On Friday, it’ll be the Bank of Japan’s turn to announce their monetary policy decision.

Will they shift their tone this time? And if so, how can this affect JPY pairs?

Here are the important points you need to know if you’re planning on trading the news:

Event in Focus:

Bank of Japan (BOJ) Monetary Policy Statement

When Will it Be Released:

June 16, Friday: tentatively 3:00 am GMT

BOJ Governor Kazuo Ueda will hold a press conference after the announcement.

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- BOJ to keep policy rate on hold at -0.10%

- No changes to yield curve control policy expected

Relevant Eurozone Data Since Last BOJ Statement:

? Arguments for Hawkish Monetary Policy / Bullish JPY

April consumer confidence index climbed from 33.9 to 35.4 vs. estimated 34.7 figure, May reading improved further to 36.0

April Economy Watchers Sentiment index rose from 53.3 to 54.6 to reflect stronger optimism vs. estimated 54.1 reading, May reading improved further to 55.0

Preliminary Q1 GDP showed stronger 0.4% quarterly expansion vs. projected 0.2% growth figure and earlier flat reading, later on upgraded to 0.7% growth

Preliminary GDP price index for Q1 accelerated from 1.2% year-over-year to 2.0% as expected

April national core CPI rose from 3.1% year-over-year to 3.4% as expected, marking back-to-back monthly gains

May flash manufacturing PMI rose from 49.5 to 50.8 to signal shift from contraction to expansion for the first time in seven months

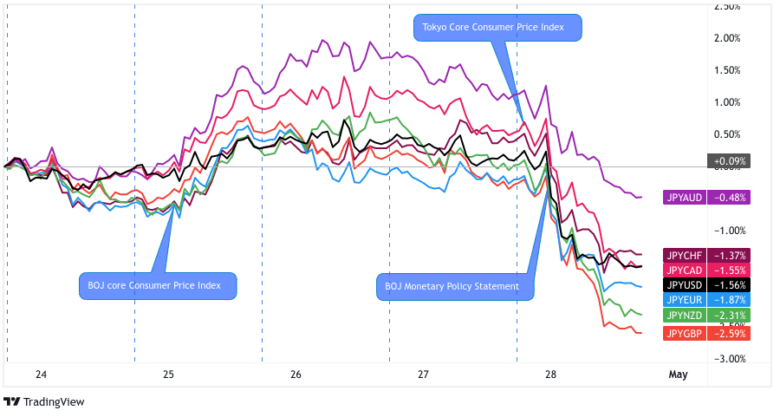

BOJ core CPI for April rose from 2.9% to 3.0% year-over-year instead of dipping to consensus at 2.8%

? Arguments for Dovish Monetary Policy / Bearish JPY

March average cash earnings unchanged at 0.8% year-over-year gain vs. estimated 1.0% increase, later on upgraded to 1.3% rise. April reading fell short at 1.0% y/y increase vs. 1.7% consensus

March household spending slumped 1.9% year-over-year vs. projected 0.9% gain, erasing part of earlier 1.6% rise, May figure fell further to show 4.4% y/y decline

April producer price index reflected 5.8% year-over-year gain vs. estimated 5.6% increase, but the pace slowed down for the fourth consecutive month. May PPI slipped to 5.1% y/y

March tertiary industry activity slowed 1.7% month-over-month vs. estimated 0.3% uptick, erasing earlier 1.7% gain

April Tokyo core CPI fell from 3.5% year-over-year to 3.2% vs. projected dip to 3.4%

April industrial production fell 0.4% month-over-month vs. estimated 1.4% gain, marking first fall in three months

April retail sales slowed from downgraded 6.9% year-over-year gain to just 5.0% vs. estimated 7.1% increase

Previous Releases and Risk Environment Influence on JPY

Apr. 28, 2023

Action/Results: The BOJ kept monetary policy unchanged during their April decision, holding rates at -0.10% and maintaining YCC, as expected.

Prior to the announcement, head honcho Ueda already mentioned in a speech that “it’s appropriate to maintain monetary easing” for now but also said that BOJ stands ready to raise interest rates “if wage growth and inflation accelerates faster than expected.”

Yen selling carried on until the end of the week since the central bank removed any forward guidance and hinted that it could take over a year before their policy review is completed.

Risk environment and Intermarket behaviors: The safe-haven yen was already enjoying some support from risk-off flows early in the week, as recession fears and debt ceiling issues were in play.

Later on, the Japanese currency got an extra boost from stronger than expected BOJ core CPI.

Risk-taking took over around the middle of the week when U.S. earnings figures started comin’ in hot and Congress passed legislation that could raise the debt ceiling. This forced the yen to return some of its earlier gains, before accelerating its slide during the BOJ announcement.

Mar. 10, 2023

Action/Results: This was former BOJ Governor Kuroda’s last stint as head honcho, so policymakers refrained from making any major changes as they transitioned to incoming Chairperson Ueda’s leadership.

Policymakers voted unanimously to keep rates on hold at -0.10% and to maintain the yield curve control in place.

Although the yen took a sharp tumble during the announcement, the lower-yielding currency managed to pull up before the week came to a close, as risk aversion stayed the dominant market theme.

Risk environment and Intermarket behaviors: U.S. banking sector woes stemming from the SVB bank run were the main theme for this trading week, spurring risk-off flows and the lower-yielding yen supported.

Apart from that, hawkish expectations from the likes of the Fed also had traders flocking to the dollar and boosting U.S. bond yields while also staying wary of recession risks.

Price action probabilities

Risk sentiment probabilities: Most major currencies appear to be trading cautiously in ranges so far, as market players are likely holding out for the week’s top-tier catalysts.

The biggest event of the week, FOMC monetary policy statement, just came and went and despite the Fed holding off on hiking once again, we’re seeing a slight pro-dollar reaction at the moment, likely on rhetoric that more rate hikes are likely to come and that no Fed member sees a rate cut in 2023.

This may tip risk sentiment towards risk-off by the time we get to the BOJ statement, with rising probability of risk-off vibes if we get a hawkish tone to accompany a rate hike from the ECB monetary policy decision on Thursday.

JPY scenarios

Base case: As many are expecting, the BOJ is likely to keep interest rates and overall monetary policy unchanged for the time being.

Keep in mind that policymakers had been counting on the wage hike talks to translate to a much stronger pickup in salaries and inflationary pressures in the past month. However, actual cash earnings figures turned out weaker than expected, keeping a lid on household spending as well.

With that, BOJ officials would likely acknowledge green shoots in the economy but also reiterate their plans to stay easy on policy until they achieve target inflation in a “stable and sustainable” manner.

Confirmation that the BOJ plans on keeping policy unchanged for over a year or until they complete their policy review might mean more downside for JPY against currencies with more hawkish policies like EUR, AUD, or CAD, especially if broad risk sentiment leans positive heading into the weekend.

Alternative Scenario: In some of Governor Ueda’s speeches, he mentioned that they are starting to see noteworthy economic improvements.

He even suggested that changing the bank’s policy target from the current 10-year yield to a five-year one might be an option if they were to modify the YCC in the future. After all, he also noted that they’re open to tweaking the YCC “if the balance between the benefit and cost of the policy shifts.”

Although Ueda said that the BOJ must refrain from tightening prematurely, policymakers might have differing opinions and express not-so-dovish biases in this week’s announcement.

In that low probability scenario, look for short-term opportunities to buy JPY against forex rivals whose central banks are shifting to a less hawkish stance, such as NZD or possibly USD, with more conviction if broad risk sentiment is leaning negative heading into the weekend.