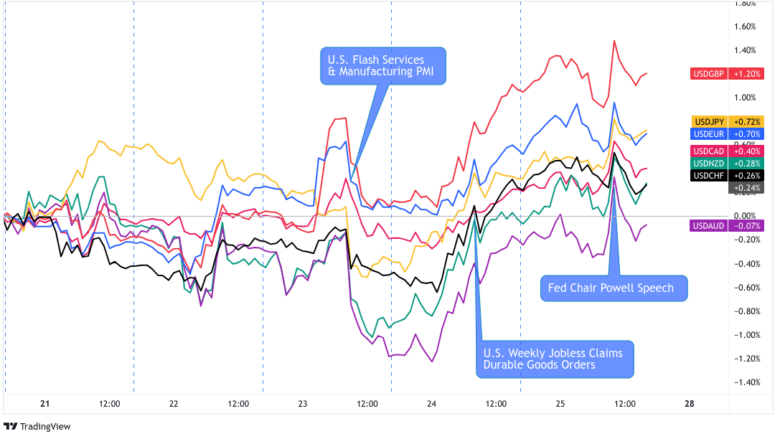

This week kicked off with an underwhelming PBOC announcement, before the spotlight turned to mostly downbeat PMI readings and the Jackson Hole Symposium.

A bit of risk-taking and anti-dollar sentiment lifted the commodity currencies midweek, but the U.S. currency managed to stage quite the turnaround later on.

Missed the major forex headlines? Here’s what you need to know from last week’s FX action:

USD Pairs

Safe-haven flows supported the dollar early in the week, following a smaller than expected PBOC prime loan rate cut.

However, the U.S. currency was barely able to extend its gains midweek, even though 10-year bond yields surged to record highs in the next couple of days.

Mostly weak flash PMI readings from major economies boosted the dollar versus the pound, euro, and Aussie on Wednesday, but it still wound up returning its intraday gains when the U.S. PMI figures also fell short. It didn’t help that a report revealed that U.S. payrolls were likely 306K lower than previously estimated.

Still, the Greenback mustered enough strength to pull up from its intraweek lows on Thursday when traders started pricing in expectations for a hawkish Powell speech in the Jackson Hole Symposium.

🟢 Bullish Headline Arguments

Federal Reserve Bank of Boston President Susan Collins sees further hikes may be necessary

U.S. 10-year bond yield broke October highs, reaching 4.35% and its highest level since November 2007

Weekly initial unemployment claims for week ending Aug. 18th: 230k (242k forecast; 240k previous)

Fed Chair Powell reiterates that the Fed will hold policy at restrictive levels until its confident inflation will move below 2% sustainably; still open raising interest rates if appropriate

Cleveland Fed President Mester said on Friday that the Fed doesn’t want to overtighten, but likely has more work to do as core inflation is too high.

🔴 Bearish Headline Arguments

Existing Home Sales for July: 4.07M (4.1M forecast; 4.16M previous)

S&P downgrades multiple U.S. banks on growing liquidity worries

Richmond Fed Manufacturing Index for August: -7.0 (-6.0 forecast; -9.0 previous); employment index fell to -3 from 5 in July

Flash Manufacturing PMI for August: 47.0 vs. 49.0 previous; Flash services PMI at 51.0 vs. 52.3

U.S. payrolls were likely 306K lower than previously estimated

Federal Reserve Bank of Philadelphia President Harker sees interest rates at restrictive levels

U.S. Durable Goods Orders for July: -5.2% m/m (0.5% m/m forecast; 4.4% m/m previous ); core durable goods came in at 0.5% m/m (0.3% m/m forecast; 0.2% m/m previous)

EUR Pairs

The shared currency was off to a slow climb at the start of the week, before the rally peaked and reversed by Tuesday.

Traders probably started pricing in expectations for another round of weak PMI figures, which would likely highlight the ECB‘s recent shift to a less hawkish stance. At the same time, the lack of euro-related catalysts then likely kept the currency sensitive to risk appetite.

