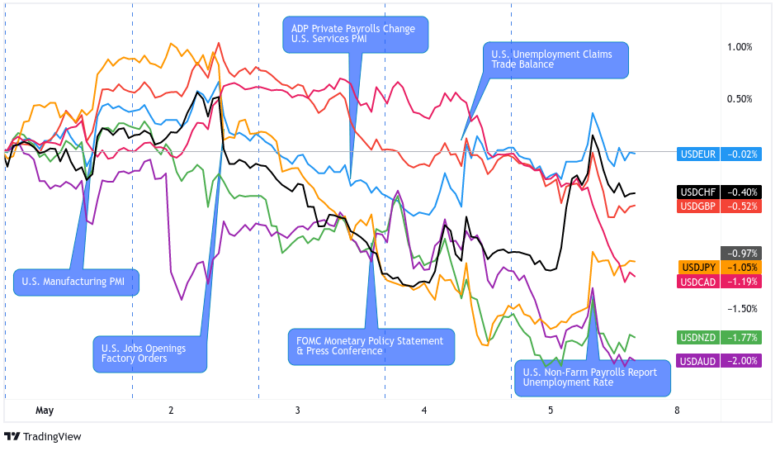

It was a crazy busy week for forex traders as they had to balance a cornacopia of top tier catalysts, including the latest U.S. employment update and THREE major central bank policy statements.

AUD and NZD took the top spot as risk sentiment shifted mid-week, while “dovish hikes” from the Fed and ECB weighed on the Greenback and the Euro into a battle for worst performer of the week.

USD Pairs

A combination of mixed labor market numbers, regional bank contagion fears, and recession concerns dragged the dollar into a downtrend for most of the week.

It wasn’t until Uncle Sam printed stronger-than-expected U.S. NFP reports that the dollar found enough demand to recoup some of its intraweek losses.

? Bullish Headline Arguments

S&P Global US Manufacturing PMI for April: 50.2 vs. 49.2 in March; ” input costs and output charges increased at steeper rates during April.”

ISM Manufacturing PMI for April: 47.1 vs. 46.3 in March: Prices Index for by 4.0 to 53.2; Employment Index was up 3.3 to 50.2

U.S. Private sector payrolls for April: +296K (+140K forecast) vs. 142K in March

ISM Services PMI for April: 51.9 vs. 51.2 in March; Prices Index ticked up 0.1 to 59.6; Employment Index dipped to 50.8 vs. 51.3 previous

U.S. Factory Orders for March: +0.9% m/m (+1.2% m/m forecast) vs. -1.1% m/m previous

FOMC hiked interest rates by 0.25% as expected from 5.00% to 5.25%, as policymakers noted that inflation remains above goal

Fed head Powell noted that there was strong support for interest rate hikes and that a pause was not yet discussed during their meeting

U.S. continuing jobless claims fell by 38K to 1.805M

U.S. Non-Farm Payrolls for April: 253K (190K forecast) vs. 165K in March; unemployment rate fell to 3.4%; Average hourly earnings came in above 0.3% forecast at 0.5%

? Bearish Headline Arguments

Yellen Says U.S. Risks Default as Soon as June 1 Without Debt Ceiling Increase

POTUS Biden invited top congressional leaders for a May 9 meeting on the debt limit

U.S. layoffs grew to the highest levels since 2000; the quits rate fell to 2.5% (lowest in 2 years); job openings fell to 9.59M from 10M

Shares of major U.S. regional banks fell as FRC failure shakes faith in banking sector recovery

U.S. weekly MBA Mortgage Applications: -1.2% w/w vs. 3.7% w/w

Powell mentioned that policymakers believe they are approaching the end of their tightening cycle but that cutting would not be appropriate given inflation trends

U.S. weekly jobless claims for the week ending April 28: 242K vs. 229K the previous week

U.S. job cuts in April 2023: 66.99K cuts vs. 24.28K in April of 2022 – Challenger, Gray & Christmas, Inc.; this is the fourth month in a row where the number of cuts were higher than the same month in the year previous

EUR Pairs

Euro price action was mixed but with a risk-off lean despite expectations of a rate hike from the European Central Bank this week. The Euro area calendar was arguably net negative for the euro leading up to the ECB event, but the bearish lean may have also been some profit taking on the recent rally in the euro ahead of the major risk event.

On Thursday, we finally got the highly anticipated 25 bps rate hike, and ECB President Lagarde made it clear that they’re not yet done tightening. But traders priced in future easing as the ECB hinted at potentially slowing their pace of hikes going forward.

