Risk sentiment tossed and turned throughout the week leading to a mostly choppy market as traders balanced broad recession fears with major economic & central bank event updates.

The market spotlight was on Chinese stimulus updates early on before the focus shifted to global PMI survey results midweek.

Record high U.S. 10-year bond yields also took center stage then, along with equity market rallies that fizzled out pretty quickly.

Before I tell all the deets, lemme show you the biggest headlines first:

Notable News & Economic Updates:

🟢 Broad Market Risk-on Arguments

Over the weekend, PBOC and financial regulators met with bank executives and told lenders again to boost loans to support a recovery

U.S. equity indices manage to hold on to gains despite rising Treasury yields midweek, buoyed by expectations of strong Nvidia earnings

BOJ core CPI advanced from 3.0% to 3.3% year-over-year in July vs. estimated 2.9% figure

Nvidia shares rallied 3.2% in session and 9% after hours after the company saw Q2 revenue of $16B vs. expectations of $12.5B and provided a stronger than expected outlook for Q3 revenue

🔴 Broad Market Risk-off Arguments

PBOC announced a smaller than expected cut to its 1-year prime loan rate from 3.55% to 3.45% vs. 3.40% forecast and kept its 5-year rate steady at 4.20% instead of cutting to the 4.05% consensus

S&P downgrades multiple U.S. banks on growing liquidity worries, following Moody’s earlier downgrade on some regional lenders due to high commercial real estate exposure

U.S. 10-year bond yields surge to 2007 highs midweek on expectations of hawkish Fed rhetoric during Jackson Hole Symposium

New Zealand headline retail sales fell 1.0% q/q in Q2 vs. projected 0.4% dip, core retail sales slumped 1.8% q/q vs. estimated 0.2% decline

Global PMIs broadly disappoint, sparking broad risk-off sentiment across the board and forcing global bond yields to retreat

- Australia’s flash manufacturing PMI fell from 49.6 to 49.4 in August, services PMI down from 47.9 to 46.7 to reflect sharper pace of contraction

- Japanese flash manufacturing PMI ticked higher from 49.6 to 49.7 in August to signal slightly slower pace of contraction

- French flash manufacturing PMI rose from upgraded 45.1 reading to 46.4 in August, services PMI down from 47.1 to 46.7 vs. 47.5 forecast

- German flash manufacturing PMI ticked higher from 38.8 to 39.1 vs. 38.9 forecast in August, services PMI tumbled from 52.3 to 47.3 to reflect major shift to industry contraction

- U.K. Manufacturing PMI for August: 42.5 vs. 45.3; Services PMI at 48.7 vs. 51.5

- U.S. Flash Manufacturing PMI for August: 47.0 vs. 49.0 previous; Services PMI at 51.0 vs. 52.3 previous

European yields tumble as markets price in stronger odds of September ECB pause, possible BOE tightening peak

U.S. payrolls were likely 306K lower than previously estimated, as BLS weighs adjustments on warehousing and transportation

Fed officials share mixed views, as Boston Fed President Susan Collins suggests further hikes may be necessary while Philadelphia Fed President Harker sees interest rates at restrictive levels

On Friday, Fed Chair Powell reiterated that the Fed will hold policy at restrictive levels until its confident inflation will move below 2% sustainably; still open raising interest rates if appropriate