Although there were some green shoots in the region’s PMI figures, EUR wound up losing ground overall, except against GBP which was also dealing with dismal results from both manufacturing and services sectors.

It wasn’t until Thursday’s London session that the shared currency put up a valiant effort to pull higher against majority of its rivals but still stayed on weak footing versus the majors (minus Sterling and the Japanese yen) despite an arguably more-hawkish-than-expected speech from ECB President Lagarde at Jackson Hole.

🟢 Bullish Headline Arguments

French flash manufacturing PMI rose from upgraded 45.1 reading to 46.4 in August

German flash manufacturing PMI ticked higher from 38.8 to 39.1 vs. 38.9 forecast

European Central Bank President Lagarde kept the door open for rate hikes and for extended restrictive monetary policy during her Jackson Hole speech on Friday.

🔴 Bearish Headline Arguments

German producer prices slumped by 1.1% month-over-month in July vs. estimated 0.1% dip and earlier 0.3% decline

French services PMI down from 47.1 to 46.7 vs. 47.5 forecast in August

German services PMI tumbled from 52.3 to 47.3 to reflect major shift to industry contraction

Eurozone consumer confidence index dipped from -15 to -16 vs. expectations of no change in August

ECB Governing Council member Mario Centeno says earlier projected downside risks have materialized

GBP Pairs

Overlay of GBP vs. Major Currencies Chart by TV

After a positive start to the week and a bit of consolidation, all hell broke loose for the British pound in the days that followed.

There actually wasn’t much on the docket for the U.K. economy, so it appears that the downbeat PMI readings and some risk-taking midweek are mostly to blame for sterling’s losses.

After all, signs of persistent trouble in the business sectors might be enough to convince BOE officials to take it easy with their rate hikes, even though inflation remains way above target.

🔴 Bearish Headline Arguments

U.K. Public Sector Net Borrowing in July: -3.48B (-17.2B forecast; -17.11B previous)

Flash Manufacturing PMI for August: 42.5 vs. 45.3 previous, 45.1 forecast, indicating sharper than expected pace of contraction

Flash Services PMI at 48.7 vs. 51.5 previous, 50.9 forecast, reflecting shift from industry growth to contraction in August

U.K. Retail Sales Volumes in August: -44 vs. -25 previous

CHF Pairs

The lack of top-tier catalysts from the Swiss economy left the franc functioning mostly as a counter currency and getting tossed around by changes in market sentiment and individual currency drivers.

The lower-yielding currency started off on bullish footing, thanks to the disappointing PBOC loan rate cut, but it wound up returning these early gains the very next day.

Another safe-haven rally boosted CHF midweek when global flash PMIs mostly fell short of estimates, but sentiment shifted a bit after weak U.S. PMIs turned on some risk-on vibes.

The rest of the week really was a mixed bag as some of the majors were focused on their individual drivers, including a weak U.K. PMIs dropping Sterling, while the U.S. tore higher on employment data and hawkish Fed speak.

🔴 Bearish Headline Arguments

Swiss trade surplus narrowed from 4.82 billion CHF to 3.13 billion CHF vs. projected 4.50 billion CHF

AUD Pairs

Despite several dips throughout the week, Aussie pairs cruised generally higher in the past few days.

The commodity currency spent Monday mostly in consolidation, chalking up some losses but quickly getting back on its feet after the PBOC announcement.

A surge in risk-taking and iron ore prices gave the Aussie a big boost on Tuesday, before it returned some winnings on downbeat flash PMI reports.

Another round of risk-on moves kept the higher-yielding currency supported midweek, but it ended up returning good chunk of these gains to its lower-yielding counterparts when traders began positioning ahead of Powell‘s Jackson Hole testimony.

Ultimately, the Aussie was able to hold on to the top spot ahead of the weekend despite a broad risk-off drop during the U.S. session, correlating with Fed Chair Powell’s arguably net hawkish speech during the Jackson Hole Symposium.

