The modus operandi behind investment fund PGIM Jennison Global Equity Opportunities is to identify companies that are likely to dominate the corporate world in the next decade – and then invest in them big time.

It’s a bold investment strategy, all built around growth, and not without risk, especially in the short term.

But it’s a rather compelling investment proposition given its emphasis on exciting themes such as the boom in artificial technology (AI); new drug developments; the demand for luxury goods (especially in Asia); and the digitalisation of financial services in Latin America.

‘We try to spot unique business models that will deliver strong earnings growth long into the future,’ says Mark Baribeau, who manages the £580 million fund out of Jennison’s offices in New York and Boston – Jennison Associates being one of several investment businesses owned by PGIM.

‘Invariably, the companies have identifiable competitive advantages that means they can sustain their market position. And they can make big profit margins.’

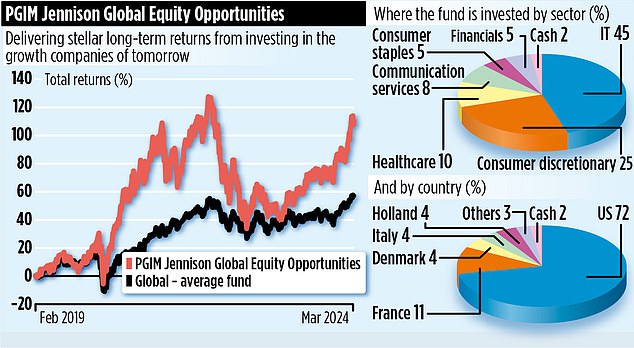

The result is a portfolio comprising just 36 stocks, most of which are listed in the United States, but all have global reach.

Many are familiar names including the likes of AI specialist Nvidia, Microsoft and Amazon – the fund’s three biggest holdings. These are all members of the ‘magnificent seven’ club: technology-based companies which have been primarily responsible for the strong performance of the equity market in the United States.

The fund’s performance numbers are good although they also highlight how volatile some of the prices of the stocks it holds can be. Over the past year, it has registered a 35 per cent return, but over the two previous discrete one-year periods, the fund has incurred losses of 5.5 per cent (year to March 2023) and 15.7 per cent (year to March 2022).

‘Yes, the prices of many of the growth stocks we held in 2022 were hit by higher interest rates and economic downturn,’ says Baribeau. ‘But their recovery started in 2023 and it looks like this will continue well into this year.’

Although the fund has more than 70 per cent of its assets in the United States, Baribeau says it’s not a deliberate policy.

‘We don’t take a top-down view on markets,’ he says. ‘We jump on investment opportunities wherever they present themselves. It’s coincidental that most happen to be in the US.’

A big theme in the fund outside of the United States is continued global demand for luxury goods, especially from the burgeoning middle classes in some of the economies of South East Asia.

‘Businesses such as LVMH, Hermes and Ferrari – all headquartered in Europe – are phenomenal companies,’ says Baribeau. ‘They can’t be replicated which makes them compelling from an investment point of view.’

He is also excited about the digitalisation of financial services in Latin America – a top ten fund holding is Argentine company MercadoLibre which is listed in the United States. The manager says a concentrated portfolio – built around best of breed companies – is the only way to deliver stellar returns for investors.

The fund’s five-year performance numbers prove his point. Its overall return of 117 per cent compares with the 61 per cent gain registered by the average global fund.

Annual fund charges are reasonable at 0.83 per cent and the fund can be bought on most mainstream investment platforms.

#fiveDealsWidget .dealItemTitle#mobile {display:none} #fiveDealsWidget {display:block; float:left; clear:both; max-width:636px; margin:0; padding:0; line-height:120%; font-size:12px} #fiveDealsWidget div, #fiveDealsWidget a {margin:0; padding:0; line-height:120%; text-decoration: none; font-family:Arial, Helvetica ,sans-serif} #fiveDealsWidget .widgetTitleBox {display:block; float:left; width:100%; background-color:#af1e1e; } #fiveDealsWidget .widgetTitle {color:#fff; text-transform: uppercase; font-size:18px; font-weight:bold; margin:6px 10px 4px 10px; } #fiveDealsWidget a.dealItem {float:left; display:block; width:124px; margin-right:4px; margin-top:5px; background-color: #e3e3e3; min-height:200px;} #fiveDealsWidget a.dealItem#last {margin-right:0} #fiveDealsWidget .dealItemTitle {display:block; margin:10px 5px; color:#000; font-weight:bold} #fiveDealsWidget .dealItemImage, #fiveDealsWidget .dealItemImage img {float:left; display:block; margin:0; padding:0} #fiveDealsWidget .dealItemImage {border:1px solid #ccc} #fiveDealsWidget .dealItemImage img {width:100%; height:auto} #fiveDealsWidget .dealItemdesc {float:left; display:block; color:#004db3; font-weight:bold; margin:5px;} #fiveDealsWidget .dealItemRate {float:left; display:block; color:#000; margin:5px} #fiveDealsWidget .dealFooter {display:block; float:left; width:100%; margin-top:5px; background-color:#e3e3e3 } #fiveDealsWidget .footerText {font-size:10px; margin:10px 10px 10px 10px;} @media (max-width: 635px) { #fiveDealsWidget a.dealItem {width:19%; margin-right:1%} #fiveDealsWidget a.dealItem#last {width:20%} } @media (max-width: 560px) { #fiveDealsWidget #desktop {display:none;} #fiveDealsWidget #mobile {display:block!important} #fiveDealsWidget a.dealItem {background-color: #fff; height:auto; min-height:auto} #fiveDealsWidget a.dealItem {border-bottom:1px solid #ececec; margin-bottom:5px; padding-bottom:10px} #fiveDealsWidget a.dealItem#last {border-bottom:0px solid #ececec; margin-bottom:5px; padding-bottom:0px} #fiveDealsWidget a.dealItem, #fiveDealsWidget a.dealItem#last {width:100%} #fiveDealsWidget .dealItemContent, #fiveDealsWidget .dealItemImage {float:left; display:inline-block} #fiveDealsWidget .dealItemImage {width:35%; margin-right:1%} #fiveDealsWidget .dealItemContent {width:63%} #fiveDealsWidget .dealItemTitle {margin: 0px 5px 5px; font-size:16px} #fiveDealsWidget .dealItemContent .dealItemdesc, #fiveDealsWidget .dealItemContent .dealItemRate {clear:both} }