? Bullish Headline Arguments

Euro area unemployment rate for March: 6.5% vs. 6.6% in February

European Central Bank hiked the deposit rate from 3.00% to 3.25% on Thursday as expected; APP bond reinvestments will end in July; tightening will continue but at a slower pace

HCOB Eurozone Services PMI in April: 56.2 vs. 55.0 in March

HCOB Germany Services PMI for April: 56.0 vs. 53.7 in March; businesses are seeing increased interest from clients

Euro Area PPI for March: 5.9% y/y (6.9% y/y forecast) v.s 13.9% y/y previous; on a monthly basis, the slowdown accelerated at -1.6% m/m vs. -0.4% m/m previous

Lagarde: Central bank is not pausing from tightening, as governors are all determined to fight inflation

? Bearish Headline Arguments

Germany’s retail sales were down by another -2.4% m/m in March vs. downwardly revised -0.3% in February, 0.4% expected

HCOB Eurozone Manufacturing PMI for April: 45.8 vs. 47.3 in March

HCOB Germany Manufacturing PMI for April: 44.5 vs. 44.7 previous; “Average purchase prices fell for the third month running and at the quickest rate since December 2019”

Euro Area Monetary Developments for March: “Annual growth rate of adjusted loans to households decreased to 2.9% in March from 3.2% in February”; “Annual growth rate of broad monetary aggregate M3 decreased to 2.5% in March 2023 from 2.9% in February”

Germany Factory Orders for March: -10.7% m/m (-2.3% m/m forecast) vs. 4.5% m/m

Euro Area retail trade for March 2023: -1.2% m/m (-0.1% m/m forecast) vs. -0.2% m/m previous

GBP Pairs

This week’s U.K. sorely lacked top-tier economic reports, and what we did get wasn’t enough to maintain Sterling’s recent net bullish vibes over the past month.

The currency also fell victim to risk aversion in the first half of the week but also recovered some of its losses, especially against the euro and the Swiss franc.

? Bullish Headline Arguments

British Retail Consortium: U.K. shop price inflation cooled from a record high of 8.9% to 8.8% in April as heavy discounting on clothing and furniture pulled the index lower.

Nationwide: U.K.’s house prices rose by 0.5% m/m in April, the first increase in eight months. Annual growth improved from -3.1% to -2.7%.

? Bearish Headline Arguments

S&P Global / CIPS UK Manufacturing PMI for April: 47.8 vs. 47.9 in March; “Rates of increase in average input costs and output charges both eased in April, falling to 35- and 28-month lows respectively”

S&P Global / CIPS UK Services PMI for April: 55.9 vs. 52.9; “a combination of stronger demand and rapidly rising business expenses led to a faster rate of prices charged inflation”

U.K. mortgage approvals for March were inline with February at £700M but far below £1.6B forecast; net lending to individuals slowed considerably to £1.6B (£2.7B forecast) vs. £2.2B previous

CHF Pairs

Overlay of CHF vs. Major Currencies Chart by TV

Switzerland’s calendar was mostly quiet this week, which meant that CHF mainly took its cues from risk sentiment and counter currency flows.

With the broad markets mostly in risk-off mode, “Safe haven” demand helped pushed CHF 1% to 1.50% higher across the board until risk-taking behavior recovered and dragged it below its weekly open prices against most of the majors.

? Bullish Headline Arguments

On Friday, Swiss National Bank Chairman Thomas Jordan said they may have to tighten interest rates further

Swiss Unemployment in April: 90.5K unemployed vs. 92.7K in March; the unemployment rate held steady at 2.0%

Swiss Consumer Price Index for April: +2.6% y/y but +0.0% m/m; Core inflation rose +0.2% m/m

? Bearish Headline Arguments

SECO Swiss Consumer Sentiment Index: -29.7 (-24.4 forecast) vs. -30.1 previous

Swiss Purchasing Managers Index (PMI) for April: 45.3 vs. 47.0 in March

AUD Pairs

Overlay of AUD vs. Major Currencies Chart by TV

A surprise RBA rate hike pushed AUD sharply higher to its intraweek peak on Tuesday.

Risk aversion nearly dragged it back to its weekly open prices, but a recovery in market sentiment on Thursday and Friday eventually pushed it back in the green against its major counterparts.

? Bullish Headline Arguments

RBA surprised market playas with a 25bps rate hike to 3.85%, citing “too high” inflation that will take “a couple of years” before returning to the target range. RBA noted that some further tightening “may be required” to return inflation to its target “in a reasonable timeframe” -11th increase in a year, the highest rate since April 2012

Australia’s retail sales rose 0.4% m/m in March, the third consecutive month of growth, driven by rising food prices.

