The dollar was the king of pips early in the day, but divergences soon emerged when central bank officials shared insights on monetary policy.

A busy day in terms of top-tier economic reports had major currencies marching to the beat of their own drums while market sentiment continued to toss around.

European markets closed in the red as risk-off flows from geopolitical tensions lingered, but the Dow managed to squeeze out gains thanks to positive earnings data.

Headlines:

- Chinese industrial production for March: 4.5% y/y (6.0% expected, 7.0% previous)

- Chinese GDP for Q1 2024: 5.3% q/y (4.8% expected, 5.2% previous)

- Chinese retail sales for March: 3.1% y/y (5.1% expected, 5.5% previous)

- Chinese fixed asset investment for March: 4.5% ytd/y (4.0% expected, 4.2% previous)

- U.K. claimant count change for March: 10.9K (17.9K expected, 4.1K previous, positively revised from initially reported 16.8K reading)

- U.K. average earnings index for February: 5.6% 3m/y (5.5% expected, 5.6% previous)

- U.K. unemployment rate for February: 4.2% (4.0% expected, 3.9% previous)

- German ZEW economic sentiment index for April: 42.9 (35.9 expected, 31.7 previous)

- Eurozone ZEW economic sentiment index for April: 43.9 (37.8 expected, 33.5 previous)

- Canadian headline CPI for March: 0.6% m/m (0.7% expected, 0.3% previous)

- Canadian core CPI for March: 0.5% m/m (0.5% expected, 0.1% previous)

- U.S. building permits for March: 1.46M (1.51M expected, 1.52M previous)

- U.S. housing starts for March: 1.32M (1.48M expected, 1.55M previous)

- Fed official Jefferson talked about extending the current restrictive period of policy since inflation goal hasn’t been achieved

- U.S. industrial production: 0.4% m/m (0.4% expected, 0.4% previous)

- New Zealand GDT price index: 0.1% (2.8% previous)

- FOMC member Williams: Inflation across categories has fallen over 1.5 years

- ECB head Lagarde: We will cut interest rates soon, barring any major surprises in data

- BOE Governor Bailey noted encouraging signs in global economy

- BOC Governor Macklem: Downtick in core inflation suggests that price pressures are easing

- FOMC member Barkin warned that inflation data is not supportive of “soft landing” views

- Fed head Powell suggested that policymakers might wait longer to cut rates due to surprisingly strong inflation reports

- New Zealand quarterly CPI for Q1 2024: 0.6% (0.6% expected, 0.5% previous)

Broad Market Price Action:

