Price action was more mixed this week as traders once again had to battle between geopolitical risks and monetary policy events.

Despite continued conflict and uncertainty in Ukraine, it appears that the “war” trade faded a bit this week as oil and gold fell against a bounce in crypto and equities.

In FX, the comdolls rallied late in the week to take the top spots after a sluggish start on Monday and Tuesday.

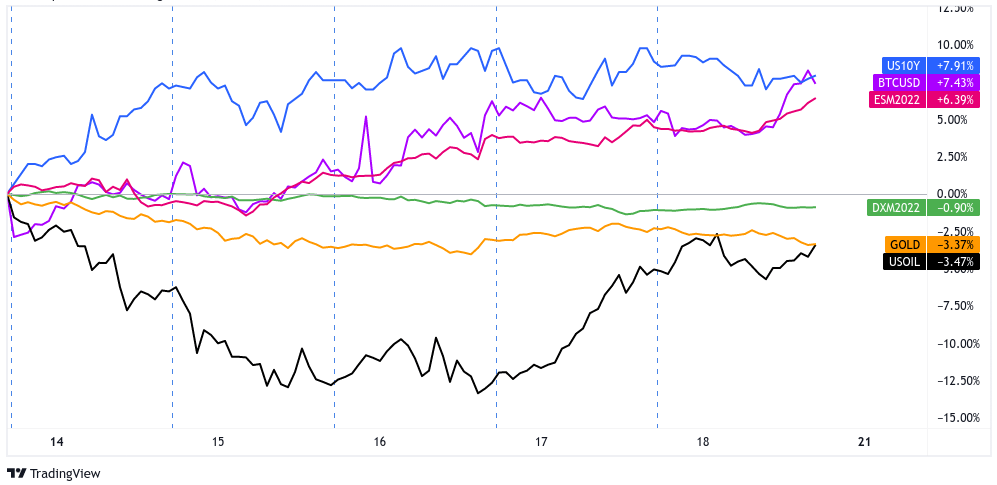

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10YR Yield, Bitcoin Overlay 1-Hour

As mentioned in the into, oil & gold moved lower early week, likely a reaction to headlines and speculation on Monday and Tuesday suggesting that ceasefire talks between Russia and UKraine were progressing.

Oil was possibly getting hurt as well from headlines out of China that lockdowns were imposed to stem the outbreak of COVID-19 cases.

Bond yields continued its broad upswing early in the week with the 10-yr U.S. Treasury yield topping out around 2.19%. Traders were likely positioning ahead of the highly anticipated FOMC statement on Wednesday, expecting the Fed to announce several rate hikes for 2022. This was also a likely contributor to the early week weakness in equities, as possibly in gold as well.

Risk sentiment seems to have been the main driver on Wednesday, possibly focusing on somewhat optimistic talks between Russia and Ukraine. Equities and crypto drifted higher, while the earlier drop in oil steadied around $95/bbl – $99/bbl ahead of the FOMC statement.

We eventually get to the FOMC event, where they hiked the Fed Funds rate by 25 bps rather than 50 bps, but signals six more hikes for 2022. On the announcement, we saw a pop higher in risk assets after the event, which may have been traders pricing in a bit more certainty now that the Fed’s 2022 plans have been made known.

Thursday’s price action was relatively tame in most markets. Oil was the outlier as it rallied 9% on the session, trading back above $100/bbl. Gold was also higher to $1950, signaling traders may have been pricing in new developments between Ukraine and Russia (e.g. “Kremlin reportedly dismissed news of progress in Ukraine-Russia peace talks”, fears Russia may miss debt payments).

Equities and bond yields moved into the green later in the day (Greenback moved lower), possibly a risk sentiment reaction to news that Russia was able to make payments in dollars and that the money would soon be distributed to bondholders.

On Friday, risk sentiment continued to shift positive, despite calls from Fed members Bullard, Wallard and others for aggressive Fed hikes to combat high prices.

It’s possible that traders were a bit relieved that the result of the call between U.S. President Biden and Chinese President Xi today was to focus on the humanitarian situation in Ukraine, and that both sides want to coexist in peace with each other.

In the FX space, it looks like risk sentiment was the core driver for price action this week; safe havens were broadly lower, while AUD, NZD and CAD closed out the week strong.

