The markets are expecting a further slowdown in China’s consumer AND producer prices growth in July!

Will it lead to concerns over the economy’s growth?

Or will weaker price pressures inspire speculation of more concrete government stimulus, potentially supporting asset prices ahead?

Event in Focus:

China Consumer Price Index (CPI) and Producer Price Index (PPI) for July 2023

When Will it Be Released:

August 9, 2023 (Wednesday), 1:30 am GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- Headline CPI m/m: +0.2% forecast vs. -0.2% previous

- Headline CPI y/y: -0.5% forecast vs. 0.0% previous

- Headline PPI y/y: -0.5% forecast vs. -5.4% previous

Relevant Data Since Last Event/Data Release:

- In mid-July, PBoC Deputy Governor Liu Guoqiang said that “This year CPI’s year-on-year growth has softened, and July may see a decline,” adding that “At this time there is no deflation, and there will be no risk of deflation in the second half of the year”

- New loan growth accelerated in China to ¥3.05T in June (¥2.9T forecast) vs. ¥3.05T from ¥1.36T in May

- China’s retail sales slowed down from 12.7% to 3.1% y/y in June

- The PBoC raised a parameter on cross-border corporate financing under its macro-prudential assessments (MPA) to 1.5 from 1.25, allowing companies to borrow more overseas in proportion to their assets

- The input prices index of China’s manufacturing PMI jumped by 4.2 pts to 45.0 in June, while the ex-factory prices index increased by 2.3 pts to 43.9

- The input prices index of China’s non-manufacturing PMI went up by 1.8 pts from 49.0 to 50.8

- Caixin’s July manufacturing PMI: “Deflationary pressure continued to build. The decline in the prices of bulk commodities…has dragged down the costs of production, and the market downturn and insufficient demand have prevented companies from raising prices for their customers.”

- Caixin’s July services PMI: “Input price inflation…dropped to its lowest level since February;” “The rate of selling price inflation softened from June.”

Previous Releases and Risk Environment Influence on AUD

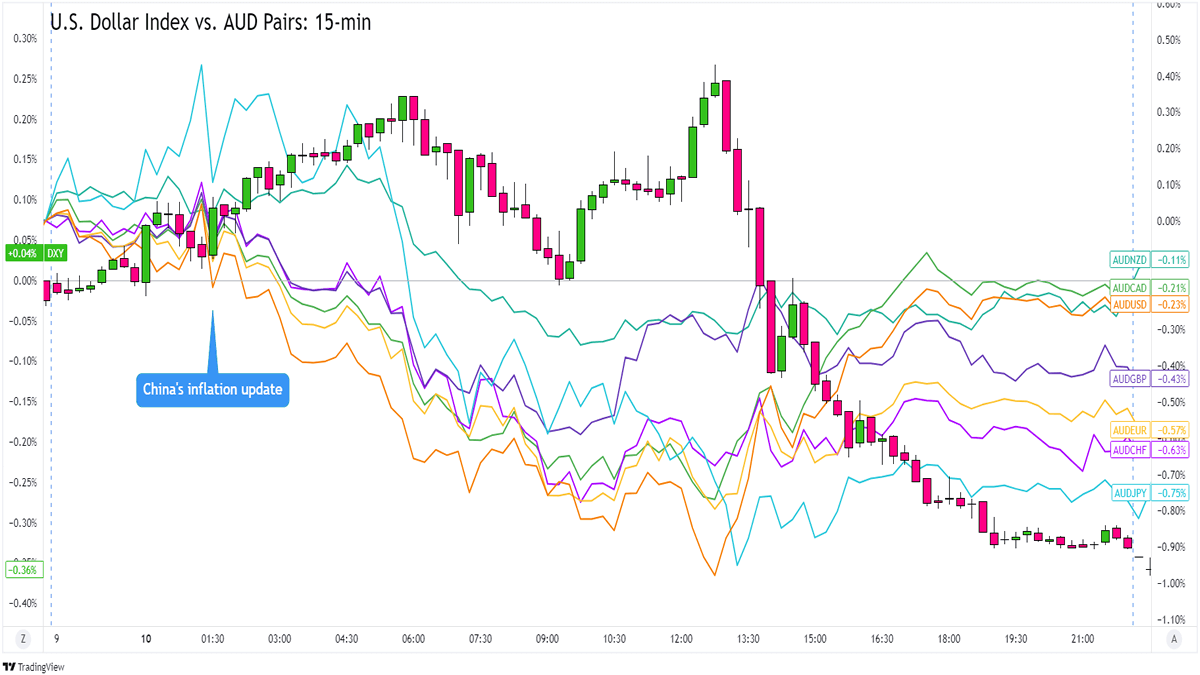

Jul 10, 2023

Event results / Price Action: China’s annualized CPI 0.0% y/y (vs. +0.2% expected, +0.2% previous) and PPI -5.4% yy/ (vs. -5.0% expected, -4.6% previous) reports both showed further deceleration in June.

