U.S. debt-limit drama was the big sentiment driver this week, but we also saw fresh central bank comments and top tier economic updates that actually shook up interest rate outlooks and the usual intermarket price action tendencies.

Ready to hear what happened this week? Better check the market-moving headlines first!

Notable News & Economic Updates:

? Broad Market Risk-on Arguments

Australia’s monthly CPI accelerated from 6.3% y/y in March to 6.8% y/y in April (vs. 6.4% expected)

JOLTS U.S. Job Openings in April: 10.1M vs. 9.75M in March; “the number and rate of layoffs and discharges decreased to 1.6M”

ADP National Employment Report for May: +278K (+200K forecast) vs.291K previous

The debt-limit legislation brokered by President Joe Biden and Speaker Kevin McCarthy last weekend was passed by the House Wednesday evening with a 314-117 vote

American Petroleum Institute (API) data showed that crude oil inventories rose by 5.202M barrels last week vs. an expected dip of 1.22M barrels; EIA crude oil inventories post surprise 4.5 million barrel build instead of the estimated 1.2 million barrel draw, suggesting slower demand

Fed official Harker pointed out that consumers aren’t spending as much as they used to, so it might be time to pause in June

France’s inflation unexpectedly lower at -0.1% m/m in May vs. 0.3% expected, 0.6% uptick in April

The U.S. Senate passed the debt ceiling and budget cuts package late Thursday evening, bringing the U.S. one step closer to avoiding a debt default scenario

Caixin China General Manufacturing PMI for May: 50.9 vs. 49.5 previous; the first expansionary read in three months

U.S. Non-Farm paryolls for May: +339K (+180K forecast) vs. upwardly revised 294K in April; Unemployment Rate rose to 3.7% (3.5% forecast, 3.4% previous); Average hourly earnings: +0.3% (+0.4% forecast/previous)

? Broad Market Risk-off Arguments

China’s manufacturing PMI unexpectedly fell down from 49.2 to 48.8 vs. 49.5 expected in May on weakening demand

China’s services PMI eased from 56.4 to 54.5 in May, marking the slowest expansion in four months

RBA Gov. Lowe: “We really want people to understand that we’re serious about this, that we will do what is necessary, and not to question our commitment to get inflation down. As painful as it is, we’ve got work to do there.”

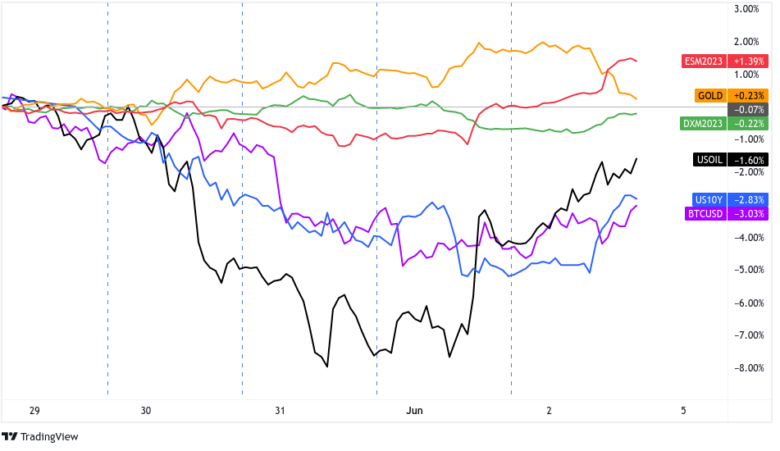

Global Market Weekly Recap

Dollar, Gold, S&P 500, Bitcoin, Oil, U.S. 10-yr Yield Overlay Chart by TV

Over the weekend, U.S. lawmakers reached a tentative agreement that would suspend the $31.4 trillion debt ceiling until Jan. 1, 2025. The deal was still up for Congress vote, but lawmakers seemed optimistic the deal would pass, and the markets cheered the development.

The optimism was particularly felt during the Monday Asian session as most European and U.S. markets were closed on holiday. Commodity-related currencies rose while Nikkei jumped to its highest levels since 1990. That’s about the time The Simpsons was just getting traction after its December 1989 release!

Traders went “hmmmm…” on Tuesday as some doubted the debt deal would pass. It also didn’t help risk-takers that China released data during the weekend showing weak industrial profits (-18.2% y/y drop), casting doubts on global economic recovery post-pandemic.

Gold traded higher and crude oil plummeted by more than 4% on uncertainties over China’s growth, the passing of the debt ceiling deal, and the upcoming OPEC meeting.

Volatility got crazier on Wednesday thanks to a couple of market-moving catalysts. Australia got the party started with a higher-than-expected monthly CPI that supported another Reserve Bank of Australia (RBA) rate hike. Then China took the baton just a couple of hours later with not one but TWO disappointing official PMI reports that brought back fears of low growth ahead amidst expectations of a high inflation, high-interest rate environment.

Then, a slower-than-expected inflation read from France eased European Central Bank (ECB) rate hike expectations and lowkey weighed on the euro. The party peaked during the U.S. session when JOLTS job openings showed an unexpected rise in job openings which raised Fed rate hike expectations.

But that was before Fed members Philip Jefferson and Patrick Harker started talking about a “June skip.” In separate speeches during the Wednesday U.S. trading session, the FOMC voting members implied that the Fed would need more time to assess the lagging impact of their previous rate hikes.

This likely fueled some to price in lower odds of a rate hike in June (i.e., typically leading to some risk-on moves), but it only seemed to be enough to stabilize broad risk sentiment as there was likely plenty of traders still worried about the passing of the U.S. debt ceiling bill and lower growth indicators from China.

Thursday brought a glimmer of hope as China’s Caixin manufacturing PMI exceeded expectations, correlating with a bounce in oil and bond yields, as well as further stabilization behavior in equities.

European equities also joined the party during the Thursday London session as easing inflation updates encouraged discussions on whether the ECB will still need a rate hike beyond this month. This is despite ECB President Lagarde literally saying that they “still have ground to cover” to bring rates to “sufficiently restrictive levels” but that’s neither here nor there. I guess.

Of course, it also helped risk-takers that the U.S. House of Representatives approved a bipartisan bill to suspend the government’s $31.5 trillion debt ceiling, reducing Uncle Sam’s risks of default. The U.S. Treasury yields and the dollar extended their losses while equities, crude oil, GBP, AUD, and NZD traded higher. Gold even gained ground on the back of USD weakness!

Friday’s calendar was extremely light, but it’s no question that what we got was a market mover. During the U.S. trading session, we got the highly anticipated monthly U.S. government update on employment conditions, including the Non-Farm Payrolls change, unemployment rate, and average earnings change for the month of May. The numbers showed resilience once again with the NFP number coming in way above the +180K expectations at 339K jobs added and the April number being revised up to 294K.

These numbers arguably support the idea that the risk of crashing the economy with more Fed rate hikes has lowered, and when coupled with news of the U.S. Senate passing the debt-limit deal, it’s no surprise why traders were in risk-on mode, as well as dumping gold and buying some Greenbacks into the weekend.