🟢 Bullish Headline Arguments

PBOC cut its 1-year prime loan rate from 3.55% to 3.45% vs. 3.40% forecast and kept its 5-year rate steady at 4.20% instead of cutting to the 4.05% consensus

🔴 Bearish Headline Arguments

Australia’s flash manufacturing PMI fell from 49.6 to 49.4 in August, services PMI down from 47.9 to 46.7 to reflect sharper pace of contraction

CAD Pairs

Overlay of CAD vs. Major Currencies Chart by TV

Apart from June retail sales data, there wasn’t much for the Loonie to chew on throughout the week, forcing the commodity currency to take cues from overall sentiment.

The start of the week was characterized by mostly sideways price action, except against the yen, then risk-off vibes spurred a gradual selloff when global PMIs broadly disappointed.

Another round of risk aversion kicked in as the focus shifted to the Jackson Hole Symposium, with many market participants still betting on relatively hawkish remarks from Fed head Powell.

🟢 Bullish Headline Arguments

Canada Retail Sales for June: +0.1% m/m to C$65.9B (-0.1% forecast; 0.1% m/m previous)

EIA crude oil inventories down by 6.1 million barrels vs. estimated reduction of 2.9 million barrels, suggesting stronger demand

🔴 Bearish Headline Arguments

Canada New Housing Price Index for July: -0.1% m/m (0.0% m/m forecast; 0.1% m/m previous)

NZD Pairs

Overlay of NZD vs. Major Currencies Chart by TV

Weak trade data printed over the weekend put the Kiwi on shaky ground early in the week, but it managed to pull higher and somewhat shrug off downbeat quarterly retail sales data from New Zealand later on.

Higher iron ore prices in Dalian lifted the Kiwi’s spirits and allowed it to trail behind the Aussie’s rally on Wednesday’s Asian session, before mixed price action ensued as global PMIs were released.

The Kiwi actually managed to score pips against the euro, pound, and dollar then, but the higher-yielding currency gave up most of these winnings as we approached the start of the Jackson Hole Symposium event on Thursday.

Price action was less uniform on Friday with the Kiwi lacking in major catalysts from New Zealand. It acted as a counter currency to other events on Friday, and traded mostly stable to lock in net gains going into the weekend.

🔴 Bearish Headline Arguments

New Zealand trade deficit widened from 0.11B NZD to 1.11B NZD in July as exports fell 14% while imports tumbled 16% during the month

PBOC cut its 1-year prime loan rate from 3.55% to 3.45% vs. 3.40% forecast and kept its 5-year rate steady at 4.20% instead of cutting to the 4.05% consensus

New Zealand credit card spending up by 3.6% year-over-year in July, slower than earlier 5.1% and indicative of weaker consumer spending

New Zealand headline retail sales fell 1.0% q/q in Q2 vs. projected 0.4% dip, core retail sales slumped 1.8% q/q vs. estimated 0.2% decline

JPY Pairs

Overlay of JPY vs. Major Currencies Chart by TV

Yen bears sprang to action as soon as the trading week started, although there were no clear catalysts for the move and recurring yen-tervention fears kept losses limited.

It’s also worth noting that, unlike most of the major economies, Japan was able to print slightly stronger than expected PMI data. Upbeat BOJ core CPI figures and news of the country’s Ministry of Finance’s plans to raise long-term rates for debt repayments likely provided some support as well.

Sideways price action ensued in the next couple of days, before a strong surge in risk aversion boosted the lower-yielding currency when majority of global PMIs came in below estimates.

Still, the Japanese currency wound up returning most of these gains on Thursday and Friday, only securing a win against the beaten down British pound.

🟢 Bullish Headline Arguments

Japan’s Ministry of Finance to raise its assumed long-term interest rate (for debt interest rate payments on annual state budget) to 1.5% based on rising government bond yields

BOJ core CPI advanced from 3.0% to 3.3% year-over-year in July vs. estimated 2.9% figure

Japanese flash manufacturing PMI ticked higher from 49.6 to 49.7 in August to signal slightly slower pace of contraction

Tokyo’s core CPI rose by 2.8% y/y in August (vs. 2.9% expected, 3.0% previous)

Japan’s corporate services price index jumped from 1.4% to 1.7% y/y in July