After a lot of consolidation and a bit of a rally versus the dollar, AUD pairs started the week on shaky footing when China printed weaker-than-expected inflation data.

The Aussie sold off across the board, chalking up the steepest losses to the franc, yen, and euro, while also falling behind its comdoll buddies.

Meanwhile, the safe haven dollar gained ground as more traders braced for a possibly weak U.S. CPI discouraging the Fed from further rate hikes.

p

Risk Environment and Intermarket Behaviors: Like in the June release, data flow and volatility were light during the Asian session. Unlike in June, however, the Monday inflation release came ahead of a more closely watched U.S. CPI report.

The lack of “noise” at the start of the week enabled the major currencies to react more directly to China’s deflation prospects. Comdolls like AUD, NZD, and CAD traded lower until the start of the U.S. session when other catalysts moved the markets.

Jun 9, 2023

Overlay of DXY vs. Major AUD Chart by TV

Event results / Price Action: China’s monthly (-0.2% vs. -0.1% expected) and annual consumer inflation (0.2% vs. 0.3% expected) showed further price slowdowns in May. Producer prices (-4.6% y/y vs. -4.3% expected) even caught some extra attention as slow demand continued to drag prices lower.

The CPI and PPI releases ended up taking a backseat to speculations that the government had asked its biggest state banks to cut their interest rates, which may herald the PBoC’s own rate cuts.

Still, the prospect of deflation and low demand in China weighed on the China-related AUD. The comdoll broke below its U.S. session ranges and made new intraday lows until the start of European trading.

Risk Environment and Intermarket Behaviors: China’s inflation numbers were printed on a Friday following a busy trading week. There was limited volatility at the time, so major currency price reactions were muted.

We did see a bit more risk-taking in the late Asian/early European trading when speculations of a PBoC rate cut started gaining traction.

Price action probabilities:

Risk sentiment probabilities: Price action across the markets are currently mixed, with hopes of “peak interest rates” clashing with patchy data prints and global growth concerns.

Risk sentiment may get clearer as the week progresses and more traders price in their monetary policy biases, but probably not in time for the China inflation data dump, raising the level of uncertainty on the likely reaction to this event.

Keep an eye out for more concrete Chinese government stimulus announcements (being vague didn’t work last week!) or strong trade figures from China on Tuesday in case we see risk-taking before Wednesday’s release.

Australian dollar scenarios:

Potential Base Scenario: Leading indicators point to further price deceleration in July. Besides, PBoC Deputy Governor Liu Guoqiang already said that the central bank is expecting more CPI declines.

Monthly CPI may gain by 0.2% after a 0.2% decline in June but the annual CPI is expected to drop by 0.5% in July after a 0.0% June reading. Producer prices, which are suffering from slower demand, could see another 5.0% y/y drop after June’s 5.4% dip.

While inflation is decelerating all over the world, China’s situation is a bit trickier as it flirts with deflation. For newbies out there, deflation could lead to less consumer spending, tighter corporate profits, and maybe lower employment.

Unless we hear more concrete stimulus plans from the government before the release and we get signals of further inflation rate decline as expected, we could see AUD (and other risk assets correlated to China’s economic health) lose ground short-term on demand and growth concerns for the world’s second-largest economy.

Potential Alternative Scenario: With everyone and their pets already pricing in lower annual inflation that’s also partly due to base year adjustments, traders could focus on the details of the upcoming CPI and PPI reports.

If we see higher demand prospects, or if the Chinese government announces concrete stimulus ahead of the CPI and PPI releases, then “risky” assets related to China like the comdolls and crude oil may see gains against their “safer” counterparts.

Check out assets like AUD, CAD, and NZD against currencies like JPY, USD, and CHF for more obvious risk sentiment correlations. Of course, if China’s inflation data surprises to the upside, a similar price scenario may play out as traders unwind short-term weak inflation and growth bets.