What are you selling? How are you selling it? Why would anybody want to buy from you? Where can they find your product or services? After all, even the greatest invention will not launch a successful business if people do not know where to find it. Once upon a time the most important aspect of marketing for a brick-and-mortar business was location, location, location—indeed, to a large extent it still is. But today, in the virtual world that is the internet, location may be replaced by Facebook, LinkedIn, Instagram, YouTube, and TikTok.

Your marketing plan is all about knowing your target market and making sure those customers know where they can find you. However, before you can start reaching out to your public, you need to have a marketing strategy that defines what you are selling, at what price(s), from where, and how you are going to spread the word. To simplify, you can use the four Ps of marketing: product, price, place, and promotion. In this article, we will tackle the first two Ps.

Defining Your Product

Product, the first of the four Ps, refers to the features and benefits of what you have to sell (as usual, we’re using the term as shorthand for products and services). Many modern marketers have a problem with this “P” because it doesn’t refer to customer service, which is an important part of the bundle of features and benefits you offer to customers. However, it’s pretty easy to update product by simply redefining it to include whatever services are offered.

There are a number of issues you need to address in your product section. You need to first break out the core product from the actual product. What does this mean? The core product is the nominal product. Say you’re selling snow cones. A snow cone is your core product. But your actual product includes napkins, an air-conditioned seating area, parking spaces for customers, and so forth. Similarly, an electronics store nominally sells computers, tablets, and devices, but it also provides expert advice from salespeople, a service department for customers, opportunities to comparison shop, software, and so on.

It’s important to understand that the core product isn’t the end of the story. Sometimes the things added to it are more valuable than the core product itself. That’s not necessarily bad, but failing to understand this is likely to lead to trouble.

Defining Your Customer

Marketing great toys for five-year-olds to teenagers isn’t going to work, nor will selling singles cruises to married couples or milkshakes to people who are lactose intolerant. While you may not be able to define everyone who is a likely customer, you need to know your target audience and know it well.

You need to talk about your ideal customer as if he or she is someone you know very well. For example, she or he is twenty-five to twenty-nine years of age, earning x amount of money, has no children yet, and earned a college degree.

A new Italian restaurant might say it’s going for families eating out on a budget who live within a five-mile radius of its location. It might quote Census Bureau figures showing there are 12,385 such families in its service area. Even better, it would cite National Restaurant Association statistics about how many families it takes to support a new Italian restaurant.

A bicycle seat manufacturer might have identified its market as casual middle-aged cyclists who find traditional bike seats uncomfortable. It may cite American College of Sports Medicine surveys, saying that sore buttocks due to uncomfortable seats is the chief complaint of recreational bicyclists.

It is important to quantify your market’s size if possible. If you can point out that there are more than six million insulin-dependent diabetics in the United States, it will bolster your case for the new easy-to-use injection syringe your company has developed.

In addition to fully defining your product, you need to address other issues in your marketing plan. For instance, you may have to describe the process you’re using for product development. Tell how you come up with ideas, screen them, test them, produce prototypes, and so on.

You may need to discuss the life cycle of the product you’re selling. This may be crucial in the case of quickly consumed products such as corn chips and in longer-lasting items like household appliances. You can market steadily to corn chip buyers in the hopes they’ll purchase from you frequently, but it makes less sense to bombard people with offers on refrigerators when they need one only every ten or twenty years. Understanding the product’s life cycle has a powerful effect on your marketing plan, as does knowing logical buying habits. For example, one popular department store was offering a buy-one-get-one-at-half-price deal on fine jewelry. The deal was not generating a strong response because most people do not shop for expensive jewelry in “bulk” quantities but instead take a personalized approach. In fact, such a promotion was cheapening the products.

Other aspects of the product section may include a branding strategy, a plan for follow-up products, or line extensions. Keeping these various angles on products in mind while writing this section will help you describe your product fully and persuasively.

The Universally Wrong Assumption

It’s always easy to market something by saying, “Everyone will love it!” But that’s the kiss of death in marketing. No matter how wonderful a product or service may appear, nothing will please “everyone.” Therefore, each product or service must have a defined market if you are serious about your business succeeding. Narrow your demographic group by positioning your product appropriately. That may include more than one place, such as bicycles, which might go under “bikes” or “sporting goods,” but not “everywhere” or for “everyone.”

