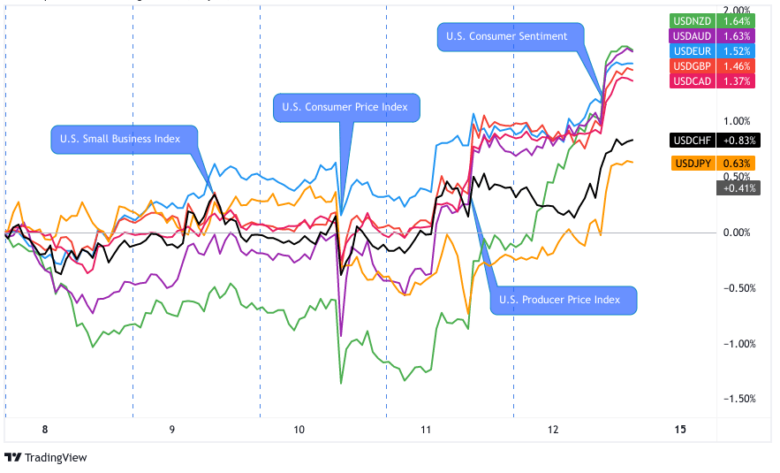

Dollar traders were on edge for the early part of the week as markets braced for the U.S. CPI release which later on underscored expectations for a Fed pause.

Pound pairs got an extra dose of volatility during the BOE decision, thanks to the central bank’s shift to a less hawkish stance.

Along with a return in risk-off flows, this allowed the U.S. dollar to regain advantage from its safe-haven appeal towards the end of the week.

USD Pairs

Even though the FOMC refrained from committing to a pause in last week’s meeting, dollar bulls were nowhere to be found ahead of the April CPI report.

The actual figures reflected softer inflationary pressures than expected, spurring expectations of rate cuts by next year. It didn’t help that debt ceiling negotiations didn’t bear much fruit, with the Friday talks postponed to give more time for staff-level discussions.

Broad risk sentiment shifted by Thursday towards risk aversion on weaker-than-expected data from China and the U.S., and instead of the recent run to hard metals and bonds for safety, traders were moving capital towards Greenback. With fears of both global recession and the U.S. debt ceiling growing, it makes sense that cash was king at the end of the week.

? Bullish Headline Arguments

Headline monthly CPI came in line with expectations of a 0.4% increase for April, faster than the earlier 0.1% uptick, while core CPI posted a higher than expected 0.4% month-over-month gain

Core producer prices rose by 0.2% month-over-month as expected in April, earlier reading upgraded to show a flat figure from the previously reported 0.1% dip

Fed Governor Michelle Bowman said on Friday that interest rates will likely need to move and be held higher if price pressures do not ease and the job market remains tight

? Bearish Headline Arguments

Headline CPI dipped from 5.0% to 4.9% year-over-year versus estimates of a 5.0% reading, marking the smallest 12-month increase since April 2021

Headline producer prices fell short with a 0.2% month-over-month uptick in April versus the projected 0.3% increase, bringing year-over-year rate down from 2.7% to 2.3% – its lowest reading since January 2021

Initial jobless claims came in at 264K versus the 245K estimate and earlier 242K figure, chalking up yet another pickup in unemployment for the past two weeks

Biden noted some progress in debt ceiling meetings with Congressional leaders early in the week, but talks scheduled for Friday were postponed to make more time for staff-level discussions

U.S. Preliminary consumer sentiment index for May: 57.7 (64.0 forecast) vs. 63.5 previous – University of Michigan

EUR Pairs

Overlay of EUR vs. Major Currencies Chart by TV

The shared currency unwound most of its post-ECB gains in the previous week, as traders continued to price in the possibility of a future rate hike pause or even easing.

This week’s mostly downbeat euro data threw more focus into the central bank’s hints of potentially slowing their tightening going forward, as industrial production data fell short of estimates.

? Bullish Headline Arguments

French trade deficit narrowed from 9.3 billion EUR to 8.0 billion EUR vs. estimated 9.5 billion EUR shortfall in March

? Bearish Headline Arguments

German industrial production sank by 3.4% month-over-month in March vs. estimated 1.6% decline, following earlier 2.1% gain

Euro zone Sentix investor confidence index fell from -8.7 to -13.1 to reflect worsening pessimism vs. projected improvement to -7.9

Italian industrial production tumbled by 0.6% month-over-month in March vs. estimated 0.2% uptick, adding to earlier 0.2% decline

GBP Pairs

Overlay of GBP vs. Major Currencies Chart by TV

Sterling tossed and turned during the BOE decision as the central bank also joined the “dovish hike” bandwagon by toning down their forward guidance.

Later in the week, the downbeat monthly GDP reading further stoked expectations of a tightening pause and perhaps even the possibility of a rate cut if economic data worsens.

