The spotlight turned to China and the U.S. for the most part of the week, as updated Chinese GDP forecasts and net better-than-expected U.S. economic updates stole the show.

Hawkish central bank rhetoric during the ECB Forum on Central Banking also affected overall market sentiment, especially since the arguably upbeat outlook was underscored by mostly strong data.

Missed all the market movers this week? Lemme show you the biggest headlines first:

Notable News & Economic Updates:

? Broad Market Risk-on Arguments

Crude oil opened slightly higher after a failed coup attempt in Moscow, as Wagner mutiny convoys returned to bases and charges against Prigozhin dropped

PBOC set USD/CNY reference rate lower than expected during their announcements on Tuesday and Thursday to slow down the pace of the yuan’s declines

Chinese Premier Li Qiang said that growth has picked up this quarter and more stimulus was in store

U.S. EIA crude oil inventories showed a draw of 9.6 million barrels vs. the estimated reduction of 1.4 million barrels and earlier draw of 3.8 million barrels

Mostly upbeat U.S. economic data:

- May core durable goods orders rebounded 0.6% month-over-month after an earlier 0.3% decline, with headline reading up 1.7% vs. estimated 0.8% drop

- New home sales jumped from 680K to 763K, beating the consensus at 677K

- Richmond manufacturing index improved from -15 to -7 in June vs. the estimated -12 figure

- U.S. CB consumer confidence index jumped from 102.5 to 109.7 in June vs. the projected 103.9 reading, the highest level since early 2022

- Initial jobless claims came in at 239K vs. 264K forecast and 265K previous, easing fears of a U.S. labor market slowdown

- U.S. final Q1 GDP revised higher to 2% year-over-year growth from 1.2% previously reported

- U.S. Core PCE Index for May: 3.8% y/y (3.9% y/y forecast; 4.3% y/y previous); personal income grew by +0.4% m/m (+0.3% m/m forecast/previous)

? Broad Market Risk-off Arguments

S&P cut the Chinese GDP forecast from 5.5% to 5.2% for the year, citing that an uneven pace of growth can be expected

Australian May CPI slumped from 6.8% to 5.6% year-over-year vs. an estimated dip to 6.1%

Japanese Ministry of Finance’s vice minister Kanda says they are closely monitoring FX moves with a high sense of urgency

Canadian headline May CPI came in line with consensus at 3.4% year-over-year from the previous 4.4% reading, the lowest since June 2021

ECB Forum on Central Banking remarks:

- Fed Chair Powell said that “although policy is restrictive, it many not be restrictive enough and it has not been restrictive for long enough” upping the odds of two more rate hikes this year

- ECB Chairperson Lagarde noted the impact of tight labor markets on wage increases, which are further stoking inflationary pressures

- BOE head Bailey pointed to noticeable signs of sustained inflation in the U.K. economy and that they would take all steps necessary to bring it back to target

- BOJ Governor Ueda reiterated their plans to keep monetary policy unchanged while policymakers monitor the impact of higher rates on economic activity

Global Market Weekly Recap

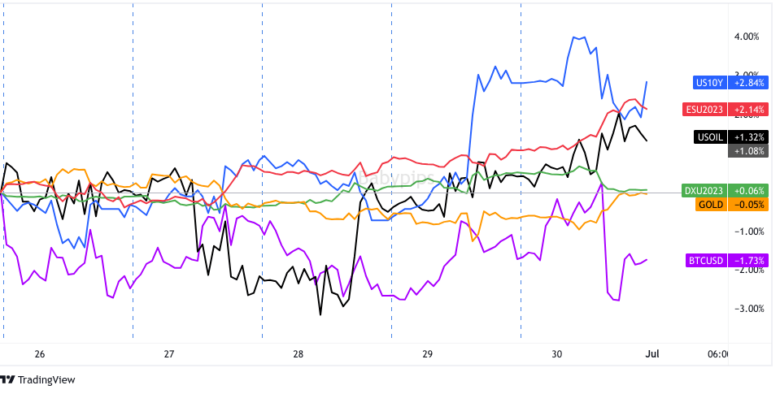

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TV

Market players woke up on the wrong side of the bed this week, as risk-off flows from last Friday and the S&P downgrade on Chinese growth forecasts over the weekend soured the mood.

Not even crude oil, which enjoyed a bit of a rally on news of a military coup in Russia, was able to hold on to its gains early on.

However, the tide turned on Tuesday when the People’s Bank of China took the markets by surprise when they set the yuan reference rate stronger than expected, sending the message that the central bank is keen on slowing the currency’s decline.

Riskier assets like U.S. equities and commodity currencies staged sharp rallies, although rumors that the U.S. government is considering fresh restrictions on AI-related exports to China led to losses for Nvidia and AMD.

Comdolls soon coughed up their winnings when downbeat Australian and Canadian CPI figures dampened hopes for another round of rate hikes from the RBA and BOC.

Safe-havens like the dollar and gold continued to gain ground when the ECB forum highlighted hawkish rhetoric among the likes of Fed head Powell, ECB Chairperson Lagarde, and BOE Governor Bailey.

Crude oil put up a pretty decent fight thanks to improving demand conditions as reflected in surprise inventory reductions from the API and EIA, but the commodity soon caved to expectations of higher global interest rates.

Later in the week, Treasury yields and the dollar got another boost from upbeat U.S. initial jobless claims data, soothing fears that the labor market could soon see a slowdown. Upgraded final GDP figures for Q1 also contributed to dollar gains.

With that, markets priced in stronger odds of at least two more Fed rate hikes before the year comes to a close while traders looked ahead to Friday’s U.S. core PCE price index report.

As expected, the Fed’s preferred inflation gauge didn’t disappoint. While the core reads weren’t too far off from expectations, the headline read’s (including the volatile food and energy components) decline was very notable at 3.8% y/y vs. 4.3% y/y in April. Personal income surprised with a 0.4% m/m read, while personal spending was significantly below April’s 0.6% read at 0.1%.

On net, this likely lowered the case for the Fed to be less hawkish going forward, characterized by a swift move lower in the U.S. dollar and bond yields after the event. Of course, signs that the Fed may take their foot off the gas was net positive for risk sentiment, along with supporting the idea that expectations of an improving interest rate environment will likely help the U.S. to potentially avoid recession.