Event in Focus:

Bank of Canada Monetary Policy Statement

When Will it Be Released:

April 12, Wednesday: 2:00 pm GMT, 3:00 pm London, 10:00 am New York, 11:00 pm Tokyo

Consensus Expectations:

Likely to hold the policy interest rate at 4.50%

The Bank of Canada’s business and consumer surveys indicate an impending economic slowdown, likely resulting in a more dovish outlook from the BOC at the upcoming April meeting.

While recent inflation updates have ticked lower, overall, expectations are still well above the target inflation range, making the probability of near-term easing highly unlikely.

Canadian Data Since Last Monetary Policy Statement:

| Bullish arguments for tighter monetary policy | Bearish arguments for looser monetary policy |

|

Canada GDP for January 2023: +0.5% m/m to CA$ 2.078T vs. -0.1% m/m in December

Canada CPI for February: 5.2% y/y vs. 5.9% y/y in January; +0.4% m/m vs. 0.5% m/m forecast/previous The Bank of Canada’s Summary of Deliberations showed that members were concerned that inflation will be held above the 2% target and see a potential further need to tighten monetary policy. January Canadian retail sales rose 1.4% m/m to $66.4B; core retail sales—excluding gasoline stations and fuel suppliers and motor vehicle and parts dealers—rose 0.5% m/m Canada employment change in March: +34.7K (+10K forecast) vs. +21.8K previous; unemployment rate held at 5.0% |

S&P Global Canada Manufacturing Purchasing Managers’ Index for March: 48.6 vs. 52.4 in February; Inflation rate is trending lower

Canada CPI for February: 5.2% y/y vs. 5.9% y/y in January; +0.4% m/m vs. 0.5% m/m forecast/previous Canada new housing price index for February: -0.2% m/m vs. -0.1% m/m forecast (-0.2% m/m previous) Canadian Industrial Product Price Index in February: -0.8% m/m vs. +0.3% m/m in January; Raw Materials Price Index was -0.4% m/m vs. -0.2% m/m in January |

Previous Releases and Risk Environment Influence on the Canadian Dollar

Mar 8, 2023

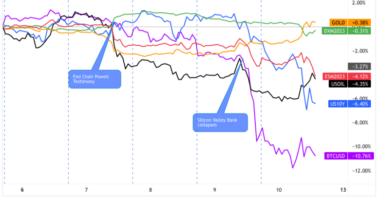

Action / results: The BOC kept interest rates on hold at 4.50% as widely expected but kept the door open for more hikes if needed. They stated that they expect their previous tightening moves to bring CPI down to their 3% target by the middle of 2023. CAD trended lower all week, likely due to the BOC pausing and on the broad risk-off environment.

Risk environment and Intermarket behaviors: Broad risk-off environment due to negative global economic updates, hawkish comments from Fed Chair Powell to fight inflation during testimony to congress. The weaker-than-expected U.S. jobs figures probably also played a role in the mood. The SVB collapse event accelerated the week’s general trend away from risky investments.

Jan 25, 2023:

Action / results: The 25 bps rate hike to 4.50% was expected and with the BOC signaling a pause in rate hikes to assess their effects on the economy, it shouldn’t have been much of a surprise that the Loonie fell after the event. That fall was short-lived though as the Loonie likely recovered with the positive lean in global risk-on sentiment this week.

Risk environment and Intermarket behaviors: No major risk sentiment catalysts during this week in January. We saw choppy and mixed intermarket price action as traders battled Fed interest rate and inflation expectations. On net, risk assets traded mostly in the green (with exception to oil prices).

Oil was choppy but ultimately net lower on the week. Possibly influenced by the latest round of PMI updates. Global PMI’s were more optimistic than expected, but still net contractionary, signaling economic slowdown ahead.

Price Action Probabilities This Week:

Risk sentiment probabilities: Broad risk sentiment has recently been shifting positive on rising probabilities that we may be passing a peak inflation environment and peak aggressiveness with regards to rate hikes.

But U.S. CPI may be a large X-Factor for overall risk sentiment. It will be released 1 hour and 30 minutes ahead of the BOC event, and may have a significant influence on broad risk sentiment during the rest of the Wednesday trading session.

A lower read in the pace of inflation may spark “risk-on sentiment” as it supports the idea of the Fed holding off on hiking interest rates aggressively, possibly opening up the possibility of a pivot.

This may overshadow the BOC statement, especially if we get a big divergence between actual and expected U.S. CPI numbers.

Loonie scenarios:

Potential Scenario 1:

BOC continues to pause, but with a more dovish tone this time around. And if market sentiment is leaning broadly risk-off, then it may draw in CAD sellers short-term if not priced in beforehand.

In this scenario, we’ll likely see mixed CAD performance against the majors, but likely net lower overall, especially if the risk environment is extremely negative and/or oil trends lower during the week.

Odds of this scenario rises if the U.S. CPI release comes in hotter-than-expected, raising odds of central banks keeping interest rates high, likely shifting risk sentiment negatively.

Watch CAD/JPY, CAD/CHF, and GBP/CAD for potential short-term short CAD setups in this scenario, especially if oil prices are trending lower.

Potential Scenario 2:

BOC continues to pause, and with a more dovish tone this time around. Broad risk sentiment leans positive, which may play out if the U.S. CPI release comes in colder-than-expected, supporting a pause in Fed monetary policy tightening behavior, and possibly even a policy pivot if economic data worsens.

CAD/JPY, CAD/CHF, and USD/CAD will be the pairs to watch for short-term long CAD setups in this scenario, especially if oil is trending higher with a fresh bullish oil catalyst.

Bullish CAD runs may be limited, depending on how hawkish/dovish the BOC may sound during their statement.