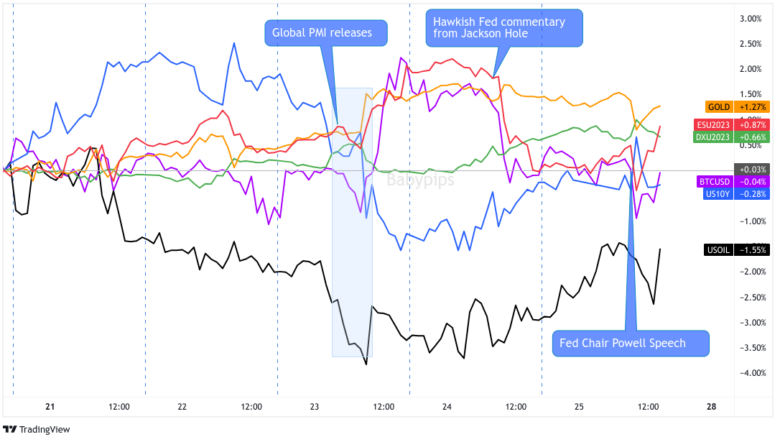

Global Market Weekly Recap

Weekend headlines revealed that Chinese regulators urged lenders to boost loan activity, which likely spurred some risk-on flows early on, but the gains were erased when the PBOC delivered underwhelming prime loan rate cuts during the Monday morning Asia session.

Market players were likely worried that Chinese policymakers are all bark and no bite, as doubts swirled that feeble policy stimulus will be enough to boost credit demand and provide support for property developers already defaulting on obligations.

Still, commodity currencies like the Aussie and Kiwi were able to benefit from news that Dalian iron ore prices were on the rise, which led investors to price in potentially stronger trade profits for export-driven economies.

U.S. bond yields were also on the rise during Monday’s New York session, with 10-year yields surging to their highest levels since 2007. Even so, the dollar struggled to take advantage of these gains while U.S. equities also advanced in anticipation of strong earnings figures from chipmaker Nvidia.

Treasury yields extended their rallies the next day with the 10-year UST yield climbing to fresh 16-year highs and lifting European yields in the process. Equity market rallies faltered, though, as traders braced themselves for a slew of global PMI readings.

Australia was first to print its numbers, although risk appetite seemed undeterred by another slump in business activity, as well as downbeat quarterly retail sales data from New Zealand.

It wasn’t until the euro zone released very dismal readings from the services sector of France and Germany that risk-off flows popped back in the markets. German bund yields took a beating, with the 10-year yield 13 bp to 2.52% on expectations that the ECB will likely pause tightening in September.

The U.K. economy followed through with its own set of PMI disappointments for both the manufacturing and services sectors, triggering a fall in 10-year gilt yields of 17 bp to 4.46%, which is its steepest one-day decline since March.

Uncle Sam wasn’t spared from the PMI meltdown, as flash manufacturing and services figures also pointed to slower activity, forcing 10-year yields to tumble to 4.19% and 2-year yields to slump to 4.97%.

Fortunately for U.S. equity indices, Nvidia earnings did not disappoint as the company boasted of stronger-than-expected revenue for the second quarter and even provided a much brighter outlook for Q3. During the regular session, the S&P 500 rose 1.1%, while the Nasdaq was 1.6% higher thanks to a broad bid in tech sector shares.

However, the equity market struggled and failed to hold on to its gains for very long as the spotlight turned to jitters ahead of the Jackson Hole Symposium.

Although FOMC officials were sharing mixed views on interest rates, many are still banking on Fed head honcho J-Pow to reiterate his hawkish bias and suggest that a September hike is one of the options on the table.

With that, the U.S. dollar has been able to pull up across the board, both on expectations of higher U.S. borrowing costs and risk-off vibes stemming from recession fears, which are now largely driven by higher borrowing costs…weird environment, right?

On Friday, traders were in wait-and-see mode during Asia and London trade, getting ready for the highly anticipated speech from Fed Chair Powell at the Jackson Hole Symposium. And the event didn’t disappoint as volatility picked up quickly after Fed members kept the door open for rate hikes ahead, citing high inflation rates and an unexpectedly strong employment environment.

This set the broad market in temporary risk-off/pro-dollar mode, along with a spike higher in bond yields. But the risk-off momentum moves were held in check, arguably on the idea that these comments were mostly as expected given recent economic data updates.

Overall, it was another positive week for the Greenback and gold, bond yields sit flat-to-negative and oil sits solidly in the red, signaling the rising speculation of recession fears.

Despite that main driver, equities were able to hold on to its gains as it likely found some support on the idea that we continue to inch closer to the peak interest rate hike scenario, potentially only one more Fed hike in November after an expected pause in September.

This post first appeared on babypips.com