The U.S. dollar continued to lose pips against its major counterparts as more traders digested the Fed’s less hawkish than expected policy decision.

Other major financial assets and dollar counterparts were more mixed as they reacted to both the dollar’s trends and their individual drivers.

Here’s what you missed from yesterday’s markets!

Headlines:

- Switzerland’s inflation unexpectedly accelerated from 0.0% to 0.3% in April – bringing the annualized CPI from 1.2% to 1.4% – due to rising prices for international package holidays and air transport

- Switzerland’s Procure manufacturing PMI for April: 41.4 (45.5 expected, 45.2 previous); “The PMI pointed to a bifurcation of the Swiss economy: robust services but weak manufacturing”

- France’s final HCOB manufacturing PMI for April revised higher from 44.9 to 45.3 (no changes expected)

- Germany’s final HCOB manufacturing PMI for April revised slightly higher from 42.2 to 42.5 (no changes expected)

- Eurozone’s final HCOB manufacturing PMI for April revised higher from 45.6 to 45.7 (no changes expected)

- The U.S. Challenger Report noted that U.S.-based employers announced 64,689 job cuts in April, a 28% decrease from March’s figure. Companies have announced 4.6% fewer job cuts through April last year.

- U.S. weekly initial jobless claims printed another 208K reading (vs. 212K expected) in the week ending April 27

- U.S. preliminary nonfarm productivity in Q1: 0.3% q/q (0.8% expected 3.5% previous); Preliminary unit labor costs in Q1: 4.7% q/q (3.6% expected, 0.4% previous)

- BOC Gov. Macklem said Canada’s interest rates don’t need to be the same as the U.S. rate but that “there’s a limit to how far they can diverge,” qualifying that “we’re certainly not close to that limit.”

- U.S. factory orders for March: 1.6% m/m as expected (1.2% previous), boosted by demand for commercial aircraft and motor vehicles

Broad Market Price Action:

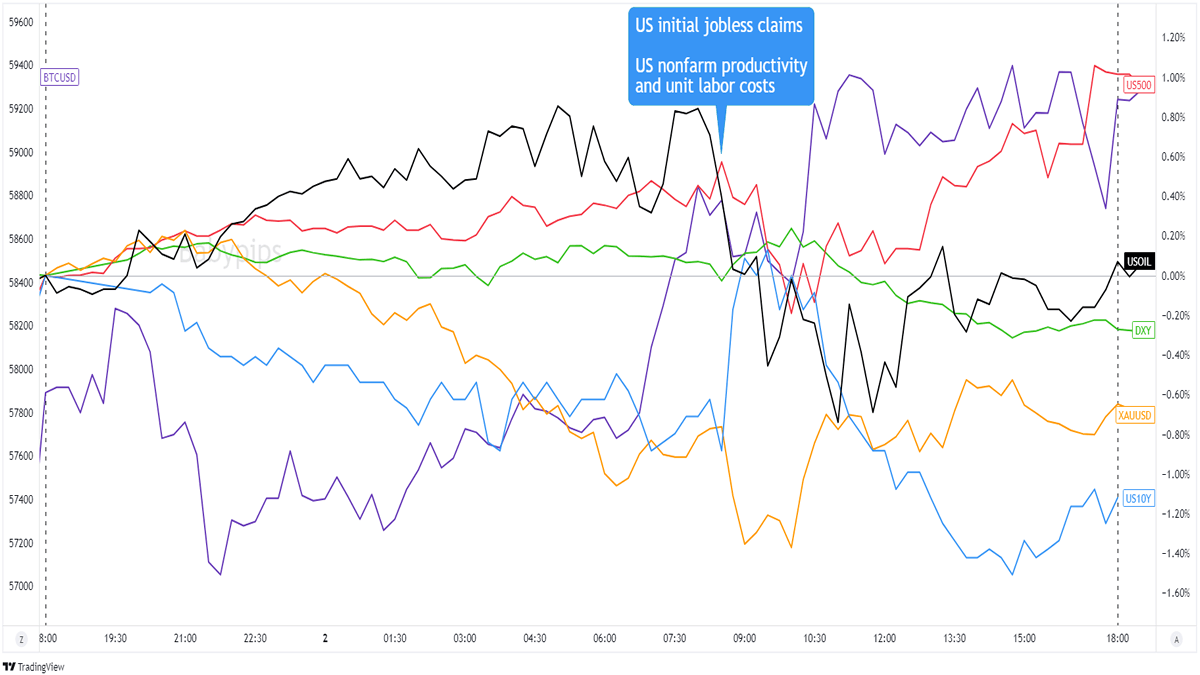

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major financial assets continued to react to Fed Chairman Powell’s pushback against interest rate hikes amidst a sticky high inflation environment.

Spot gold did give up some of its post-FOMC gains and made its way to $2,290 before getting support during the U.S. session but bitcoin (BTC/USD) saw an intraday uptrend after falling sharply early in the day.

The U.S. dollar was treading water all day until a quarterly productivity and unit labor costs report pointed to a tight labor market but also inspired concerns of slower hiring in the next few months. The Greenback and U.S. 10-year bond yields weakened through the U.S. session while counterparts like spot gold, crude oil, and U.S. stock indices saw gains.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

Except for speculations around another Japanese currency intervention and a spike lower against CHF following a stronger-than-expected Swiss CPI report, the U.S. dollar was trading in tight ranges against its counterparts.

The plot thickened during the U.S. session when the quarterly non-farm productivity and unit labor cost reports pointed to a tight labor market. The dollar found support for a while before traders started worrying about a future slowdown in hiring and Friday’s U.S. NFP report release.

USD lost pips across the board and capped the day in the red against its major counterparts.

Upcoming Potential Catalysts on the Economic Calendar:

- Japan and China’s markets out on bank holiday

- France’s government budget balance at 6:45 am GMT

- France’s industrial production at 6:45 am GMT

- Spain’s unemployment change at 7:00 am GMT

- U.K.’s final services PMI at 8:30 am GMT

- Euro Area’s unemployment rate at 9:00 am GMT

- U.S. NFP reports at 12:30 pm GMT

- U.S. final services PMI at 1:45 pm GMT

- U.S. ISM services PMI at 2:00 pm GMT

It’s NFP day for U.S. session traders! U.S. labor market numbers will be under the spotlight as traders try to see how the reports would affect the Fed’s monetary policy biases.

The final S&P services PMI and U.S. ISM services PMI scheduled a few minutes from the NFP reading may also get attention so make sure you’re glued to the tube during the report releases!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!