Judo Bank Australia Services PMI Business Activity Index shot up from 48.6 to 53.7 – its fastest pace in a year – in April, supporting RBA’s rate hike

Australia’s trade surplus widened from 14.1 billion AUD to 15.27 billion AUD in March vs. estimated 13 billion AUD figure, thanks to 4% increase in exports

RBA statement on monetary policy: More rate hikes may be required in order for inflation to reach the target within a reasonable timeframe, reducing the risk of a wage spiral

RBA lowered its end-of-year 2023 forecasts for inflation (4.25% to 4.0%) and broader GDP growth (from 1.5% to 1.25%) and upgraded its unemployment estimates (from 3.75% to 4.0%) compared to its March projections

? Bearish Headline Arguments

Australia’s MI inflation gauge slowed from 0.3% month-over-month to 0.2% in April to reflect weaker price pressures

Australia’s ANZ job advertisements tumbled 0.3% month-over-month in April, following earlier 2.4% slump

Australian commodity prices slipped 19.2% year-over-year in April vs. an earlier 6.9% drop due to lower coal, iron ore and LNG prices

Judo Bank Australia Manufacturing PMI for April: 48.0 vs. 49.1 in March

CAD Pairs

Risk aversion and lower oil prices dragged CAD across the board all week.

On Thursday, a combination of improving broad risk sentiment and comments from BOC Governor Macklem opening up the possibility of rate hikes again had the comdoll reversing a majority its losses into the weekend. It even managed to cap the week higher against the European currencies (EUR, GBP, CHF) and the dollar!

? Bullish Headline Arguments

S&P Global Canada Manufacturing PMI for April: 50.2 vs. 48.6 previous; “Prices paid for inputs rose sharply in April, with the rate of inflation accelerating to its highest level of the year so far”

Canada Trade Balance for March: C$972M vs. -C$487M in February; Exports in March fell by -0.7% m/m while imports fell by -2.9% m/m

BOC Governor Macklem says they are not done hiking interest rates, especially if inflation climbs back above 2%

Canada labour Force Survey for April: +41K (+25K forecast) vs. +34K previous; Unemployment Rate came in below the 5.2% forecast at 5.0%; Average hourly wages was below 5.4% y/y forecast at 5.2% y/y (inline with previous read)

? Bearish Headline Arguments

Canadian Ivey PMI down from 58.2 to 56.8 vs. estimated 59.0 figure, reflecting slower expansion instead of the expected faster growth pace

NZD Pairs

Overlay of NZD vs. Major Currencies Chart by TV

The Reserve Bank of Australia unexpectedly raising its interest rates got traders speculating on an RBNZ rate hike, supported later by a better than expected unemployment update from New Zealand.

And with broad risk sentiment improving on Thursday, NZD rode the hawkish expectations high to the top of the forex heap this week.

? Bullish Headline Arguments

Global Dairy Prices rose by +2.5% to $3.506 in Tuesday’s auction (below the +3.2% rise in the Apr. 18 auction)

RBNZ’s Financial Stability Report: “New Zealand’s financial system is well placed to handle the increasing interest rate environment and international financial market disruptions”

New Zealand’s quarterly employment change up by 0.8% in Q1 vs. 0.5% expected and previous, unemployment rate steady at 3.4% vs. 3.5% expected

? Bearish Headline Arguments

New Zealand ANZ commodity prices slipped 1.7% month-over-month in April vs. previous 1.3% gain, as exporter freight prices continue to soften

JPY Pairs

Overlay of JPY vs. Major Currencies Chart by TV

A not-so-hawkish BOJ event last week weighed on the yen on Monday and early Tuesday, but the vibe shifted quickly as recession worries grew, drawing in JPY buyers in the process.

That seems to have been enough to keep the Japanese yen a net winner at the week’s end with exceptions its behavior against the AUD and NZD.

? Bullish Headline Arguments

Japanese consumer confidence index improved from 33.9 to 35.4 in April vs. estimated 34.7 figure, as overall livelihood, income growth, and employment ticked higher

AU Jibun Bank Japan Manufacturing PMI for April: 49.5 vs. 49.2 in March; “Average cost burdens faced by manufacturing firms increased amid ongoing reports of input shortages and exchange rate weakness”

? Bearish Headline Arguments

Japan monetary base sinks further, down 1.7% y/y vs. -1.3% expected in April

This post first appeared on babypips.com