

Spain’s CPI accelerated from 5.9% y/y to 4.2% y/y in September

Germany Import Prices for August: 0.4% m/m (0.3% m/m forecast; -0.6% m/m previous)

Euro Area Flash CPI for September: 4.3% y/y (4.7% y/y forecast; 5.2% y/y previous

🔴 Bearish Headline Arguments

IfO German business climate index dipped slightly from 85.8 to 85.7; “The German economy appears to have bottomed out”

INSEE: France consumer confidence remained at a four-month low of 83 in September

Germany’s GfK consumer sentiment deteriorated from -25.6 to 26.5 in September; “Private consumption will not be able to positively contribute to overall economic development this year.”

Euro area annualized growth rate of broad monetary aggregate M3 in August: -1.3% y/y; Growth rate of total credit to euro area residents in August: -0.2% y/y vs. 0.1% y/y in July

North Rhine Westphalia (Germany) CPI slowed down from 0.5% m/m to 0.2% m/m in September

Germany Preliminary CPI read for September: 0.3% m/m (0.5% m/m forecast; 0.3% m/m previous); 4.5% y/y (4.8% y/y forecast; 6.1% y/y previous)

Germany Retail Sales for August: -2.3% y/y (-1.0% y/y forecast; -2.2% y/y previous)

GBP Pairs

Overlay of GBP vs. Major Currencies Chart by TradingView

Ah, the British pound, the currency that’s sometimes as unpredictable as the British weather! Its price action this week was like trying to guess whether it’s going to rain or shine in London, an unsurprising outcome given the lack of catalysts for most of the week. On Friday, the U.K. released a slew of data, which was weaker-than-expected overall, and seems to have been a net negative on the currency during the Friday London session.

🟢 Bullish Headline Arguments

U.K. Distributive Trades: -14.0 (-23.0 forecast; -44.0 previous)

🔴 Bearish Headline Arguments

U.K. Current Account for Q2 2023: -25.29B (-12.1B forecast; -15.16B previous)

U.K. GDP Final read for Q2 2023: 0.2% q/q as forecasted vs. 0.3% q/q previous

U.K. Mortgage Approvals for August: 45.4K vs. 49.5K previous

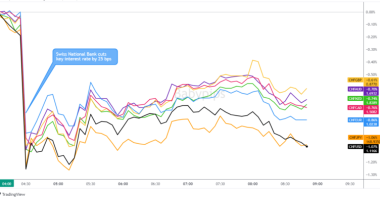

CHF Pairs

The Swiss Franc had another downer week, arguably due to counter currency strength, tracking the euro lower, and possibly continued disappointed from the Swiss National Bank holding interest rates at 1.75% last week. It was the biggest loser as it closed red against all of the major currencies on Friday.

🟢 Bullish Headline Arguments

Credit Suisse: Swiss investors’ sentiment improved from -38.6 to -27.6 in September, the highest in seven months

🔴 Bearish Headline Arguments

Swiss National Bank Quarterly Bulletin: SNB keeps policy rate at 1.75% to counter inflationary pressure. The SNB is open to further tightening if needed and willing to intervene in forex markets. Deposits will be remunerated at 1.25% above a certain threshold.

AUD Pairs

Overlay of AUD vs. Major Currencies Chart by TradingView

The Aussie dollar was mixed but net red to start the week, only seeing gains against the euro and franc through the Wednesday trading session.

But the tone changed quickly to bullish going into Thursday, despite a slowdown in the growth of retail sales update from Australia.

pThis could have been a delayed reaction to the surprise higher-than-expected Australian CPI update, and/or catalysts from China including better-than-expected Chinese data, as well as continued efforts in China to support their economy, again, the largest trading partner of Australia.

Risk sentiment also broadly shifted slightly positive on Thursday during the U.S. session, possibly sparked by another positive U.S. employment update, to likely draw in some long AUD traders back at lower prices.

