HALF a million mortgage holders are currently on a standard variable rate (SVR) mortgage but some pay much more than others.

This is because the SVR is the background rate that the lender charges interest at.

1

Banks and building societies have the ability to set this rate themselves and when the Bank of England increases the base rate, lenders typically increase their SVRs in line.

Over 773,000 households are on their bank’s SVR but rates vary between 6.79% and a whopping 9.49%, according to new data from TotallyMoney.

This is because lenders can set their SVR at whatever level they like, they can also increase or decrease it by whatever margin they choose, even if it’s not necessarily in direct line with any change from the Bank of England.

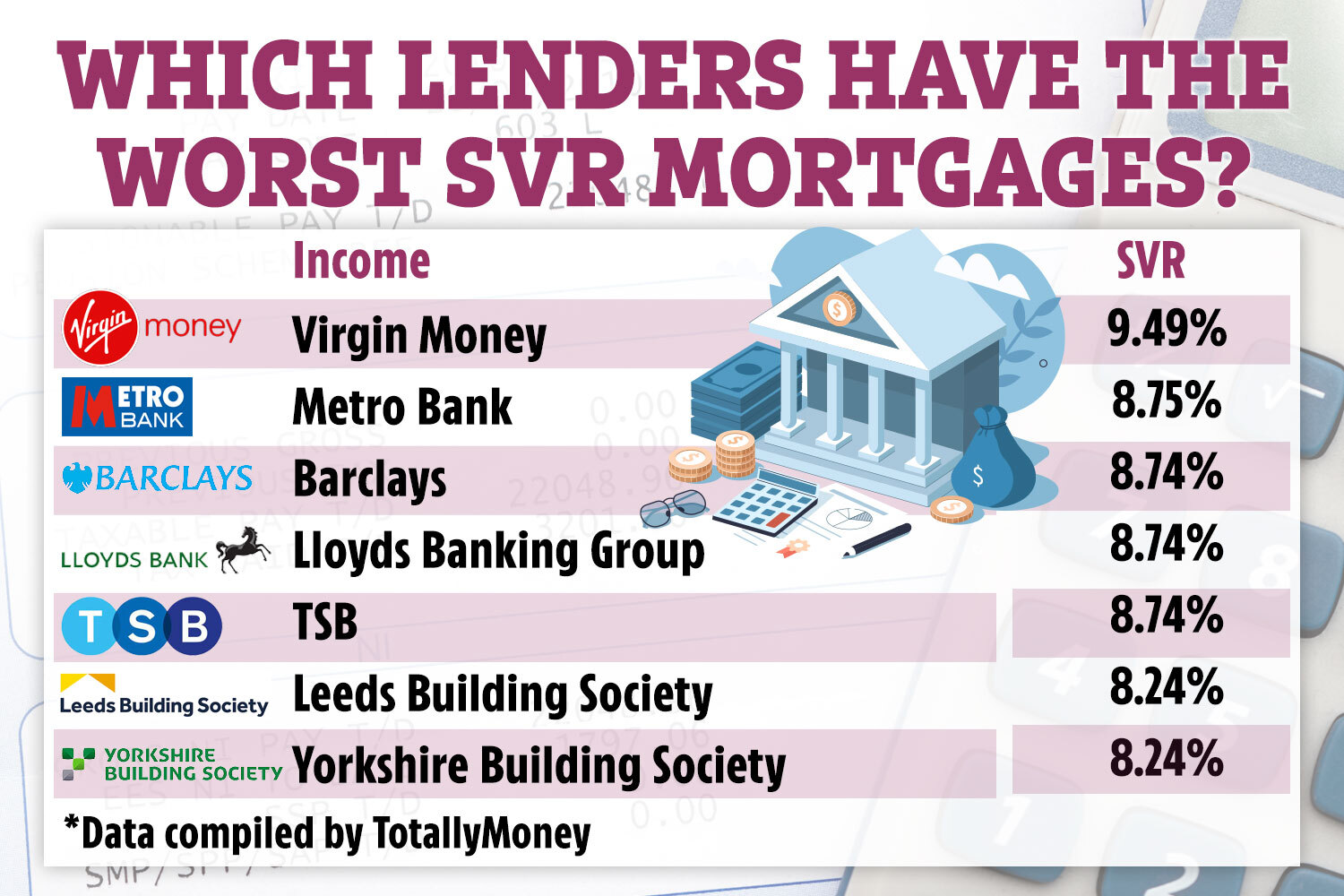

For example, Virgin Money tops the table, charging SVR customers 9.49% or 4.24 percentage points more than the Bank of England’s base rate which currently sits at 5.25%.

Metro Bank charges SVR customers 8.75% – 3.5 percentage points more than the base rate.

Barclays, Lloyds Bank and TSB charge SVR customers 8.74% – 3.49 percentage points more than the base rate.

Both Leeds and Yorkshire Building Society charge SVR customers 8.24% – 2.99 percentage points more than the base rate.

Co-op Bank charges SVR customers 8.12% and the Bank of Ireland charges the same customers 8.04%.

Most read in Money

But at the other end of the spectrum Skipton Building Society sets its SVR at 6.79%, which is only marginally higher than the average two-year fixed deal of 6.70%.

HSBC charges SVR customers 6.99%, Coventry Building Society charges 7.49%, Santander charges 7.5%, NatWest charges, 7.74% and Nationwide charges 7.99%.

Most experts would recommend looking into fixed deals if you’re at a lender with extremely high SVR rates.

Nicholas Mendes, mortgage technical manager at John Charcol, said: “There are many stories of homeowners who are on a lender’s SVR but aren’t aware that they can move on to a lower rate fixed deal with the existing lender via a product transfer.

“Otherwise, outside of looking at a product transfer with the existing lender, homeowners would need to remortgage to switch provider.”

It comes as 800,000 households face a huge mortgage shock when their fixed-rate deal expires before the end of 2023, according to UK Finance.

The Bank of England is expected to hike interest rates for the 15th consecutive time on Thursday.

Lenders will be poised to raise their SVR offers once again but the exact amount they’ll go up by will vary depending on the provider.

How can I switch and get the best deal?

If you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

But there are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you’re remortgaging and your loan-to-value ratio has changed this could also give you access to better rates than before.

A change to your credit score or a better salary could also help you access better rates.

If you have a fixed rate, you could see higher rates when you come to the end of the current term after 14 bank rate rises since December 2021.

And if you’re nearing the end of a fixed deal in the next six months it’s worth contacting your broker now to lock in a rate.

If they come down between now and the end of your deal, you can always apply for another rate before you remortgage.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what’s available.

You can also go to a mortgage broker who can compare for you, with most offering free advice to secure you the best deal for you.

Some brokers charge for advice, so ask them first.

It could cost a couple of hundred pounds but it might save you thousands on your mortgage overall.

You’ll also need to factor in fees for the mortgage, though some have no fees at all, or you can add it to the cost of the mortgage, but beware that means you’ll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember, if you decide to remortgage to a new lender you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks, and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

It’s possible to avoid new affordability checks by remortgaging to a new deal with your existing lender, provided you don’t want to borrow more or extend your term.