MILLIONS of homeowners could face higher mortgage repayments as the Bank of England looks to hike interest rates again.

An unexpected rise in the UK’s inflation rate could cause the Bank of England (BoE) to up interest rates again to keep a lid on soaring prices.

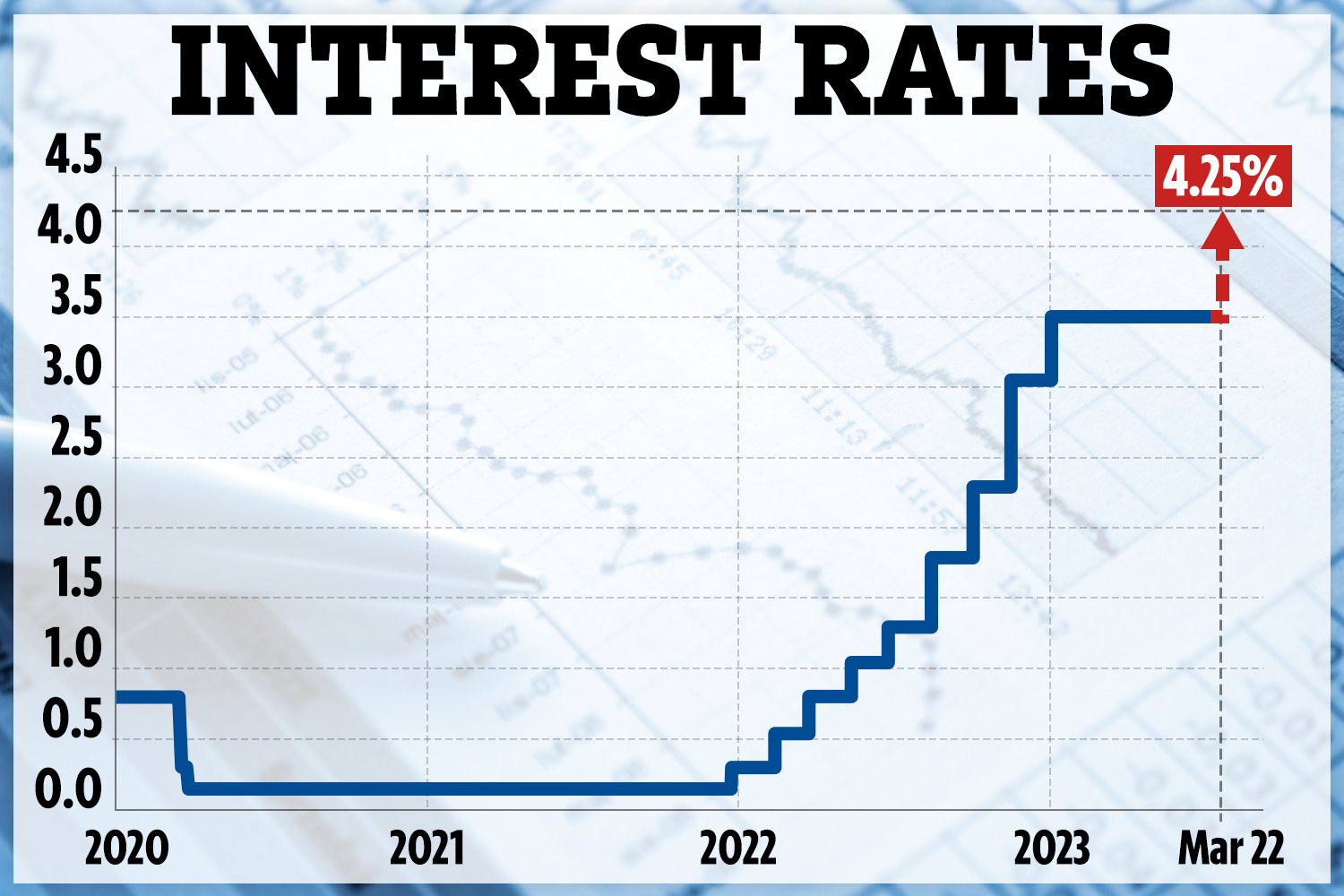

1

Experts had been on the fence about whether the central bank will opt for another rise in its Monetary Policy Committee (MPC) meeting today (March 22).

But the surprise jump in inflation, from 10.1% in January to 10.4% in February, could make it harder for the Bank to justify leaving rates as they are.

The Bank has hiked rates for ten consecutive months since December 2021 when it was at a historic low of 0.1%.

Some economists think the MPC will increase the base rate by at least 0.25 percentage points from 4% to 4.25%.

The financial markets are also confident of the increase, with traders pricing in a 99% probability that the rate will be hiked.

This means that a change in rate has been anticipated and priced into the value of stocks by the market.

Economists have said the Bank is walking a tightrope since the last few weeks of financial market rollercoasters and bank rescues have highlighted the risks and potential fallouts from higher interest rates.

The move will make the cost of borrowing, including loans, credit cards and mortgage repayments more expensive.

Most read in Money

For the average UK property costing £270,708 on a variable rate and with a 75% LTV, monthly mortgage repayments would increase by £26 a month, according to data from TotallyMoney and Moneycomms.

When compared to December 2021, this means repayments could be a whopping £456 more.

But the exact amount that your mortgage repayment will rise by will depend on the type of mortgage you have.