Whatever the case may be, the Aussie managed to end the week as a net winner among the majors, only falling to the Greenback and Kiwi.

🟢 Bullish Headline Arguments

Higher fuel prices boosted Australia’s CPI from 4.9% y/y to 5.2% y/y in August as expected, adding to rate hike speculations for next month

Australia’s private sector borrowing accelerated from 0.3% m/m to 0.4% m/m in August

China’s industrial profits fell by 11.7% ytd/y in August, a bit better than the 15.5% ytd/y decline in July, as government support measures helped stabilise parts of the economy

🔴 Bearish Headline Arguments

Australia’s retail sales slowed down from 0.5% m/m to 0.2% m/m in August as consumers reacted to higher living expenses and borrowing costs

CAD Pairs

The Canadian Dollar closed the week on a downswing, arguably ending up as a slight net loser on the Friday close. Canadian data updates were all positive relative to expectations, and likely why the Loonie saw green early in the week. So the fall may have been due to the pullback in oil prices on Thursday and Friday, and possible traders taking profit from a strong September rally in the Loonie against the majors.

🟢 Bullish Headline Arguments

Preliminary Canada Manufacturing Sales for August: 1.0% m/m (0.7% m/m forecast; 1.6% m/m previous)

Preliminary Canada Wholesale Sales for August: 2.6% m/m vs. 0.2% previous

Canada GDP for July: 0.0% m/m as forecasted (-0.2% m/m)

NZD Pairs

The New Zealand closed out this week as the top dog among the currency majors. Data was very light from New Zealand, but they did come positive to possibly have drawn in fundamental buyers to add to the bullish vibes in the Kiwi.

The likely big driver for the Kiwi’s gains may have also been the dwindling fears in the Asia region, after positive Chinese data and supportive action from the Chinese government and state banks hit the wires this week.

🟢 Bullish Headline Arguments

New Zealand’s business confidence index turned positive, up from -3.7 to 1.5 in September; Jury remains out on whether prices are falling “fast enough to bring core inflation pressures down in a timely fashion”

ANZ-Roy Morgan Consumer Confidence for September: 86.4 (81.5 forecast; 85.0)

JPY Pairs

The Japanese yen was mostly mixed this week but ended up a net loser as risk sentiment shifted less negative on Thursday and Friday. Traders were likely trying to balance out shifting broad risk sentiment with constant jawboning from Bank of Japan members, who were trying to turn back the excessive weakness seen recently in the yen, especially against the U.S. dollar.

🟢 Bullish Headline Arguments

BOJ Gov. Ueda hinted that they’re looking at strong wage and consumption rather than cost pressures from rising import costs for clues on their monetary policy outlook

Japan’s services producer price index accelerated from 1.7% y/y to 2.1% y/y in August

BOJ’s core CPI maintained its 3.3% y/y growth (vs. 3.2% expected) in September

BOJ’s meeting minutes showed the members’ deviating views on when they should exit their easy monetary policies

Japan’s retail sales unchanged at 7.0% y/y in August (vs. 6.6% expected); monthly retail activity edged up by 0.1% after a 2.2% growth in July

🔴 Bearish Headline Arguments

Tokyo’s core CPI rose 2.5% y/y in September (vs. 2.6% expected, 2.8% previous)

amidst some cooling in consumer spending

Japan’s unemployment rate remained at 2.7% in August (vs. 2.6% expected) as the number of unemployed rose by another 10K

Japan’s consumer confidence worsened for a second consecutive month, down from 36.2 to 35.2 in September, with all sub-indices registering decreases

Japan’s housing starts dropped by 9.4% y/y in August (vs. -8.7% expected, -6.7% previous); new construction contracted in all categories including owned, issued, rented, and built for scale

The BOJ announced an unscheduled bond-purchase operation. The central bank bought 300B JPY ($2B) worth of 5 to 10-year bonds in a bid to slow rising bond yields