Canada’s upcoming jobs release might determine whether or not the BOC can keep hiking.

So what are market watchers expecting for this top-tier report?

Here’s what you need to know.

Event in Focus:

Canada’s June Employment Data: Employment Change, Unemployment Rate

When Will it Be Released:

July 7, 2023 (Friday) 12:30 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- Net of -10,000 jobs lost in June, following earlier 17.3K reduction in May

- Unemployment rate to tick higher from 5.2% to 5.4%

- Average hourly wages rate to slow to 4.3% vs. 5.1% year-over-year rate in May

Relevant Data Since Last Event/Data Release:

- S&P Global Canada Manufacturing PMI for June: 48.8 vs. 49.0 in May; market demand subdued due to clients postponing spending decisions (likely due to high interest rates and macroeconomic uncertainty); “firms on average chose to cut their employment levels”

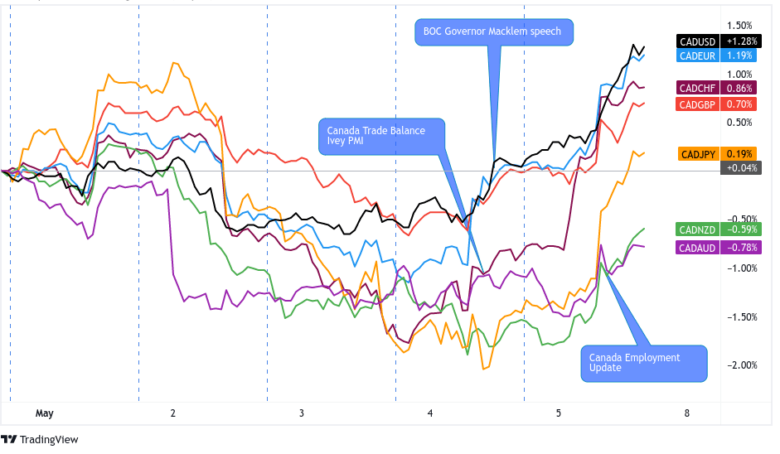

Previous Releases and Risk Environment Influence on the Canadian Dollar

June 9, 2023

Event Results / Price Action:

The Canadian economy lost 17.3K jobs in May versus expectations of a 21.2K increase in hiring. This brought the jobless rate up from 5.0% to 5.2%, higher than the 5.1% consensus.

This downbeat report forced the Loonie to return some of its gains from earlier in the week, but the initial bearish reaction was short-lived.

Risk Environment and Intermarket Behaviors:

The oil-related currency was actually off to a positive start on Monday after the OPEC+ announced voluntary output cuts over the weekend.

The Loonie even extended its gains when the BOC surprised with a 0.25% interest rate hike and signaled willingness to keep hiking until inflation returns to target.

Renewed recession fears weighed on oil prices and the correlated CAD ahead of the jobs release, but the higher-yielding comdoll managed to pull higher late Friday when risk sentiment improved on positive Chinese banking rate news.

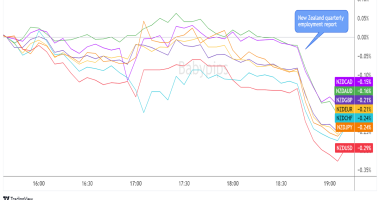

May 5, 2023

Overlay of CAD vs. Major FX: 1-Hour Forex Chart by TV

Event Results / Price Action:

Canada saw an additional 41.4K jobs in April, nearly twice as much as the estimated 21.6K increase. This was also notably higher compared to the previous month’s 34.7K gain in hiring.

With that, the jobless rate held steady at 5.0% for the fifth consecutive month instead of rising to the estimated 5.1% figure.

Not surprisingly, the Loonie rallied across the board when traders got wind of stronger than expected jobs data, as this underscored hawkish remarks made by BOC head Macklem the day before.

Risk Environment and Intermarket Behaviors:

It wasn’t exactly the best of weeks for Loonie bulls, as risk-off flows were strongly in play early on due to concerns about the U.S. banking sector and a potential government default.

However, the tide turned when risk appetite improved midweek on debt ceiling developments and Governor Macklem hinted that the BOC is not done hiking interest rates just yet.

These allowed the Loonie to pull higher ahead of Friday’s jobs release and likely helped the Canadian currency sustain its rally until the end of the week.

Price action probabilities:

Risk sentiment probabilities:

This trading week comes with a handful of top-tier catalysts, including the RBA decision, FOMC minutes, and NFP release. OPEC meetings are also scheduled to take place around the middle of the week, so any major announcements could also impact Loonie price action ahead of Friday’s employment report.

It’s likely the FOMC meeting minutes will have the most potential impact on risk sentiment heading into the Friday print, and unless we see major difference in rhetoric from what we’ve been given recently (i.e., central banks staying hawkish on fighting inflation & likely two more rate hikes ahead in 2023 from the Fed), it may not influence risk sentiment all that much.

At the moment, we’re seeing a broad risk-on lean with some anti-Dollar vibes, so we may see that heading into the Friday data, barring any major surprises between now and then.

One last note on the risk environment: Uncle Sam will be printing the NFP at exactly the same time as Canada’s jobs release, so CAD pairs might also be extra sensitive to overall market sentiment and USD direction then.

Canadian Dollar scenarios:

Potential Base Scenario:

With expectations of the Canadian employment situation expected to slow in June, we think that if that plays out, we could see selling pressure on the Loonie this week. A slower jobs environment supports the idea the BOC has the potential to pause at their next meeting.

The Canadian central bank already surprised the markets with a 0.25% interest rate hike in their June decision, so the prospect of returning to “pause mode” might be enough to encourage Loonie bulls to pull some longs/take profits and tactical bears to take on fresh shorts against currencies with more hawkish central bank regimes.

As in the previous releases, a lot hinges on how market sentiment fares for the most part of the week. Risk-on flows stemming from waning recession fears could keep a lid on Loonie sell offs.

In this case, keep an eye out for intraday short CAD positions opportunities, especially against currencies from countries who still have high expectations of further interest rate hikes ahead.

But ahead, NFP releasing at the same time, volatility and directional biases will have an increased level of uncertainty, so be very mindful of your risk management decisions around that time.

Potential Alternative Scenario:

A surprise upbeat Canadian jobs figure would be divergent from both expectations and the slowing pace of employment gains so far this year. A positive read might even be enough to re-ignite hopes of a BOC hike later this month and draw in significant short-term Loonie support from both fundie and technical traders.

If risk-on flows are in play for the most part of the week, the Loonie might be in for a more sustained rally against its forex peers. In this scenario, look out for potential short-term long CAD positions against currencies with central banks still open to slowing the pace of interest rate tightening or pausing all together.