But there was a little bit of variance from recent behavior from the majors as the euro recovery continued. This was a bit of a surprise given net negative economic updates from Europe, and rhetoric from ECB officials fading hopes that a rate hike is needed soon.

This suggests traders were buying back the heavily shorted euro as war tensions eased a bit, and if it weren’t for the last minute rally in the comdolls, the euro actually would have won out the week.

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

One year inflation expectations rise to +6.0% from +5.8% – NY Fed Survey

U.S. producer prices rise 0.8% m/m in February vs. 1.2% m/m in January

New York manufacturing unexpectedly shrinks from 3.1 to -11.8, the lowest since 2020

NAHB Housing Market Index: 79 in March vs. 81 forecast/previous

Federal Reserve approves its first Fed Funds interest rate hike in more than three years, signals the potential for six more hikes in 2022

Philly Fed manufacturing Index rose 11 points to 27.4 in March

U.S. housing starts spiked by 6.8% y/y in March vs. 5.5% y/y in Feb.

U.S. weekly jobless claims falls to 214,000, more than expected

Fed Governor Waller says half-point rate hikes could be needed as ‘inflation is raging’

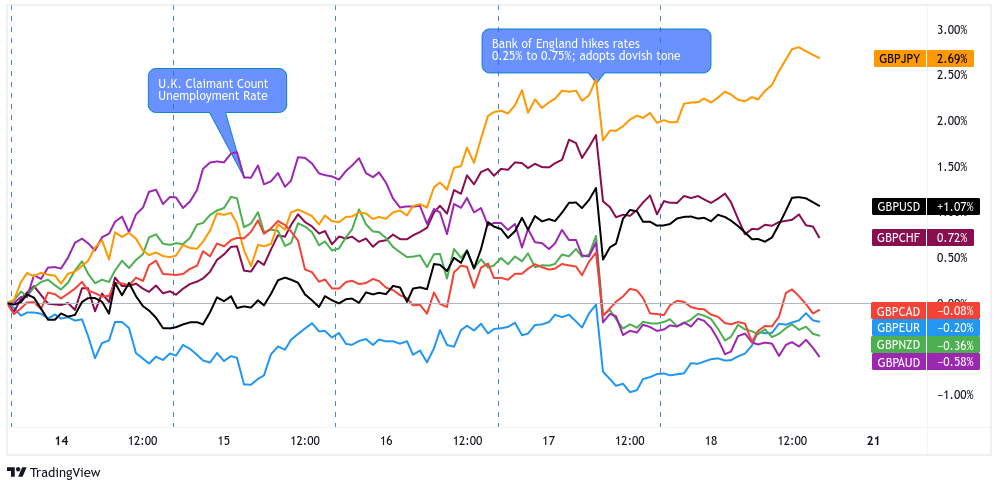

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

The Conference Board Leading Economic Index for the U.K. in Jan. 2022: +0.2% to 82.6

UK unemployment falls below pre-pandemic rate to 3.9%; Average weekly earnings rise by annualized 4.8%

U.K.’s Boris Johnson visits Saudi Arabia and UAE, seeking more oil output

Bank of England hikes rates again, adopts dovish tone as Ukraine war adds to inflation concerns

EUR Pairs

Germany February wholesale price index 1.7% vs 2.3% in January

France trade balance increased slightly in January 2022 to -€9.6B

German ZEW economic sentiment falls at record pace In March to -39.3 vs. 54.3 in February

ECB’s de Guindos says Europe will not go into recession due to Ukraine war

Sweden’s Riksbank Chief won’t rule out a rate hike in 2022

ECB President Lagarde stressed policy flexibility as war risks new price trends

Annual inflation up to 5.9% in the euro area; Up to 6.2% in the EU

Euro area international trade in goods deficit €27.2B in January; €36.0B deficit for EU

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

SECO lowers Swiss growth forecast for 2022 to 2.8% due to higher inflation and Ukraine conflict

Switzerland trade balance: CHF 5.95B in February vs. CHF 3.18B; exports jump +10.3% m/m

CAD Pairs

Overlay of CAD Pairs: 1-Hour Forex Chart

Canadian manufacturing sales were up 0.6% m/m in Jan; +13.4% y/y

Canada housing starts rise 8% in February

Canada core CPI rose by +5.7% in February vs. +3.3% rise in January

Canada wholesale sales rose 4.2% in January

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

New Zealand overseas visitor arrivals were 4K in Jan. 2022 vs. 5.4K in Jan. 2021

Global Dairy prices fell -0.9% to $5.039 at the latest auction

New Zealand Services Index February of 2022: 48.6 vs. upwardly revised 46.0 in January