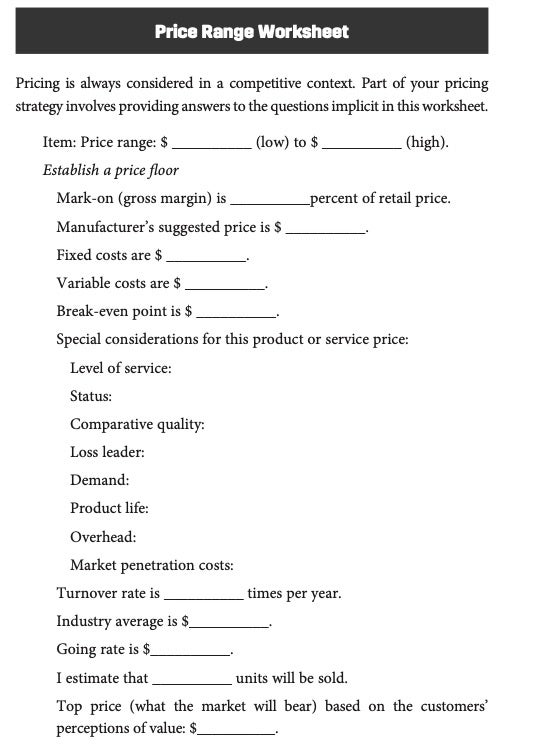

How to Set Prices

One of the most important decisions you have to make in a business plan is what price to charge for what you’re selling. Pricing determines many things, from your profit margin per unit to your overall sales volume. It influences decisions in other areas, such as what level of service you will provide and how much you will spend on marketing. Pricing has to be a process you conduct concurrently with other jobs, including estimating sales volume, determining market trends, and calculating costs. There are two basic methods you can use for selecting a price.

One way is to figure out what it costs you altogether to produce or obtain your product or service, then add in a suitable profit margin. This markup method is easy and straightforward, and assuming you can sell sufficient units at the suggested price, it guarantees a profitable operation. It’s widely used by retailers. To use it effectively, you’ll need to know all of your costs as well as standard markups applied by others in your industry.

The other way, competitive pricing, is more concerned with the competition and the customer than with your own internal processes. The competitive pricing approach looks at what your rivals in the marketplace charge, plus what customers are likely to be willing to pay, and sets prices accordingly. The second step of this process is tougher—now you have to adjust your own costs to yield a profit. Competitive pricing is effective at maintaining your market appeal and ensuring your enterprise’s long life, assuming you can sell your goods at a profit.

Pricing is inherently strategic. You can use prices to attack competitors, position your business, test a new market, and/or defend a niche. The only hard-and-fast rule to follow in setting prices is: Set prices carefully, deliberately, knowledgeably, and with long-range goals in mind. All the rest are footnotes.

Setting Prices Objectives

Before you can select a pricing approach, you need to know your pricing objectives. Following are questions to ask yourself about your pricing goals:

- Which is more important: higher sales or higher profits?

- Am I more interested in short-term results or long-term performance?

- Am I trying to stabilize market prices or discourage price-cutting?

- Do I want to discourage new competitors or encourage existing ones to get out of the market?

- Am I trying to quickly establish a market position, or am I willing to build slowly?

- Do I have other concerns, such as boosting cash flow or recovering product development costs?

- What will the impact of my price decision be on my image in the market? How does that fit the image I want?

- What reputation do I want—”sells low and beats prices” or “provides higher-quality goods and/or more personalized service”?

Answer these questions first, then prioritize them to decide how each objective will weigh in setting your pricing strategy. That way, when you present your price objectives in your business plan, it will make sense and be supported by reasonable arguments integrated with your overall business goals.

Further Pricing Thoughts

Why is setting price so tough? Perhaps because nobody really understands it. Pricing is as much art as science. Price too low and lose money. Price too high and lose customers. Price in the middle and lose position. It seems like a no-win situation for most small business owners. There is no mechanical way to grind out the right price. There is no shortcut. It’s a matter of doing your research, and then it often comes down to some trial and error.

Small businesses simply cannot afford to compete on price. Lowballing drives small businesses out of business, cheapens their image, and costs them the opportunity to upgrade their customer base. It’s a race to the bottom and simply does not work.

There’s always someone willing to sell on price alone. Sometimes the price competition comes from a giant like Walmart, which buys in such huge quantities that suppliers cave in and pare their margins to the bone. (Walmart has revolutionized inventory management and distribution, which allows them to make vast profits on thin margins. They aren’t just competing on price.) Sometimes the competitor is a newcomer who thinks—erroneously—that the best way to enter a market is to buy market share with loss-leader pricing.

The two main ways to deal with price competition are to meet the price (cave in and watch your margins evaporate) or to reposition yourself so the price competition is indirect (repositioning).

This article is from Entrepreneur.com