The British pound took the top spot this week after a round of record setting inflation updates from the U.K.

Inflation, monetary policy and geopolitical developments remained as the main market drivers, in what was a shortened trading week due to the Easter holiday.

Notable News & Economic Updates:

Ukraine-Russia Conflict updates:

- Putin say Ukraine talks ‘at dead end’, vows to pursue ware

- Ukraine claims Russian forces used chemical weapons in Mariupol

- Russia warns of nuclear, hypersonic deployment if Sweden and Finland join NATO

- Russia warns on Friday of “unpredictable consequences” if weapons shipments continue to Ukraine

EIA reports a 9.4M barrel rise in crude oil inventories the week of Apr. 8.

U.S. CPI increased by 1.2% m/m in March; +8.5% y/y

U.K. inflation hits 7.0% in March, the highest rate since 1992

Australian employment change came in below expectations at 17.9K vs. 30.0K forecast

Fed’s Waller sees likelihood of multiple half-point interest rate hikes ahead; Fed’s Bullard says central bank must put brakes on economic activity

China reports its exports rose 15.7% in March over a year earlier, while imports were flat due to virus disruptions

The European Central Bank held off from raising interest rates on Thursday, but hinted we may see hikes as early as Q3 2022

U.S. officials link North Korean hackers to $615M crypto hack of Ronin Network

Central Bank moves this week:

- South Korea central bank unexpectedly raised policy rate 0.25% to 1.50%

- Singapore’s central bank tightened monetary settings and raised 2022 inflation forecast to 4.5% – 5.5% range vs. 2.5%-3.5% range

- Reserve Bank of New Zealand hiked rates more than expected to 1.50%

- Bank of Canada hiked 50 bps to 1.00%

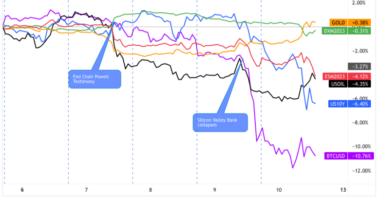

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour

It was a holiday shortened week, but we got to see quite a bit of action before the markets closed early on Friday for Easter. There didn’t seem to be one dominant theme to drive price action, but developments with the war in Ukraine, high inflation, and monetary policy speculation continued to drive price action.

As far as the Ukraine-Russia conflict, it’s arguable that it sparked risk-off vibes as the direction trended more towards escalation rather than de-escalation or a diplomatic end. As we can see from the Notable Headlines above, it looks like talks between the two countries have gone no where. Also, Russia warned of more action if Sweden/Finland join NATO and if the U.S. continued to supply Ukraine with weapons, both raising nuclear war speculation.

We got fresh catalysts on the inflation and monetary policy front with a heavy calendar of not only inflation updates, but central bank action and hawkish rhetoric of more hikes to come. The most notable catalyst of short-term price action was the inflation updates from the U.S. (the highest CPI read since 1981 at 8.5% y/y), which turned out to be a sell on the news event for bond yields as they rallied leading up to the event. There is also some speculation that we may be seeing the top of the inflation rate spectrum.

We also tightening action from the central banks from South Korea, Singapore, New Zealand and Canada, while U.S. Fed rhetoric continued to paint a scenario of multiple 50 bps hikes ahead.

With inflation and geopolitical fears still the main driving themes, it shouldn’t be any surprise to see equities and crypto down once again, as with previous weeks/months for this kind of environment. And on the other side of the spectrum, gold, the U.S. dollar and bond yields saw a bid throughout the week.

Oil took a trip higher this week, arguably on signs of some easing of covid lockdown protocols in China. This possibly overshadowed news that OPEC saw a slowdown of demand in 2022 due to Ukraine war and data showing a rise in crude oil inventories.

In the forex space, the action picked up a bit thanks to central bank rhetoric and action. The Japanese yen was the biggest loser after dovish comments from Bank of Japan Governor Haruhiko, while the British pound took the top spot after traders saw way better-than-expected inflation data from the U.K. on Wednesday.

The biggest surprise from the space, though, was the bigger-than-expected rate hike from the Reserve Bank of New Zealand. They hiked the official cash rate 50 basis points to 1.50%, but with the Kiwi fell throughout the session after the announcement. Arguably, this bigger-than-expected rate hike may be front loading the tightening and that the RBNZ may not move further than a 2.00% OCR target.

USD Pairs

Fed’s Evans: half-point hikes likely, shouldn’t go too far

Consumer fears over inflation hit a record high in March, New York Fed survey shows

Consumer prices rose 8.5% in March, slightly hotter than expected and the highest since 1981

Fed’s Barkin says interest rates should be moved rapidly to neutral

U.S. Producer Prices was up +1.4% m/m in March; +11.2% y/y

The University of Michigan’s consumer sentiment index: 65.7 in April vs. 59.4 in March

U.S. business inventories rose 1.5% in February vs. 1.3% in January; +12.4% y/y

Fed’s Mester says it’s ‘imperative’ to get inflation down

U.S. Weekly jobless claims: 185K vs. 167K previous week

U.S. retail sales rise 0.5% in March vs. 0.6% forecast & 0.8% previous

NY manufacturing rebounds from -11.8 to 24.6 in April

GBP Pairs

U.K. GDP rose +0.1% m/m in February vs. +0.8% in Jan.

U.K. CPI rose by 7.0% y/y in March, the highest rate in 30 years; Core CPI rose 5.7% y/y, both above expectations

U.K. Services output rose by 2.1%; construction output up 1.1% in February

U.K. Manufacturing production in Feb. was down -0.4%; industrial production -0.6%

U.K. claimant count down 46.9K vs. projected 41.1K decline; U.K. jobless rate improved from 3.9% to 3.8% as expected; U.K. average earnings index climbed from 4.8% to 5.4% as expected

EUR Pairs

German final CPI unchanged at 2.5% as expected

German ZEW economic confidence weakened to -41.0 in April from -39.3 in March

Euro Zone ZEW Economic Sentiment fell to -43 vs. -38.7

Germany wholesale price index: +6.9% in March vs. +1.7% in February

Spain March final CPI rises 9.8% y/y, fastest pace since May 1985

European Central Bank renewed pledge to end bond-buying in Q3; See inflation remaining high due to energy costs

Lagarde pinpoints June as moment for clarity on ECB pullback

CHF Pairs

Swiss PPI posted 0.8% uptick vs. projected 1.1% gain, 0.4% previous

CAD Pairs

Bank of Canada hikes key interest rate by 50 basis points to 1.00%; will end QT beginning April 25.

Canadian manufacturing sales rose 4.2% to $67.7B

NZD Pairs

New Zealand business confidence: -40 in Q1 vs. -28 previous

NZD firms as RBNZ raises rates by 0.50% to 1.5%, the biggest rate hike in 22 years

New Zealand BusinessNZ manufacturing index up from 53.6 to 53.8

AUD Pairs

Australian NAB business confidence index climbed from 13 to 16 in March

AU MI consumer sentiment index dipped by -0.9% m/m in April vs. -4.2% m/m in March

Australian economy added 17.9K jobs vs. 30K expected in March; unemployment rate steady at 4

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Bank of Japan cuts view on most Japan regions, warns on Ukraine impact

Japanese bank lending up by 0.5% as expected

Japanese producer prices rose 9.5% vs. 9.2% forecast, 9.7% previous

Japanese finance minister Suzuki jawbones excess FX volatility

Japan’s wholesale prices surge 7.3% in FY 2021, fastest pace on record

Japan’s machinery orders fell by 9.8% in February, the biggest decline since April 2020

Japan’s Tankan sentiment index for manufacturers improves from 8 to 11 in April