New Zealand economy expanded by 3.0% in Q4 2021 vs. 3.3% consensus

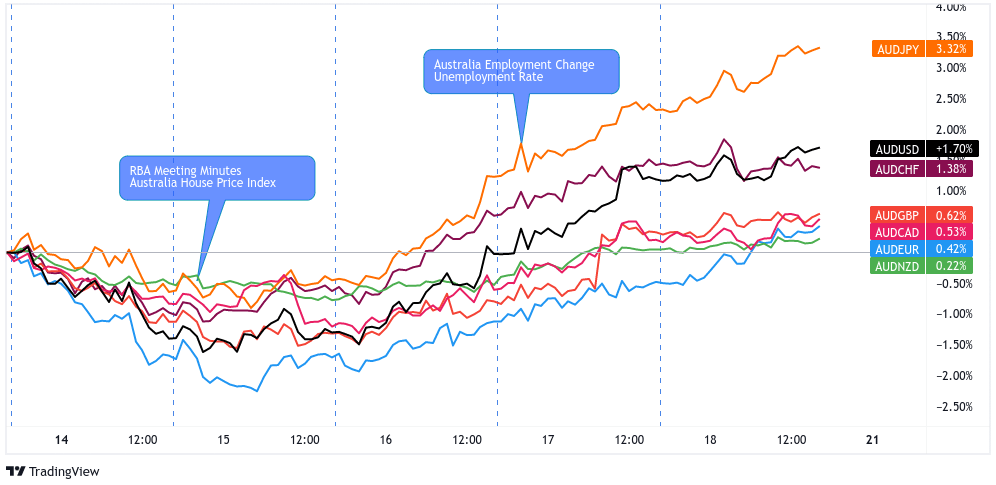

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

RBA meeting minutes: Russia’s war on Ukraine is a new source of uncertainty

RBA: Australian economy is resilient, sees a central case to stay patient

Australia House price Index rose +4.7% q/q, 23.7% y/y – ABS

AU Westpac leading index rises from -0.5% to -0.25% in February

Australian economy added +77.4K jobs in February vs. a +36K forecast; jobless rate moved lower from 4.2% to 4.0% vs. 4.1% forecast

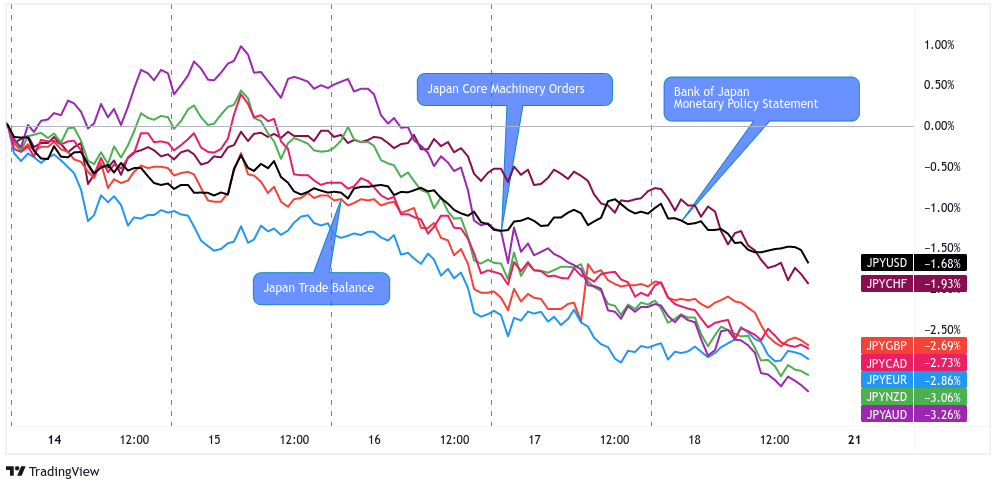

JPY Pairs

Japan posts bigger-than-expected trade gap of 1.03T JPY as energy imports jump in February

Japan to fully lift COVID-19 restrictions as infections slow

BOJ Governor Kuroda says they will keep easing until inflation target is reached

Japan core machinery orders: -2.0% m/m in January vs. 2.2% forecast, +3.1% in December