Tracker mortgages are directly tied to the BoE base rate and around 715,000 households with this type of mortgage will see repayments rise straight away.

Around 191million households on standard variable rates (SVRs) are likely to see their monthly bill rise if their bank decides to pass on the increase.

Anyone with a fixed mortgage won’t see rates increase as they are locked in to a rate for a set period.

But when these homeowners come to remortgage, they will face a shock with higher repayments as they’ll be forced to take out fixed deals with much higher rates.

Exactly how much more depends on the size of the mortgage, the rate you fixed at, the new rate and the loan-to-value when you remortgage.

It is estimated that 5.2million mortgages may be exposed to changes in interest rates from June 2022 to the end of June 2024.

And around 360,000 of these mortgage borrowers could face payment difficulties as a result, according to the Financial Conduct Authority (FCA).

High-street banks use the Bank’s base rate to work out the interest rates it offers to customers.

This means the move is pushing up borrowing costs, including on mortgages, though savers may get better rates on their nest egg.

Andrew Hagger, personal finance expert at Moneycomms.co.uk, said: “It appears that UK interest rates may have finally peaked in this current cycle as the Government banks on inflation falling sharply throughout the remainder of 2023.

“But the current high rates are of little comfort to consumers struggling to make ends meet and particularly those facing an additional huge payment shock when they come to renew their fixed rate mortgage in the coming months.”

Martin Lewis previously warned that millions of homeowners face a “huge payment shock” in the Spring.

But fixed mortgage rates are currently at a six-month low, according to MoneyFacts.

Both the average two- and five-year fixed rates fell month-on-month for the fourth month running.

Two-year fixes were down to 5.32%, while five-year fixes were down 5%.

Mortgage rates shot up to record highs last autumn after the mini-Budget, but have since come down.

But they are still higher than before the BoE started hiking rates when many fixed at historic low rates.

Rachel Springall, finance expert at Moneyfacts, said that while it’s encourafing to see fixed rates falling, variable interest rates are “rising significantly”.

She added: “The average SVR has now breached 7% for the first time since October 2008, which means borrowers will be in for a shock if they are about to revert from a low fixed rate deal.”

Households usually end up on an SVR at the end of a fix and they are usually far higher, so getting a new fix can save you cash.

How to choose the best mortgage deal

There are lots of factors to consider when searching for the best mortgage deals.

The amount you can borrow and interest rate are important factors but you should also consider the type of mortgage.

Do you want the certainty of a fixed-rate mortgage or the flexibility of a tracker that could get cheaper rates and doesn’t have exit fees?

There are mortgage calculators online that will let you compare the monthly cost of a mortgage based on the interest rate and any fees.

A lender or mortgage broker will be able to offer advice on the best type of mortgage deal to meet your needs.

Shop around for the best mortgage deals rather than opting for the first bank you see.

Remember a bank or building society will only offer its own options which limits your choice.

You can also use a comparison website to find deals across the market based on your level of deposit and whether you want a fixed or variable rate.

A comparison website will usually let you search for all types of home loans such as for first-time buyers or the best buy-to-let mortgage deals.

This will give you an indication of what is on offer but you will need to do the application yourself.

Some lenders may not be on comparison websites so it is worth searching directly online as well.

Alternatively, a mortgage broker can help search the market more widely and find the most suitable deals for you.

Is it better to get a mortgage from a bank or a broker?

A bank may offer the best mortgage deal for you but shop around before you commit.

This is because a bank adviser will only offer their own products.

Limiting yourself to one bank’s products could mean you end up paying more than you needed to or you may not even meet their criteria.

Alternatively, a broker can use their market knowledge to help decide which type of mortgage and lender is best for you.

This could be of benefit if you are self-employed or have a poor credit rating as they may have more experience dealing with these sorts of applications.

It saves time on doing multiple applications, as you just tell your broker your income and expenses and they will work out the best mortgage you can get.

They can usually help with your application and will fight your corner to get you approved.

A broker will be able to advise on a range of products from different lenders, but these may also be limited to a panel so you should check if they are tied or work across the whole market.

There may, however, be extra fees when using a broker.

A mortgage may have an application or product fee but a bank adviser won’t charge anything on top of that.

In contrast, a mortgage broker may have their own fees for their advice.

When should I start looking for a new mortgage deal?

Getting your mortgage prepared when buying your first home can make you more attractive to sellers as they can see you have finance in place and are serious about proceeding with a purchase.

It can take a couple of hours or a few days in more complicated cases to get a mortgage in principle.

This gives you an idea of how much you can borrow, and you can usually get a decision within hours or a few days in more complicated cases.

You can do a full application once you have had an offer on a property accepted.

It can take four to six weeks for a mortgage to be approved depending on how much information a lender needs.

A seller will usually wait, once they have accepted your offer, for you to get your mortgage sorted.

But having an idea of what you can borrow in advance will speed up your purchase and ensure you don’t miss out on your dream home.

More preparation is needed if you are remortgaging.

A lender will move you onto a more pricey SVR once your mortgage deal comes to an end.

That means you could have been on one of the best mortgage deals and suddenly your monthly repayments will increase.

You should start looking for a new mortgage at least three months before your deal ends.

It can take at least two months for a remortgage to complete so you need to allow time to find a new deal and make the application.

Mortgage offers typically last up to six months, so you could start early if you spot a good rate and time the start date so you avoid any exit fees and move smoothly onto the new rate once your deal expires.