The Australian dollar took the top spot among the FX majors in the first week of 2023 trading.

The Aussie likely benefited from fresh global data and headlines supporting the idea that central banks could potentially ease tightening regimes soon as recessionary conditions grow and signs of inflation peaking.

Notable News & Economic Updates:

J.P.Morgan Global Manufacturing PMI dropped to a 30-month low of 48.6 in December

On Monday, the IMF warned that a third of the world may enter a recession this year.

S&P Global PMI Commodity Price Pressures Index dipped to 0.3; Global supply shortages index fell to 2.2

FOMC minutes from the December meeting signaled scope for higher rates for “some time” ahead

U.S. Energy Information Administration (EIA) reported an oil inventory increase of 1.7M barrels for the week to December 30.

Euro Area CPI rose by 9.2% y/y in December 2022 vs. 9.5% y/y forecast; Core inflation hits record-high of 5.2% y/y

U.S. Non-Farm Payrolls rose 223K in December 2022 and the pace of wage growth cooled to prompt bets that Fed will slow pace of rate hikes

Intermarket Weekly Recap

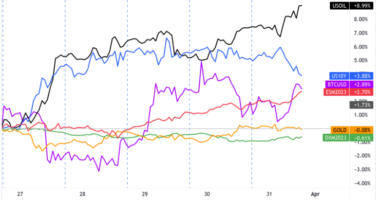

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour by TradingView

Based on the chart above, the big price movers of the week was oil and bond yields after taking a big dip on Tuesday and Wednesday.

This was likely a reaction to IMF warnings of weaker growth, as well as continued rising COVID cases in China. Bond yields likely drew in additional influences from weakening inflation data from Europe and wage data from Japan and the U.S.

On Thursday there was a noticeable reaction in the financial markets during the U.S. trading session, which correlated with the release of better-than-expected U.S. employment data (ADP Non-Farm Payrolls and Unemployment Claims).

And based on the jump in U.S. dollar and bond yields vs. dip in equities, it looks like traders once again took the strong labor market data as a potential argument for the Federal Reserve to stay hawkish on monetary policy.

On Friday, we got the main economic event of the week, he U.S. government report on employment, which confirmed the ADP’s strong jobs survey by coming in better-than-expected at 223K net job adds in December.

But the big takeaway from the event appears to be the slowdown in the wages growth rate, prompting a big rally in equities and fall in bond yields/Greenback. The idea is that a slowdown in wages gives the Fed a little bit of room to be less hawkish on rate hikes as lower wages may lead to lower inflation rates down the road.

In FX, the U.S. was the big winner of the week, at least until the Friday U.S. employment report showed a slower pace of wage growth. After the event, the Australian dollar took the top spot into the weekend, likely a beneficiary of the risk-on sentiment that a scenario of slowing rate hikes brings.

Overall, risk assets benefited from this week’s catalysts, but probably more so on a weaker U.S. dollar as evidenced by gains in gold, bitcoin and equities into the Friday close.

USD Pairs

S&P Global U.S. Manufacturing PMI dipped to 46.2 in December from 47.7 in November

ISM Manufacturing PMI for December dipped to 48.4 vs. 49.0 in November

The Job Openings and Labor Turnover Survey showed 10.46M openings in November, above the 10M forecast and slightly below the 10.51M read in October

FOMC minutes signaled scope for higher rates for “some time” ahead

U.S. private payrolls in December rose by 235K, well ahead of the 153K forecast – ADP

Federal Reserve Bank of Kansas City President Esther George forecasted that interest rates will reach over 5% and “staying there for some time”

S&P Global U.S. Services PMI in December: 44.7 vs. 46.2 in November

U.S. Non-Farm Payrolls rose 223,000 in December 2022 and the unemployment rate fell to 3.5% from 3.6%; the pace of wage growth cooled to 0.3% vs. 0.4% previous

Atlanta Federal Reserve President Raphael Bostic said that the December employment report doesn’t change his view that interest rates will continue to rise and likely sustain above 5%

GBP Pairs

U.K. manufacturing PMI for December fell to 45.3 vs. 46.5 in November

The Bank of England revealed on Wednesday that the number of U.K. mortgages issued dropped more than anticipated to 46,100 from 57,900 in October.

S&P Globa/CIPS U.K. Services PMI for December: 49.9 vs. 48.8 in Nov.

Halifax: UK’s house prices fell by 2.5% in the three months to December, the biggest drop since February 2009

U.K. Construction PMI for December 2022: 48.8 vs. 50.4 November

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

S&P Global Germany Manufacturing PMI in December: 47.1 vs. 46.2 in November

S&P Global Eurozone Manufacturing PMI for December: 47.8 vs. 47.1

Joachim Nagel, a member of the European Central Bank’s Governing Council, stated that more measures are required to contain rising price expectations and return inflation to the 2% target.

Eurozone Services Business Activity Index for December was 49.8 vs. 48.5 in November

S&P Global Germany Services PMI rose from 46.1 in November to 49.2 in December

French inflation unexpectedly slows from 7.1% to 6.7% y/y in December

Germany Import Prices for Nov. 2022: -4.5% m/m vs. -1.2% m/m in October

German trade surplus grew from 6.9B EUR to 10.8B EUR in Nov, exports down 0.3% m/m

Germany’s factory orders down by 5.3% m/m in November, the fastest decline since October 2021

Retail trade volume was up by 0.8% m/m in the euro area in November and by 0.9% m/m in the EU

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

Swiss Manufacturing PMI in December: slight move higher to 54.1 from 53.9 in November

Swiss Consumer Price Index fell -0.2% m/m to 104.41 in December (0.0% m/m in November

Swiss Retail trade turnover in November 2022: +1.3% y/y; +1.6% m/m

CAD Pairs

S&P Global Canada Manufacturing PMI fell to 49.2 in December vs. 49.6 in November

Canada trade balance for November: a deficit of C$40M, the first deficit in 11 months; previous month was revised lower to a C$130M surplus

Canada Ivey PMI dropped from 51.4 in November to 33.4 in Decmeber 2022; Prices Index ticked higher to 64.6 vs. 63.5 previous; Employment Index fell to 49.8 vs. 54.3 previous

Canada added 104K jobs in December (vs. 10K forecast) and the unemployment rate fell to 5.0%

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

Global dairy prices fell -2.8% to $3.36

AUD Pairs

Australian commodity prices up 15.6% y/y in Dec vs. previous 19.6% gain

Australia Manufacturing PMI for December: 50.2 vs. 51.3 in November

JPY Pairs

Japanese PM Kishida urges businesses to bump up wages to spur inflation

Japanese consumer confidence index up from 28.6 to 30.3 in Dec vs. 28.2 forecast

Japan’s real wages fall by 3.8% y/y in November, the fastest pace in over 8 years thanks to inflation

au Jibun Bank Japan Services PMI for December: 51.1 vs. 50.3 in November