On Friday, we’ll get a sneak peek at one of the earliest consumer and inflation indicators closely watched by the Fed!

What are markets expecting and how may USD react?

Read on for the major points you need to know if you’re planning on trading the release:

Event in Focus:

University of Michigan Preliminary Consumer Sentiment for August 2023

When Will it Be Released:

August 11, 2023 (Friday), 2:00 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- UoM Consumer Sentiment Index to dip from 71.6 to 71.3

- UoM 1-Year Inflation Expectations to ease from 3.4% to 3.3%

- UoM 5-Year Inflation Expectations to remain at 3.0%

- UoM Current Conditions to drop from 76.6 to 76.0

- UoM Consumer Expectations to slip from 68.3 to 68.0

Relevant Data Since Last Event/Data Release:

? Arguments for Strong Sentiment Update / Likely Bullish USD

U.S. weekly jobless claims rose by 6k w/w to 227k; continuing claims rose by 21k to 1.7M; productivity rose 3.7% q/q in Q2 vs. -2.1% in Q1; unit labor costs rose by 1.6% q/q vs. 4.2% q/q/ previous

? Arguments for Weak Sentiment Update / Likely Bearish USD

Fed’s bank lending survey showed U.S. banks reporting tighter credit, weaker loan demand in Q2 2023

IBD/TIPP economic optimism index fell from 41.3 to a one-year low of 40.3 in August vs. 43.0 forecast

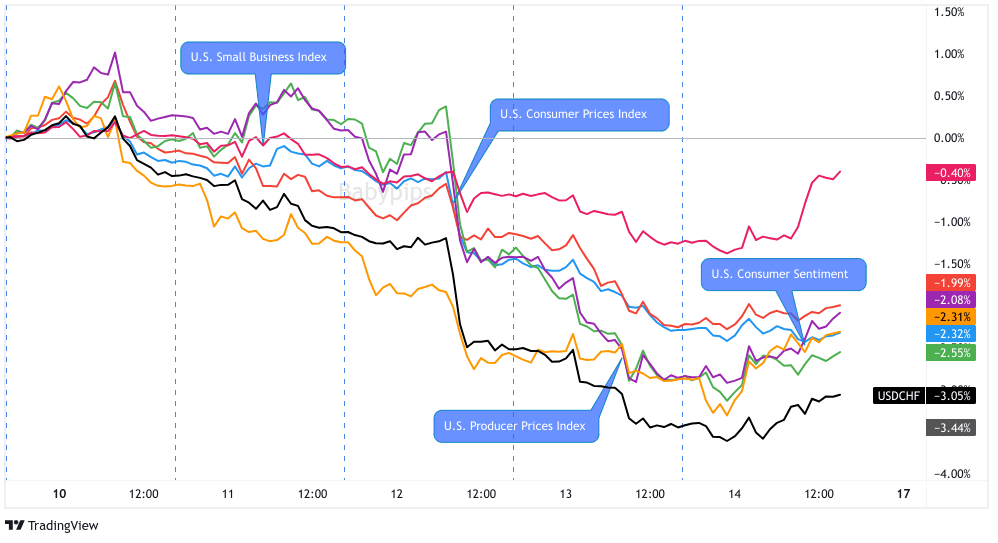

Previous Releases and Risk Environment Influence on the U.S. Dollar

July 14, 2023

Overlay of USD vs. Major Currencies Chart by TV

Event results / Price Action:

The UoM preliminary index rose by 8.2 points to 72.6 in early July, its highest level since September 2021, thanks to easing inflation and a strong labor market.

Short-term inflation expectations were little changed. Participants now expect a 3.4% annual inflation in the next year, a bit faster than the 3.3% figure in June but still much lower than the 5.4% reading in April 2022.

The U.S. dollar, which was dragged down by risk-taking following easing U.S. CPI and PPI data, shot up at the overall improvement of the report. USD extended its intraday uptrends against its major counterparts and was the second-best performer of the session after the euro.

Risk environment and intermarket behaviors:

Markets were consolidating and then all over the place earlier in the week as traders awaited the U.S. CPI report as well as the RBNZ and BOC’s policy decisions.

Confirmation that U.S. inflation rates continue to slow from high inflation levels, plus downbeat Chinese data spurring stimulus hopes, lifted risk assets towards the latter part of the week.

June 16, 2023

Event results / Price Action:

The UoM consumer sentiment index shot up from 59.2 to 63.9 in June, adding fuel to rising speculation that a soft landing is the likely scenario ahead.

The one-year inflation gauge slowed down sharply from 4.2% to 3.3%, the lowest since March 2021, over lower energy and food prices and maybe a bit from the resolution of the U.S. debt crisis.

Risk environment and intermarket behaviors:

It was a busy week for the major currencies but risk was undoubtedly on during the Friday U.S. session trading as the positive UoM consumer sentiment data pointed to a soft landing or maybe a non-recession for the U.S.

USD, JPY, and bond yields dipped while assets like oil and cryptocurrencies took advantage of a risk-friendly trading environment.

Price action probabilities:

Risk sentiment probabilities:

After a shaky start to the week where traders priced in China’s weak trade data and their worries over Italian and U.S. banks, risk-taking is getting momentum ahead of the U.S. CPI release.

It helps that rumors of China’s state-owned banks selling USD went around in the markets while weak Chinese inflation numbers are spurring talks of more stimulus. Even European stocks are getting a breather after the Italian government assured the markets that the windfall tax on banks would be “capped.”

Sentiment may turn yet again when the U.S. prints its inflation numbers. Strong or steady readings, for example, could keep the September rate hike bets alive and potentially push USD back up ahead of Friday’s consumer sentiment numbers.

U.S. Dollar scenarios:

Potential Base Scenario:

Recent gains in oil prices could have raised consumer inflation expectations while dips in employment could have dragged overall sentiment lower. Still, the Fed will be looking at the report to see if long-term inflation expectations remain mostly anchored to the 3.0% mark.

Unless we see significant surprises in inflation expectations, the report may point to the trend of consumers getting more confident. This may push USD higher as the trend would give more room for the Fed to raise its interest rates.

In case of strong consumer sentiment and inflation estimates, long USD setups against currencies with less hawkish central banks like AUD, NZD, JPY, and CHF have a better probability of positive outcomes.

Positioning will likely be a factor, most notably if the U.S. CPI update sparks a momentum move in the Greenback.

A spike higher on Thursday raises the odds of a “buy-the-rumor, sell-the-news” scenario developing on Friday, while a big dip raises the odds of quick profit taking on shorts if consumer sentiment is stronger-than-expected.

Potential Alternative Scenario:

Notable deterioration of consumer sentiment would contradict current biases that the U.S. will only see a soft (or maybe no) landing.

Concerns for the U.S. economy could weigh on USD and highlight the attractiveness of other major currencies during the Friday session. Expectations of stimulus in China, for example, could boost dollar counterparts like AUD and NZD.

If the Greenback spikes higher on Thursday after the U.S. CPI report, then a weaker-than-expected consumer sentiment read would likely spark some long profit taking ahead of the weekend.

If CPI comes in weaker-than-expected AND consumer sentiment disappointments on Friday, that may be enough to convince some traders out there to price in earlier than expected discussions of rate cuts in the future. USD could see a big pop in volatility to the downside, especially if the U.S. dollar is still holding onto weekly gains going into the Friday report.