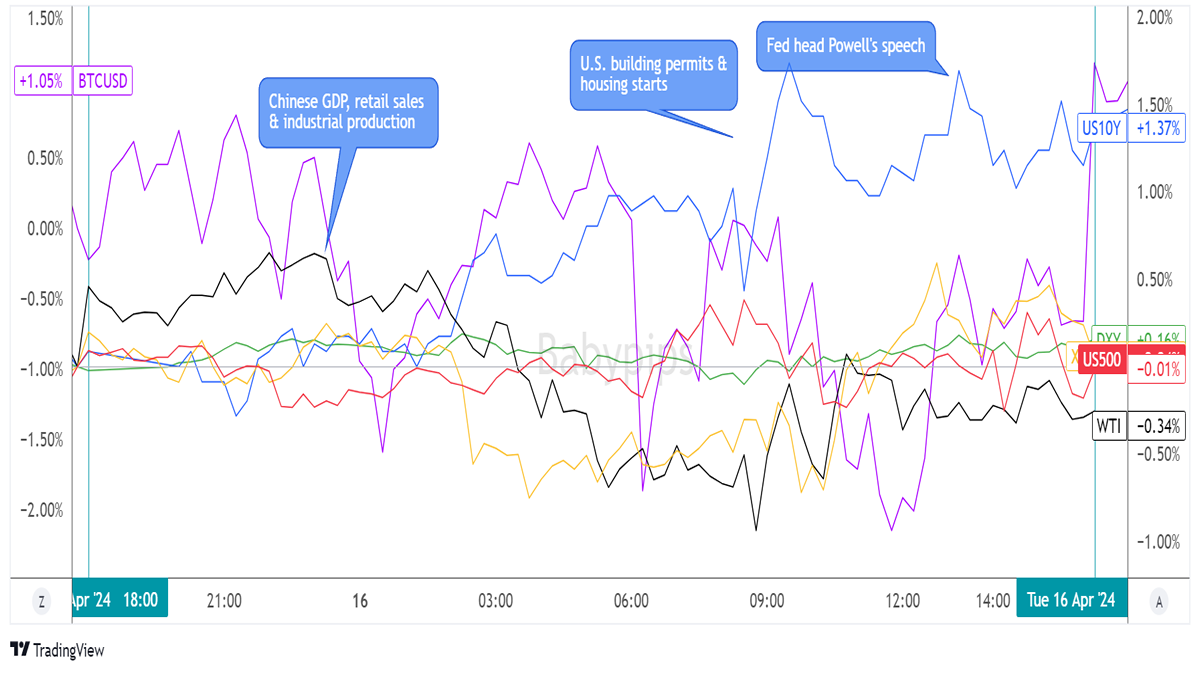

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The safe-haven dollar held its ground during the Asian market hours, as traders continued to price in the repercussions of strong U.S. retail sales data on Fed easing expectations.

China printed mixed data, with the GDP and fixed asset investment reports coming in strong while retail sales and industrial production fell short. Analysts pointed out, however, that the upside surprises should be taken with a grain of salt since stimulus measures might be propping the numbers higher.

Crude oil took hits upon seeing weak underlying demand from one of the world’s largest economies, as this could translate to slower consumption of fuel and energy commodities down the line. Gold and bitcoin also tumbled.

Later in the day, U.S. industrial production and capacity utilization data came in line with estimates and once again lifted Treasury yields while simultaneously dragging equity indices south. Fortunately for the Dow, stronger than expected earnings from Unihealth allowed the index to stay in positive territory.

The dollar also got a bit of a boost from relatively hawkish remarks from Fed officials, including main man Powell himself who mentioned that they might consider delaying interest rate cuts due to stubbornly strong inflation data.

FX Market Behavior: U.S. Dollar vs. Majors

The U.S. dollar was off to a solid start, buoyed by upbeat consumer spending data printed in the previous trading session. The safe-haven currency returned some of its gains upon seeing mostly strong Chinese data, as risk-on flows picked up.

However, profit-taking off these dollar shorts seemed swift, as market players realized that the upside surprises from China were primarily due to stimulus measures unveiled during the first quarter of the year.

Price action among the major currencies diverged during the European session when strong U.K. jobs data lifted sterling across the board while ECB head Lagarde confirmed in an interview that they are poised to cut in their next meeting. Later on, the Loonie was pulled lower by downbeat Canadian CPI, which reinforced expectations of BOC easing in June.

The Greenback enjoyed another pop higher despite weaker than expected building permits and housing starts, as traders paid closer attention to optimistic remarks from FOMC official Jefferson. He said that the central bank might look into extending the current restrictive level of policy due to stronger-than-expected price pressures.

This sentiment was echoed by Fed head Powell who also suggested that they might need to push back their rate cut timeline since they are seeing lack of progress in driving down inflation this year.

New Zealand’s quarterly CPI also allowed the Kiwi to rake in some pips, as underlying measures of inflation reflected sticky domestic inflation.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. CPI at 6:00 am GMT

- EIA crude oil inventories at 2:00 pm GMT

- BOE Governor Bailey’s speech at 4:00 pm GMT

- ECB head Lagarde’s speech at 6:00 pm GMT

- Fed Beige Book at 6:00 pm GMT

- Australia’s employment report at 1:30 am GMT (April 18)

The British pound could be front and center in the upcoming trading session, as the U.K. economy gears up to print its latest inflation report. Don’t forget that the U.K. just printed an impressive jobs report, so another strong data point could be enough to dash hopes of BOE easing anytime soon.

BOE Governor Bailey and ECB head Lagarde also have testimonies lined up that might be worth keeping tabs on!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!