? Bullish Headline Arguments

BRC retail sales monitor rose from 4.9% to 5.2% year-over-year versus estimated fall to 4.7% for April, reflecting stronger consumer spending based on same-store sales at retail level

Bank of England hiked interest rates by 0.25% as expected, with MPC members maintaining the 7-2 split in voting to increase rates or pause

BOE Monetary Policy Report featured upgrades to inflation forecasts from 3.92% in February announcement to 5.12% for the end of 2023 and from 1.42% to 2.28% for the end of 2024

Construction output increased by 0.2% month-over-month instead of falling by the estimated 0.4% figure in March

Industrial production rose by 0.7% vs. projected 0.1% uptick in March, earlier reading upgraded to show 0.1% dip from previously reported 0.2% decline

Preliminary business investment figure for Q1 2023 reflected 0.7% gain instead of the estimated 0.7% decline, rebounding over earlier 0.2% dip

? Bearish Headline Arguments

Halifax HPI showed 0.3% decline in house prices instead of the projected 0.2% uptick, marking the first decline for the year

U.K. economy contracted by 0.3% in March instead of posting another flat GDP reading, bringing the preliminary quarterly growth figure to a measly 0.1% expansion

BOE Governor Bailey mentioned that “if there were to be evidence of more persistent [inflationary] pressures, then further tightening in monetary policy would be required” then mentioned in an interview after the presser that they are nearing a point when the central bank could “rest in terms of the level of rates”

CHF Pairs

Overlay of CHF vs. Major Currencies Chart by TV

It was a light week in terms of top-tier data releases from Switzerland, allowing the franc to reap some gains off safe-haven flows and relatively hawkish words from SNB head Jordan.

? Bullish Headline Arguments

SNB Chairperson Jordan mentioned in a speech about the current challenges of monetary policy at the University of Applied Sciences that inflation is above their price stability range, higher than policymakers want

AUD Pairs

Overlay of AUD vs. Major Currencies Chart by TV

The Aussie took advantage of of the early anti-U.S. dollar movements and higher gold prices in the first half of the week before returning these gains when risk aversion popped its head back in the markets.

Downbeat inflation and trade data from China also likely weighed on copper prices, as well as other commodities, adding to losses for the higher-yielding AUD.

? Bullish Headline Arguments

NAB business confidence index improved slightly from -1 to 0 in April, as the employment component stabilized above its historical average

Retail sales posted another 0.4% month-over-month increase in March as expected, translating to 5.2% year-over-year growth

MI inflation expectations accelerated from 4.6% to 5.0% to reflect stronger estimates of price pressures over the next 12 months

? Bearish Headline Arguments

Australian building approvals fell 0.1% month-over-month in March instead of rising by the estimated 3.0% figure, following earlier 3.9% rise

China reported slower exports growth of 8.5% year-over-year in April, down from earlier 14.8% gain, and 7.9% slump in imports versus projected 0.2% decline

CAD Pairs

The Loonie managed to regain some ground early in the week, as crude oil prices turned higher and risk-on flows were in play.

However, the rallies fizzled out after the API and EIA U.S. oil inventory reports surprised traders with gains in stockpiles, turning attention to the narrative of weaker demand for oil down the road.

? Bullish Headline Arguments

Building permits jumped 11.3% month-over-month in March versus estimated 2.3% slump, earlier reading downgraded from 8.6% gain to a much lower 5.6% increase

? Bearish Headline Arguments

EIA crude oil inventories rose by a surprise 3.2 million barrels versus estimates of a decline of 2.2 million barrels and the earlier reduction of 1.3 million barrels

NZD Pairs

Overlay of NZD vs. Major Currencies Chart by TV

Last week’s bullish reaction in NZD to the RBA’s rate hike, improved risk sentiment at the start of the week, and pre-CPI U.S. dollar jitters helped lift the Kiwi early on.

Global risk-off flows changed that tune on Thursday, along with disappointing updates from New Zealand’s manufacturing sector and inflation expectations on Friday.

? Bearish Headline Arguments

BusinessNZ manufacturing index rose from 48.1 to 49.1 to reflect a slower pace of industry contraction, thanks to rising deliveries and finished stocks

Food price index slowed from an earlier 0.8% increase in March to a 0.5% monthly uptick in April, suggesting weaker consumer inflation down the line

Visitor arrivals slumped 2.9% month-over-month in March, following the earlier 0.6% increase

Quarterly inflation expectations slowed from 3.30% to 2.79% in April, suggesting weaker price pressures for the next couple of years

JPY Pairs

Overlay of JPY vs. Major Currencies Chart by TV

Yen pairs tossed and turned for the earlier half of the week, spending most of Monday through early Wednesday trading.

But the Japanese currency finally gained some traction on its climb as risk aversion sentiment spiked higher during the U.S. session, correlating with the highly anticipated U.S. CPI report.

Risk-off sentiment grew further on Thursday thanks to the previously mentioned weaker-than-expected economic updates from China and the U.S., helping the yen make extra gains to lock in the second best performance heading into the weekend.

? Bullish Headline Arguments

BOJ minutes revealed the policymakers debated the risk of inflation overshooting their expectations in March, suggesting scope for lightening up their easing efforts

BOJ minutes: Some policymakers saw “positive signs” in terms of inflation falling back within its target range

Economy Watchers sentiment index improved from 53.3 to 54.6 in April versus estimated 54.1 figure

? Bearish Headline Arguments

Average cash earnings came in at 0.8% year-over-year in March, short of projected 1.0% increase, marking a full year of declines in real wages

Household spending slumped 1.9% year-over-year in March instead of posting the estimated 0.9% gain and erasing the earlier 1.6% increase

Leading indicators fell from 98.0% to 97.5%, lower than 97.9% forecast, as economic conditions worsened in March

This post first appeared on babypips.com